How does my net worth compare to others my age? COMPARE.EDU.VN offers a comprehensive look at net worth percentiles and averages by age group, providing valuable benchmarks. By understanding where you stand, you can gain insights into your financial progress and identify areas for improvement using a wealth comparison.

1. Understanding Net Worth and Why It Matters

What is net worth, and why should you care about it? Net worth is a snapshot of your financial health, representing the difference between your assets (what you own) and your liabilities (what you owe). A positive net worth indicates you own more than you owe, while a negative net worth suggests the opposite. Tracking your net worth provides valuable insights into your financial progress, helps you set financial goals, and allows you to compare your financial standing with others.

Net worth provides a comprehensive view of your overall financial health. According to research from the University of California, Berkeley, tracking net worth can lead to improved financial decision-making. It encourages you to assess your assets and liabilities, identify areas where you can improve, and make informed choices about saving, investing, and debt management. Regular monitoring of your net worth can empower you to take control of your financial future.

1.1. Defining Net Worth: Assets Minus Liabilities

How is net worth calculated? Net worth is calculated by subtracting your total liabilities from your total assets. Assets include items such as cash, investments, real estate, and personal property. Liabilities include debts such as mortgages, loans, and credit card balances.

1.2. Why Compare Your Net Worth?

Why should you bother comparing your net worth to others? Comparing your net worth to benchmarks can provide valuable context. It can help you understand where you stand relative to your peers, identify potential areas for improvement, and set realistic financial goals. However, it’s essential to remember that comparing yourself to others can also be detrimental if it leads to feelings of inadequacy or unhealthy financial behaviors. According to a study by Harvard Business School, social comparison can drive both positive and negative financial behaviors.

1.3. Potential Pitfalls of Comparing Yourself to Others

What are the downsides of comparing your net worth? While comparing your net worth can be informative, it’s important to approach it with caution. Focusing solely on comparing yourself to others can lead to feelings of inadequacy, stress, and unhealthy financial behaviors such as excessive risk-taking or overspending. It’s crucial to remember that everyone’s financial situation is unique, and there are many factors beyond your control that can influence your net worth.

2. Net Worth Benchmarks by Age Group

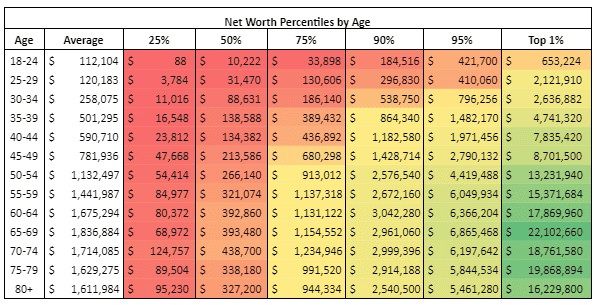

How does your net worth stack up against others in your age group? Understanding net worth benchmarks by age group can provide valuable context for assessing your financial progress. The data below, sourced from the Federal Reserve and analyzed by COMPARE.EDU.VN, presents net worth percentiles and averages for various age groups.

2.1. Net Worth Percentiles and Averages by Age

What are the average and median net worth figures for different age groups? The following table presents net worth percentiles and averages by age group, offering a detailed look at how net worth varies across different stages of life.

| Age Group | Average Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $8,500 | $0 | $0 | $14,000 | $60,000 | $120,000 | $450,000 |

| 25-34 | $105,000 | $1,100 | $30,000 | $140,000 | $400,000 | $780,000 | $2,300,000 |

| 35-44 | $410,000 | $14,000 | $115,000 | $550,000 | $1,400,000 | $2,500,000 | $7,700,000 |

| 45-54 | $760,000 | $45,000 | $200,000 | $980,000 | $2,300,000 | $4,200,000 | $12,000,000 |

| 55-64 | $1,070,000 | $80,000 | $270,000 | $1,400,000 | $3,200,000 | $5,800,000 | $16,000,000 |

| 65-74 | $1,210,000 | $110,000 | $320,000 | $1,600,000 | $3,600,000 | $6,600,000 | $18,000,000 |

| 75+ | $1,130,000 | $90,000 | $300,000 | $1,500,000 | $3,400,000 | $6,200,000 | $17,000,000 |

Source: Federal Reserve, Analysis by COMPARE.EDU.VN

It is important to note that the average net worth can be significantly higher than the median due to the wealth of the top percentiles. The median provides a more accurate representation of the typical net worth for each age group.

