When you’re shopping for a mortgage, comparing loan offers can feel overwhelming. However, understanding key components of the Loan Estimate, a standardized form provided by lenders, can simplify the process and help you make an informed decision. This document provides crucial information for comparing loan offers effectively.

Key Factors to Compare on Your Loan Estimates

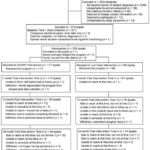

When Comparing Loan Offers You Should Use The Loan Estimate to carefully analyze the following:

Loan Amount, Interest Rate, and Monthly Payments

- Loan Amount: Verify that the loan amount aligns with your needs and borrowing capacity.

- Interest Rate: Compare interest rates from different lenders. Remember that rates can fluctuate daily. For Adjustable-Rate Mortgages (ARMs), understand the worst-case scenario if rates increase. A lower interest rate translates to lower monthly payments and overall borrowing costs.

- Monthly Principal and Interest Payment: This is the core of your monthly payment. Compare this figure across different offers.

- Mortgage Insurance: If your down payment is less than 20%, you’ll likely need mortgage insurance. Compare the monthly premiums across different loan offers.

- Total Monthly Payment: This includes principal, interest, mortgage insurance, and escrow payments (property taxes and homeowner’s insurance). This comprehensive figure represents your actual monthly outlay.

Upfront Costs and Lender Credits

- Upfront Loan Costs (Origination Charges): These are fees charged by the lender for processing your loan. Scrutinize these charges carefully as they can vary significantly.

- Lender Credits: These are rebates offered by the lender to help offset closing costs. Factor these credits into your comparison.

- Cash to Close: This is the total amount you’ll need to bring to the closing table. Ensure you have sufficient funds available.

Calculating Your Five-Year Cost of Borrowing

While you may not stay in your home for exactly five years, calculating the five-year cost provides a valuable benchmark for comparing loans:

- Locate the “In 5 Years” Section: On page 3 of the Loan Estimate, find the “Comparisons” section and the “In 5 Years” line. This section projects your total payments and principal paid over five years.

- Calculate Total Interest and Fees: Subtract the projected principal paid from the total payments to determine the total interest and fees paid over five years. This is a key metric for comparing long-term costs.

- Consider ARM Adjustments: For ARMs, remember that this is just an estimate assuming a fixed rate. Your actual costs could be higher if interest rates rise.

Negotiating and Avoiding Pitfalls

-

Negotiate with Lenders: Use competing Loan Estimates as leverage to negotiate better terms.

-

“No Closing Costs” Loans: Understand that these loans often have higher interest rates or other fees rolled into the loan amount, resulting in higher monthly payments. Be sure to compare the total cost of the loan, not just the closing costs.

-

Warning Signs: Be wary of significant discrepancies between the Loan Estimate and your initial discussions with the loan officer.

Conclusion

When comparing loan offers you should use the Loan Estimate as your primary tool. By focusing on key figures like interest rate, fees, and total monthly payment, and understanding the five-year cost projection, you can effectively evaluate different loan options and choose the mortgage that best suits your financial situation. Remember to ask questions and negotiate with lenders to secure the best possible deal.