What Is My Net Worth Compared To Others? Understanding your financial standing relative to your peers can be both enlightening and motivating, providing valuable insights into your progress towards financial goals. COMPARE.EDU.VN offers comprehensive comparisons of net worth across different age groups and demographics, helping you assess your position and make informed financial decisions. Discover benchmarks and strategies for improving your financial well-being, and explore various financial metrics.

1. Introduction: Understanding Net Worth and Its Significance

Net worth is a fundamental metric of financial health, representing the difference between your assets and liabilities. Knowing “what is my net worth compared to others” provides a benchmark to evaluate your financial standing against peers and broader demographics. This comparison can reveal areas for improvement and highlight strengths in your financial strategy.

1.1 Defining Net Worth

Net worth is calculated by subtracting your total liabilities (debts, loans, mortgages) from your total assets (cash, investments, property). It’s a snapshot of your financial health at a specific point in time, reflecting accumulated wealth and financial stability. A positive net worth indicates that your assets exceed your debts, while a negative net worth suggests the opposite.

1.2 Why Compare Your Net Worth?

Comparing your net worth to others can offer valuable insights:

- Benchmarking: Understand where you stand relative to your peers.

- Motivation: Identify areas for improvement and set realistic financial goals.

- Perspective: Gain a broader understanding of wealth distribution and economic trends.

- Validation: Acknowledge your financial achievements and build confidence.

1.3 Factors Influencing Net Worth

Several factors influence an individual’s net worth:

- Age: Net worth typically increases with age as individuals accumulate assets and pay down debts.

- Income: Higher income levels often correlate with higher savings and investment rates, leading to increased net worth.

- Education: Higher education levels can lead to higher earning potential and better financial management skills.

- Occupation: Certain professions offer higher earning potential and opportunities for wealth accumulation.

- Lifestyle: Spending habits and lifestyle choices significantly impact savings and debt levels.

- Location: Cost of living and housing markets vary by location, affecting asset values and expenses.

- Investment Decisions: Prudent investment strategies can accelerate wealth accumulation.

- Economic Conditions: Economic factors such as inflation, interest rates, and market performance can impact asset values and debt burdens.

2. Data Sources and Methodologies for Net Worth Comparison

Understanding the sources and methodologies used to gather net worth data is crucial for accurate and meaningful comparisons. Various organizations conduct surveys and studies to provide insights into wealth distribution and financial health.

2.1 Federal Reserve’s Survey of Consumer Finances (SCF)

The Federal Reserve’s SCF is a triennial survey that provides detailed information on U.S. households’ assets, liabilities, and demographic characteristics. It’s a primary source for understanding wealth distribution and trends in the United States.

- Methodology: The SCF uses a complex survey design to ensure a representative sample of U.S. households. It collects data on various assets (e.g., real estate, stocks, bonds, retirement accounts) and liabilities (e.g., mortgages, student loans, credit card debt).

- Data Points: The SCF provides data on net worth percentiles, averages, and medians by age, income, education, and other demographic factors.

- Limitations: The SCF is conducted every three years, so the data may not reflect the most recent economic changes. Additionally, the survey relies on self-reported data, which may be subject to recall bias or inaccuracies.

2.2 U.S. Census Bureau

The U.S. Census Bureau collects data on household income, poverty, and wealth through various surveys, including the Current Population Survey (CPS) and the Survey of Income and Program Participation (SIPP).

- Methodology: The CPS and SIPP use nationally representative samples to collect data on household characteristics and financial status.

- Data Points: The Census Bureau provides data on income distribution, poverty rates, and wealth inequality.

- Limitations: The Census Bureau’s wealth data may be less detailed than the SCF, as it focuses primarily on income and poverty measures.

2.3 Investment Firms and Financial Institutions

Investment firms and financial institutions often conduct their own surveys and studies to understand wealth trends and investment behavior. These studies can provide valuable insights into the financial status of their clients and the broader population.

- Methodology: Investment firms may use client data, market research, and statistical analysis to assess net worth trends.

- Data Points: These studies may provide data on asset allocation, investment returns, and wealth accumulation strategies.

- Limitations: The data from investment firms may be biased towards their client base, which may not be representative of the general population.

2.4 Academic Research and Publications

Academic researchers often conduct studies on wealth inequality, financial behavior, and economic mobility. These studies provide in-depth analysis and theoretical frameworks for understanding net worth trends.