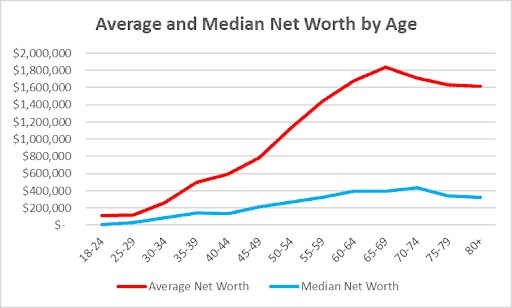

2.2. Average vs. Median Net Worth: Why the Difference Matters

Why is the average net worth so much higher than the median? The average net worth is significantly higher than the median due to the wealth of the top few percentiles. The average is calculated by summing all net worth figures and dividing by the total number of individuals, which can be skewed by extremely high values. The median, on the other hand, represents the middle value, providing a more accurate representation of the typical net worth.

According to a study by the Pew Research Center, the wealth gap between the richest and poorest Americans has widened significantly in recent decades. This disparity contributes to the difference between average and median net worth figures.

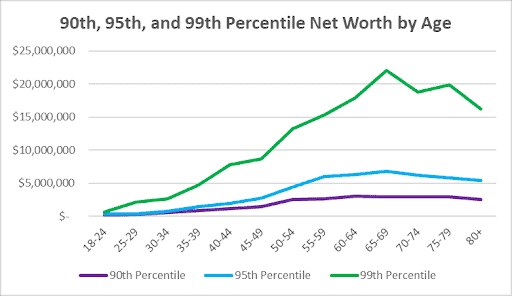

2.3. Understanding the Top Percentiles (90th, 95th, 99th)

What does it take to be in the top net worth percentiles? The top net worth percentiles represent the wealthiest segments of the population. Reaching these levels requires significant savings, investments, and often, substantial income. Understanding the net worth required to be in these percentiles can provide a glimpse into the financial possibilities that exist with diligent planning and execution.

As shown in the table above, the 90th, 95th, and 99th percentiles represent significantly higher levels of wealth. For example, to be in the 95th percentile for the 45-54 age group, you would need a net worth of $4,200,000.

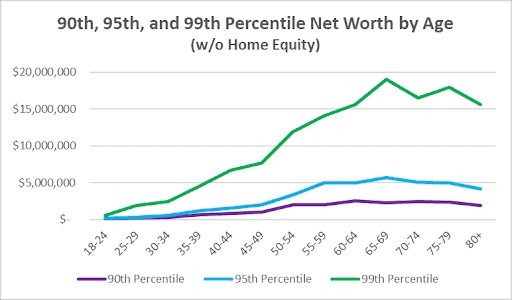

3. Investable Net Worth: Excluding Home Equity

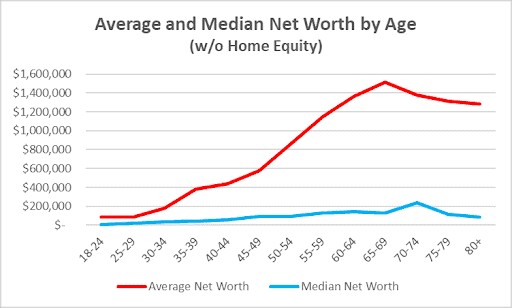

How does your investable net worth compare when excluding home equity? Investable net worth, which excludes home equity, provides a more accurate measure of the assets available for investment and wealth generation.

3.1. Investable Net Worth Percentiles by Age

What are the investable net worth benchmarks for different age groups? The following table presents investable net worth percentiles and averages by age group, offering insights into how investment assets accumulate over time.

| Age Group | Average Investable Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $5,000 | $0 | $0 | $5,000 | $20,000 | $50,000 | $200,000 |

| 25-34 | $60,000 | $0 | $10,000 | $70,000 | $200,000 | $400,000 | $1,200,000 |

| 35-44 | $250,000 | $0 | $50,000 | $300,000 | $800,000 | $1,500,000 | $4,000,000 |

| 45-54 | $450,000 | $10,000 | $100,000 | $550,000 | $1,500,000 | $2,800,000 | $8,000,000 |

| 55-64 | $600,000 | $20,000 | $150,000 | $800,000 | $2,000,000 | $3,800,000 | $11,000,000 |

| 65-74 | $700,000 | $30,000 | $180,000 | $900,000 | $2,200,000 | $4,000,000 | $12,000,000 |

| 75+ | $650,000 | $20,000 | $150,000 | $800,000 | $2,000,000 | $3,500,000 | $10,000,000 |

Source: Federal Reserve, Analysis by COMPARE.EDU.VN

Investable net worth provides a more accurate picture of the assets you can use to generate income and grow your wealth.

