Understanding why your credit scores differ between credit bureaus, such as Equifax and Experian, can be confusing. This article explores the reasons behind these variations and provides insights into credit scoring models, how they work, and factors influencing your scores.

Understanding Credit Score Variations

Your credit scores can fluctuate based on the credit scoring model, the credit report used, and the timing of the score calculation. Having multiple credit scores simultaneously is common. This is because credit scores are predictive tools used by lenders to assess the likelihood of timely bill payments. Understanding how credit scores work and how companies use them can clarify these differences.

What Factors Influence Credit Scores?

Several factors contribute to the discrepancies you might see between your Equifax and Experian scores:

Different Scoring Models: FICO vs. VantageScore

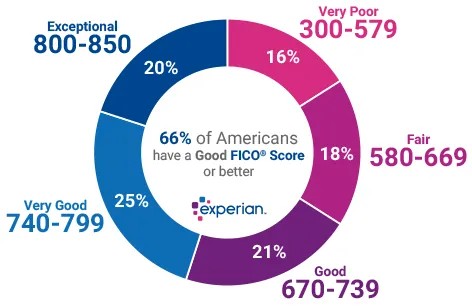

- FICO Scores: Used by 90% of top lenders, FICO offers various scoring models, including base scores (FICO Score 8, 9, and 10), industry-specific scores (auto and bankcard), and scores utilizing alternative data (banking history). These scores range from 300 to 850 (industry-specific scores range from 250-900). Higher scores indicate lower risk for lenders.

- VantageScore: Developed by Experian, TransUnion, and Equifax, VantageScore has released several versions (1.0 through 4.0 and 4plus™). VantageScore 3.0 and newer versions use a 300-850 score range, incorporating trended credit data. VantageScore 4plus™ can include data from linked bank or credit card accounts.

Even with the same score range, variations in scoring model calculations can lead to different results. For instance, mortgage lenders use specific FICO scores for each bureau: FICO Score 2 for Experian, FICO Score 5 for Equifax, and FICO Score 4 for TransUnion.

Variations in Credit Report Data

Creditors are not obligated to report to all three bureaus. They can choose which bureau(s) receive information, what data is shared, and when it’s reported. This can lead to discrepancies in your credit reports, impacting scores generated from them. Even the same scoring model can produce different scores based on the unique information in each report.

Timing of Score Updates

Credit scores are snapshots in time, reflecting the data available at the moment of calculation. Even minor timing differences in score updates can result in variations. For example, checking your FICO Score 8 with your credit card issuer and Experian on the same day might yield different results if the update times vary.

Which Credit Score Matters Most?

The most critical credit score is typically the one used by the specific lender evaluating your application. While it’s often impossible to know which score a lender will use, mortgage applications are an exception. Traditionally, lenders use older FICO scores aligned with Fannie Mae and Freddie Mac guidelines. However, a shift towards FICO 10 T and VantageScore 4.0 is underway.

Improving Your Credit Scores

While multiple scoring models exist, most rely on similar credit report data. By focusing on improving your credit report information – paying bills on time, keeping credit utilization low, and maintaining a healthy credit mix – you can positively influence all your credit scores.

Conclusion

Discrepancies between your Equifax and Experian scores are often due to differences in scoring models, credit report data, and timing. Understanding these factors can help you interpret your scores more accurately. While there’s no single “most important” score, focusing on healthy credit habits will generally improve your scores across all bureaus. Regularly monitoring your credit reports and scores empowers you to manage your financial health effectively.