- Methodology: Academic research uses various statistical techniques, econometric models, and qualitative analysis to examine wealth dynamics.

- Data Points: Academic studies may provide insights into the determinants of wealth accumulation, the impact of policies on wealth inequality, and the long-term trends in net worth.

- Limitations: Academic research may be limited by data availability, methodological constraints, and the scope of the study.

3. Net Worth Benchmarks by Age Group

Comparing your net worth to benchmarks for your age group is a common way to gauge your financial progress. These benchmarks provide a general sense of where you stand relative to your peers but should be interpreted with consideration for individual circumstances.

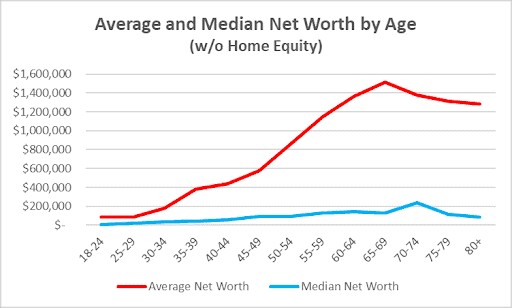

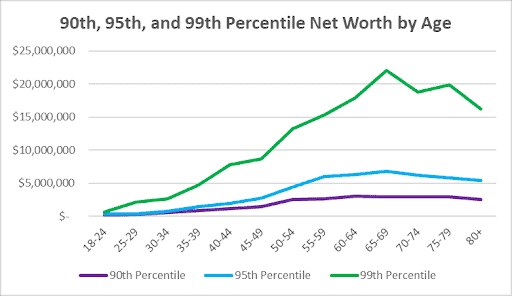

3.1 Net Worth Percentiles by Age

Net worth percentiles provide a more granular view of wealth distribution, showing the level of net worth at which a certain percentage of the population falls below. For example, the 50th percentile (median) represents the midpoint of the distribution.

| Age Group | Average Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $85,800 | $-8,400 | $11,000 | $82,000 | $279,000 | $583,000 | $1,700,000 |

| 25-34 | $224,400 | $1,500 | $54,000 | $229,000 | $723,000 | $1,300,000 | $4,200,000 |

| 35-44 | $545,400 | $23,000 | $143,000 | $524,000 | $1,400,000 | $2,700,000 | $8,600,000 |

| 45-54 | $872,900 | $82,000 | $241,000 | $833,000 | $2,100,000 | $4,100,000 | $13,300,000 |

| 55-64 | $1,209,900 | $133,000 | $357,000 | $1,100,000 | $2,700,000 | $5,200,000 | $17,000,000 |

| 65-74 | $1,269,400 | $158,000 | $404,000 | $1,200,000 | $2,900,000 | $5,500,000 | $17,400,000 |

| 75+ | $1,154,800 | $119,000 | $393,000 | $1,100,000 | $2,700,000 | $5,100,000 | $15,700,000 |

3.2 Average vs. Median Net Worth

The average net worth is calculated by summing the net worth of all individuals in a group and dividing by the number of individuals. The median net worth represents the midpoint of the distribution, where half of the individuals have a net worth above this value and half have a net worth below. The average is often skewed by a few individuals with very high net worth, making the median a more representative measure.

3.3 What the Benchmarks Tell Us

These benchmarks provide a general guideline for assessing your financial progress:

- Early Adulthood (18-34): Net worth is typically lower due to student loans, early career stages, and limited savings. Focus on building good financial habits and increasing income.

- Mid-Career (35-54): Net worth should be increasing as income rises and debts are paid down. This is a critical period for building wealth through investments and savings.

- Pre-Retirement (55-64): Net worth should be at its peak as you prepare for retirement. Focus on maximizing savings, paying off debts, and planning for income in retirement.

- Retirement (65+): Net worth may decline as you draw down assets for living expenses. Focus on managing your investments, controlling expenses, and ensuring long-term financial security.

4. Net Worth Comparison: Factors Beyond Age

While age is a significant factor, other variables play crucial roles in determining an individual’s net worth. Understanding these factors can provide a more nuanced perspective on your financial standing.

4.1 Income and Education

Income and education levels are strongly correlated with net worth. Higher income allows for greater savings and investment, while higher education often leads to better job opportunities and financial literacy.

- Income Impact: Individuals with higher incomes can allocate more resources towards savings, investments, and debt reduction. They may also have access to better financial advice and investment opportunities.