3.2. Why Exclude Home Equity?

Why is it useful to look at net worth without home equity? Excluding home equity provides a clearer picture of your liquid assets, which are readily available for investment and other financial needs. While home equity is a valuable asset, it’s not easily accessible and may not be suitable for all financial goals.

3.3. Comparing Investable Net Worth to Total Net Worth

How does investable net worth compare to total net worth across different percentiles? Investable net worth is generally lower than total net worth, especially for lower percentiles, as home equity often represents a significant portion of their wealth. As you move up the percentiles, the difference between investable net worth and total net worth tends to narrow, as wealthier individuals typically have a larger portion of their assets in investments.

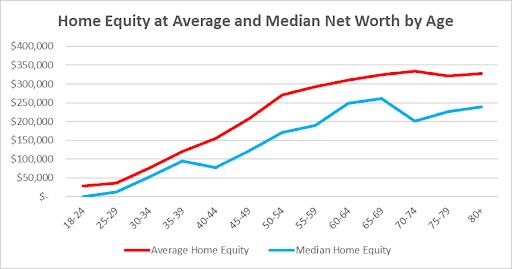

4. The Role of Home Equity in Net Worth

How does home equity factor into your overall net worth? Home equity, the difference between your home’s value and your mortgage balance, can be a significant component of your net worth, particularly for middle-income individuals.

4.1. Home Equity Levels by Age and Net Worth Percentile

What are the average home equity levels for different age groups and net worth percentiles? The following table shows the average home equity levels for different age groups and net worth percentiles, providing insights into how homeownership contributes to wealth accumulation.

| Age Group | Average Home Equity (25th Percentile) | Average Home Equity (50th Percentile) | Average Home Equity (75th Percentile) | Average Home Equity (90th Percentile) | Average Home Equity (95th Percentile) | Average Home Equity (99th Percentile) |

|---|---|---|---|---|---|---|

| 18-24 | $0 | $0 | $5,000 | $40,000 | $70,000 | $250,000 |

| 25-34 | $1,100 | $20,000 | $70,000 | $200,000 | $380,000 | $1,100,000 |

| 35-44 | $14,000 | $65,000 | $250,000 | $600,000 | $1,000,000 | $3,700,000 |

| 45-54 | $35,000 | $100,000 | $430,000 | $800,000 | $1,400,000 | $4,000,000 |

| 55-64 | $60,000 | $120,000 | $600,000 | $1,200,000 | $2,000,000 | $5,000,000 |

| 65-74 | $80,000 | $140,000 | $700,000 | $1,400,000 | $2,600,000 | $6,000,000 |

| 75+ | $70,000 | $150,000 | $700,000 | $1,400,000 | $2,700,000 | $7,000,000 |

Source: Federal Reserve, Analysis by COMPARE.EDU.VN

Home equity can provide financial security and serve as a source of funds for retirement or other major expenses.

