Boeing (NYSE:BA) recently released its delivery figures, revealing a mixed bag of results that led to investor concern and a slight dip in share price during Tuesday afternoon trading. While some aspects of the report were within expectations, key comparisons and ongoing challenges continue to weigh on the aerospace giant. This analysis will compare Boeing’s performance, particularly against its main competitor, and examine the factors influencing its stock outlook.

Boeing’s December deliveries reached 30 aircraft, bringing the total for 2024 to 348. At first glance, this might appear reasonable. However, when we compare these figures to previous years and, crucially, to Airbus (EADSY), the picture becomes less optimistic. Boeing’s deliveries were approximately one-third lower than in 2023. The gap between Boeing and Airbus widened significantly, highlighting the competitive pressures Boeing faces in the current market. Airbus reported delivering a staggering 766 planes, more than double Boeing’s output. These numbers underscore the challenges Boeing is experiencing in maintaining its market position. Further insights into Boeing’s financial health are expected in two weeks when the company announces its fourth-quarter and full-year earnings on January 28th. Currently, Boeing is navigating headwinds including a labor strike, a federally mandated production cap, and persistent supply chain disruptions, all contributing to its struggle to keep pace with demand and its primary competitor.

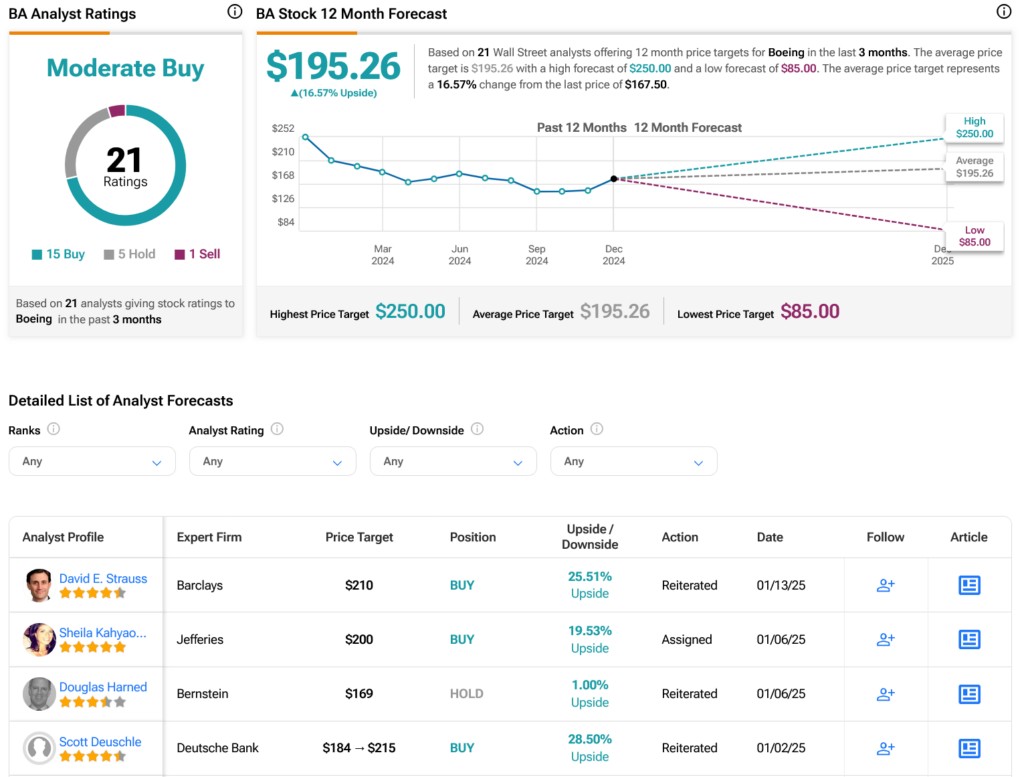

Analyst ratings for Boeing (BA) stock showing a Moderate Buy consensus.

Analyst ratings for Boeing (BA) stock showing a Moderate Buy consensus.

Despite the current challenges reflected in the Nyse:ba Compare data, there are indications of potential future improvement. According to Boeing’s vice president for commercial marketing, Darren Hulst, the company anticipates achieving a “balance between supply and market demand for passenger jets” by the end of the decade. While this timeline is not immediate, it offers a more concrete outlook than previously available. This projection suggests a five-year plan focused on resolving Boeing’s order backlog and ensuring timely aircraft delivery, which could be a positive signal for investors. This forward-looking perspective is particularly relevant given the increasing competition within the aerospace industry, including the growing influence of the Chinese market.

Turning to the financial perspective and further NYSE:BA compare analysis, Wall Street analysts currently hold a “Moderate Buy” consensus rating on BA stock. This is based on evaluations from the last three months, encompassing 15 “Buy,” five “Hold,” and one “Sell” recommendations. Despite a 16.56% decrease in Boeing’s share price over the past year, the average analyst price target for BA is $195.26. This target implies a potential upside of 16.57% from the current share price, suggesting that analysts believe in Boeing’s capacity for recovery and growth.

In conclusion, the recent delivery numbers from Boeing reveal a company still facing significant challenges when we compare NYSE:BA against its competitors. While current performance lags behind Airbus and delivery figures are down year-over-year, there is a sense of cautious optimism regarding future supply chain improvements. Analyst ratings suggest a potential upside for the stock, indicating a belief in Boeing’s long-term recovery despite current headwinds. Investors will be keenly watching the upcoming earnings report for further insights into Boeing’s financial trajectory and its ability to bridge the gap with competitors like Airbus.