- Education Impact: Higher education levels often lead to higher-paying jobs, increased financial knowledge, and better decision-making skills. Graduates may also have a stronger focus on long-term financial planning.

4.2 Occupation and Industry

The type of occupation and industry can significantly impact earning potential and wealth accumulation. Certain professions offer higher salaries and opportunities for advancement, leading to increased net worth.

- High-Paying Occupations: Professions in fields such as finance, technology, medicine, and law often offer higher salaries and bonus structures.

- Industry Growth: Working in growing industries can provide more opportunities for career advancement and wealth accumulation.

4.3 Lifestyle and Spending Habits

Lifestyle choices and spending habits play a critical role in determining net worth. Prudent financial management, saving strategies, and responsible spending can lead to greater wealth accumulation.

- Saving Rate: The percentage of income saved each month or year directly impacts the rate of wealth accumulation.

- Debt Management: Minimizing debt, especially high-interest debt, frees up resources for savings and investments.

- Expense Control: Managing expenses, budgeting effectively, and avoiding unnecessary spending can improve financial health.

4.4 Geographic Location and Cost of Living

Geographic location and cost of living can significantly impact net worth. Housing costs, taxes, and general expenses vary widely across different regions, affecting the ability to save and invest.

- Housing Costs: High housing costs can strain budgets and reduce the amount available for savings and investments.

- Taxes: State and local taxes can impact disposable income and the ability to accumulate wealth.

- Cost of Living: General expenses, such as transportation, food, and healthcare, can vary widely by location, affecting financial health.

4.5 Marital Status and Family Size

Marital status and family size can influence net worth. Dual-income households may have greater earning potential, while larger families may face increased expenses and financial responsibilities.

- Dual Income: Two-income households may have greater earning potential and the ability to save more.

- Family Expenses: Raising children and managing family expenses can strain budgets and reduce the amount available for savings and investments.

5. Investable Net Worth vs. Total Net Worth

Distinguishing between investable net worth and total net worth provides a more accurate picture of your financial flexibility and investment potential. Investable net worth excludes assets that are not easily converted to cash, such as home equity.

5.1 Defining Investable Net Worth

Investable net worth includes assets that can be readily converted to cash and used for investments, such as stocks, bonds, mutual funds, and cash accounts. It excludes assets like home equity, which may be illiquid and subject to market fluctuations.

5.2 Why Investable Net Worth Matters

Investable net worth is a more accurate measure of your ability to generate income from investments and fund future expenses. It reflects the resources available for retirement planning, emergency funds, and other financial goals.

5.3 Investable Net Worth Benchmarks

Investable net worth benchmarks provide a more realistic view of your investment potential and financial flexibility.

| Age Group | Average Investable Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $14,000 | $0 | $0 | $2,000 | $28,000 | $84,000 | $307,000 |

| 25-34 | $62,000 | $0 | $9,000 | $50,000 | $214,000 | $470,000 | $1,500,000 |

| 35-44 | $162,000 | $3,000 | $30,000 | $150,000 | $480,000 | $980,000 | $3,200,000 |

| 45-54 | $274,000 | $15,000 | $68,000 | $280,000 | $770,000 | $1,600,000 | $5,300,000 |

| 55-64 | $407,000 | $36,000 | $120,000 | $410,000 | $1,100,000 | $2,200,000 | $7,100,000 |

| 65-74 | $417,000 | $40,000 | $126,000 | $420,000 | $1,100,000 | $2,200,000 | $6,900,000 |

| 75+ | $370,000 | $30,000 | $110,000 | $370,000 | $950,000 | $1,900,000 | $5,900,000 |

5.4 Implications for Financial Planning

Understanding your investable net worth is crucial for:

- Retirement Planning: Estimating the income you can generate from investments.

- Emergency Funds: Assessing your ability to cover unexpected expenses.

- Investment Strategies: Developing appropriate asset allocation strategies based on your risk tolerance and financial goals.

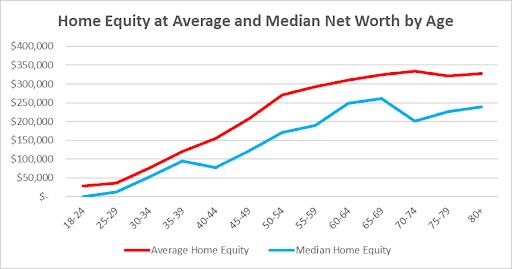

6. Home Equity and Its Impact on Net Worth

Home equity, the difference between the current market value of your home and the outstanding mortgage balance, is a significant component of net worth for many individuals.