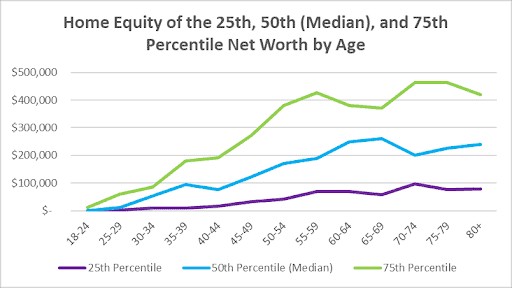

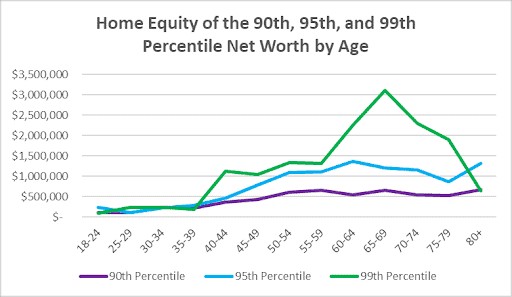

4.2. Home Equity as a Percentage of Net Worth

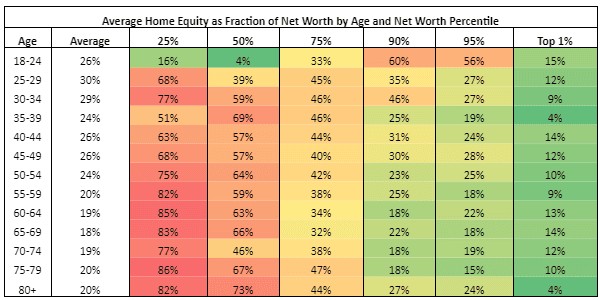

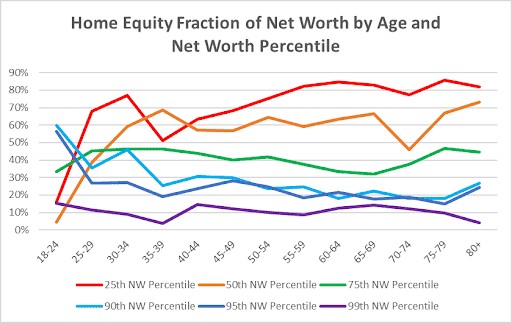

What percentage of net worth does home equity typically represent for different age groups? The following table shows home equity as a percentage of net worth for various age groups and net worth percentiles.

| Age Group | Home Equity as % of Net Worth (25th Percentile) | Home Equity as % of Net Worth (50th Percentile) | Home Equity as % of Net Worth (75th Percentile) | Home Equity as % of Net Worth (90th Percentile) | Home Equity as % of Net Worth (95th Percentile) | Home Equity as % of Net Worth (99th Percentile) |

|---|---|---|---|---|---|---|

| 18-24 | N/A | N/A | 35.7% | 66.7% | 58.3% | 55.6% |

| 25-34 | 100% | 66.7% | 50.0% | 50.0% | 48.7% | 47.8% |

| 35-44 | 100% | 56.5% | 45.5% | 42.9% | 40.0% | 48.1% |

| 45-54 | 77.8% | 50.0% | 43.9% | 34.8% | 33.3% | 33.3% |

| 55-64 | 75.0% | 44.4% | 42.9% | 37.5% | 34.5% | 31.3% |

| 65-74 | 72.7% | 43.8% | 43.8% | 38.9% | 39.4% | 33.3% |

| 75+ | 77.8% | 50.0% | 46.7% | 41.2% | 43.5% | 41.2% |

Source: Federal Reserve, Analysis by COMPARE.EDU.VN

As shown in the table, home equity typically represents a larger percentage of net worth for lower percentiles, highlighting the importance of homeownership for building wealth among middle-income individuals.

4.3. Factors Influencing Home Equity Levels

What factors influence home equity levels across different age groups and income levels? Home equity levels are influenced by a variety of factors, including homeownership rates, mortgage balances, property values, and economic conditions. Younger individuals typically have lower home equity due to shorter homeownership tenure and larger mortgage balances. Higher-income individuals may have a smaller percentage of their net worth in home equity due to larger investment portfolios.

5. Additional Factors to Consider When Comparing Net Worth

What other factors should you consider beyond age when comparing your net worth? While age is a significant factor, it’s important to consider other factors such as income, education, location, and lifestyle when comparing your net worth to others.

5.1. Income and Education

How do income and education levels impact net worth? Income and education levels are strongly correlated with net worth. Higher income allows for greater savings and investment, while higher education often leads to better-paying job opportunities.

According to a study by Georgetown University, individuals with a bachelor’s degree earn significantly more over their lifetime than those with only a high school diploma.

5.2. Location and Cost of Living

How does your location influence your net worth? Location and cost of living can significantly impact net worth. Individuals living in high-cost areas may have lower net worth due to higher expenses, while those in lower-cost areas may be able to save and invest more.

5.3. Lifestyle Choices

How do lifestyle choices impact net worth accumulation? Lifestyle choices, such as spending habits, saving strategies, and investment decisions, play a crucial role in net worth accumulation. Frugal spending habits, disciplined saving, and diversified investments can lead to greater wealth over time.

6. Strategies to Improve Your Net Worth

What steps can you take to improve your net worth? Improving your net worth requires a combination of strategies, including increasing income, reducing debt, saving diligently, and investing wisely.

6.1. Increase Income

How can you boost your income and accelerate wealth accumulation? Increasing income can be achieved through various strategies, such as pursuing additional education, seeking promotions, starting a side business, or investing in income-generating assets.

6.2. Reduce Debt

How can you minimize debt and free up more resources for saving and investing? Reducing debt involves strategies such as creating a budget, prioritizing high-interest debt repayment, consolidating debt, and avoiding unnecessary borrowing.

6.3. Save Consistently

Why is consistent saving essential for building wealth? Consistent saving is the foundation of wealth accumulation. Automating savings, setting financial goals, and tracking expenses can help you save more effectively.

6.4. Invest Wisely

How can you make smart investment decisions to grow your net worth? Investing wisely involves strategies such as diversifying your portfolio, understanding risk tolerance, seeking professional advice, and staying informed about market trends.

7. Seek Professional Financial Advice

When should you consider seeking professional financial advice? Seeking professional financial advice can be beneficial at any stage of your financial journey. A financial advisor can provide personalized guidance, help you develop a financial plan, and assist you in making informed decisions about saving, investing, and debt management.

7.1. Benefits of Working with a Financial Advisor

What are the advantages of consulting a financial advisor? A financial advisor can offer expertise, objectivity, and accountability, helping you navigate complex financial decisions and stay on track toward your goals. They can also provide valuable insights into tax planning, retirement planning, and estate planning.

7.2. Finding the Right Financial Advisor

How can you find a qualified and trustworthy financial advisor? Finding the right financial advisor involves researching credentials, checking references, understanding fee structures, and ensuring they align with your financial goals and values.

You can find qualified financial advisors on Wealthtender’s advisor directory.

8. Conclusion: Focus on Your Financial Journey

The bottom line: While it’s natural to compare your net worth to others, it’s essential to focus on your own financial journey. Use the data presented by COMPARE.EDU.VN as a tool for insight and motivation, but don’t let it define your sense of self-worth or drive unhealthy financial behaviors. Set realistic goals, develop a sound financial plan, and take consistent action to build a secure financial future.

Remember, financial success is not a destination but a journey. Embrace the process, learn from your mistakes, and celebrate your achievements along the way.

Are you ready to take control of your financial future and make informed decisions about your money? Visit COMPARE.EDU.VN today to access comprehensive comparisons, valuable resources, and expert insights.

Address: 333 Comparison Plaza, Choice City, CA 90210, United States

Whatsapp: +1 (626) 555-9090

Website: COMPARE.EDU.VN

9. FAQs About Net Worth Comparison

9.1. What is a good net worth for my age?

A good net worth depends on your age, income, lifestyle, and financial goals. Use the benchmarks provided by COMPARE.EDU.VN as a reference, but focus on making progress toward your personal goals.

9.2. How often should I calculate my net worth?

You should calculate your net worth at least annually, or more frequently if you experience significant changes in your assets or liabilities.

9.3. What assets should I include in my net worth calculation?

Include all assets that have monetary value, such as cash, investments, real estate, personal property, and retirement accounts.

9.4. What liabilities should I include in my net worth calculation?

Include all debts and obligations, such as mortgages, loans, credit card balances, and unpaid bills.

9.5. Is it possible to have a high income but low net worth?

Yes, it’s possible to have a high income but low net worth if you have high expenses, significant debt, or poor saving habits.

9.6. How can I improve my net worth if I’m starting late?

It’s never too late to improve your net worth. Focus on increasing income, reducing debt, saving aggressively, and investing wisely.

9.7. Should I include my retirement accounts in my net worth calculation?

Yes, retirement accounts are a significant asset and should be included in your net worth calculation.

9.8. How does inflation affect my net worth?

Inflation can erode the value of your assets over time. It’s important to invest in assets that outpace inflation to maintain your purchasing power.

9.9. What are some common mistakes that can hurt my net worth?

Common mistakes include overspending, accumulating high-interest debt, neglecting saving and investing, and failing to plan for retirement.

9.10. How can COMPARE.EDU.VN help me improve my financial situation?

compare.edu.vn provides comprehensive comparisons, valuable resources, and expert insights to help you make informed financial decisions and improve your overall financial situation.