6.1 Defining Home Equity

Home equity represents the portion of your home that you own outright. It increases as you pay down your mortgage and as the value of your home appreciates.

6.2 The Role of Home Equity in Net Worth

Home equity can contribute significantly to net worth, especially for middle-income households. However, it’s important to recognize that home equity is an illiquid asset that cannot be easily accessed for immediate needs.

6.3 Home Equity Trends by Age and Income

Home equity trends vary by age and income level. Younger households may have lower home equity due to recent home purchases and smaller mortgage payments. Higher-income households may have a smaller percentage of their net worth tied to home equity due to diversified investments.

6.4 Strategies for Managing Home Equity

- Mortgage Paydown: Accelerating mortgage payments can increase home equity and reduce interest expenses.

- Home Improvements: Investing in home improvements can increase the value of your home and build equity.

- Refinancing: Refinancing your mortgage can lower your interest rate and monthly payments, freeing up resources for other financial goals.

- Reverse Mortgages: For older homeowners, a reverse mortgage can provide access to home equity without requiring monthly payments.

7. Wealth Inequality and Its Impact on Net Worth Comparisons

Wealth inequality refers to the unequal distribution of assets and income within a population. Understanding wealth inequality is essential for interpreting net worth comparisons and recognizing the systemic factors that influence financial outcomes.

7.1 Understanding Wealth Inequality

Wealth inequality has been increasing in many countries, including the United States, over the past several decades. Factors contributing to wealth inequality include income disparities, access to education and healthcare, and tax policies.

7.2 The Gini Coefficient

The Gini coefficient is a statistical measure of income or wealth inequality, ranging from 0 (perfect equality) to 1 (perfect inequality). Higher Gini coefficients indicate greater inequality.

7.3 How Wealth Inequality Skews Net Worth Benchmarks

Wealth inequality can skew net worth benchmarks, making averages less representative of the typical individual. The median net worth is often a more accurate measure of central tendency due to the disproportionate impact of high-net-worth individuals on the average.

7.4 Policy Implications

Addressing wealth inequality requires comprehensive policy interventions, including progressive taxation, investments in education and healthcare, and measures to promote economic mobility.

8. Strategies for Improving Your Net Worth

Improving your net worth requires a combination of strategic financial planning, disciplined saving, and prudent investment decisions.

8.1 Setting Financial Goals

- SMART Goals: Set specific, measurable, achievable, relevant, and time-bound financial goals.

- Prioritize Goals: Identify your most important financial goals and allocate resources accordingly.

- Review Regularly: Review and adjust your financial goals as your circumstances change.

8.2 Budgeting and Expense Management

- Track Expenses: Monitor your spending to identify areas where you can reduce expenses.

- Create a Budget: Develop a budget that allocates income towards essential expenses, savings, and investments.

- Automate Savings: Set up automatic transfers from your checking account to your savings and investment accounts.

8.3 Increasing Income

- Skills Development: Invest in education and training to increase your earning potential.

- Negotiate Salary: Negotiate your salary and benefits package to reflect your skills and experience.

- Side Hustles: Consider starting a side hustle to generate additional income.

8.4 Debt Reduction

- Prioritize High-Interest Debt: Focus on paying down high-interest debt, such as credit card debt and personal loans.

- Debt Consolidation: Consolidate your debts to lower your interest rate and monthly payments.

- Avoid New Debt: Avoid taking on new debt unless it is absolutely necessary.

8.5 Investment Strategies

- Diversification: Diversify your investments across different asset classes to reduce risk.

- Long-Term Investing: Focus on long-term investing rather than short-term speculation.

- Rebalancing: Rebalance your portfolio regularly to maintain your desired asset allocation.

9. The Role of Financial Planning in Net Worth Management

Financial planning is essential for effectively managing your net worth and achieving your financial goals. A financial advisor can provide personalized guidance and support to help you make informed decisions.

9.1 Benefits of Financial Planning

- Personalized Guidance: A financial advisor can provide personalized guidance based on your unique circumstances and financial goals.

- Objective Advice: A financial advisor can offer objective advice and help you avoid emotional decision-making.

- Comprehensive Planning: A financial advisor can develop a comprehensive financial plan that addresses all aspects of your financial life.

- Ongoing Support: A financial advisor can provide ongoing support and help you stay on track towards your financial goals.

9.2 Choosing a Financial Advisor

- Credentials: Look for a financial advisor with relevant credentials, such as CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst).

- Experience: Choose a financial advisor with experience working with clients in similar situations to yours.

- Fee Structure: Understand the advisor’s fee structure and ensure that it is transparent and reasonable.

- References: Ask for references from current or former clients.

9.3 Key Components of a Financial Plan

- Net Worth Assessment: A comprehensive assessment of your assets and liabilities.

- Goal Setting: Clear articulation of your financial goals and priorities.

- Budgeting and Expense Management: Strategies for managing your income and expenses.

- Investment Planning: A diversified investment portfolio tailored to your risk tolerance and financial goals.

- Retirement Planning: Strategies for saving and investing for retirement.

- Estate Planning: Planning for the transfer of your assets to your heirs.

10. Future Trends in Net Worth and Wealth Accumulation

Understanding future trends in net worth and wealth accumulation can help you prepare for the challenges and opportunities ahead.

10.1 Impact of Technology

- Automation: Automation and artificial intelligence may disrupt traditional job markets, leading to income disparities.

- FinTech: Financial technology can provide access to low-cost investment and financial planning services.

- Digital Assets: Cryptocurrencies and other digital assets may offer new opportunities for wealth accumulation but also carry significant risks.

10.2 Demographic Shifts

- Aging Population: An aging population may strain social security systems and increase healthcare costs.

- Changing Family Structures: Changing family structures may impact household income and wealth accumulation.

- Increased Diversity: Increased diversity may lead to new perspectives on financial planning and wealth management.

10.3 Economic Factors

- Inflation: Inflation can erode the value of savings and investments.

- Interest Rates: Interest rate fluctuations can impact borrowing costs and investment returns.

- Market Volatility: Market volatility can create opportunities for wealth accumulation but also carry significant risks.

10.4 Sustainable Investing

- ESG Investing: Environmental, social, and governance (ESG) investing is gaining popularity as investors seek to align their investments with their values.

- Impact Investing: Impact investing focuses on generating positive social and environmental impact alongside financial returns.

Comparing “what is my net worth compared to others” is a useful exercise, but remember to focus on your personal financial goals and circumstances. Use the insights gained from these comparisons to motivate positive change and build a more secure financial future. For more detailed comparisons and personalized advice, visit COMPARE.EDU.VN at 333 Comparison Plaza, Choice City, CA 90210, United States or contact us via Whatsapp: +1 (626) 555-9090. Our website, COMPARE.EDU.VN, offers a wealth of resources to help you make informed financial decisions.

FAQ: Understanding Your Net Worth Compared to Others

1. What is net worth, and why is it important?

Net worth is the difference between your assets (what you own) and liabilities (what you owe). It’s a key indicator of your financial health and stability.

2. How do I calculate my net worth?

Add up all your assets (cash, investments, property) and subtract all your liabilities (debts, loans, mortgages).

3. What is a good net worth for my age?

Benchmarks vary, but generally, net worth increases with age as you accumulate assets and pay down debts. Refer to the tables in this article for age-specific percentiles.

4. What is the difference between average and median net worth?

Average net worth is the sum of all net worths divided by the number of individuals, while median net worth is the midpoint of the distribution. Median is often more representative due to wealth inequality.

5. What factors influence net worth?

Age, income, education, occupation, lifestyle, location, and investment decisions all play a role.

6. How does home equity affect net worth?

Home equity is the portion of your home you own outright. It can significantly increase net worth but is an illiquid asset.

7. What is investable net worth?

Investable net worth includes assets easily converted to cash for investments, excluding things like home equity.

8. How can I improve my net worth?

Set financial goals, budget effectively, increase income, reduce debt, and invest wisely.

9. What role does financial planning play in net worth management?

Financial planning provides personalized guidance, objective advice, and comprehensive strategies to help you manage your net worth effectively.

10. Where can I find more detailed net worth comparisons?

Visit COMPARE.EDU.VN for detailed comparisons and personalized advice to help you make informed financial decisions. Our address is 333 Comparison Plaza, Choice City, CA 90210, United States. You can also reach us via Whatsapp: +1 (626) 555-9090.

Don’t wait to take control of your financial future. Visit compare.edu.vn today to explore detailed comparisons, access personalized tools, and connect with financial experts who can guide you toward achieving your financial goals. Start making informed decisions and build a more secure financial future now!