For investors navigating the stock market, every decision involves trade-offs. Beyond balancing risk and potential reward in a single investment, the opportunity cost of choosing one stock over another, possibly similar, is always present. Today, we delve into a comparison between Kinder Morgan (KMI) and Chevron (CVX), two dividend-paying stocks that currently offer yields hovering around 4%, to help investors make informed choices.

Kinder Morgan: Understanding the Midstream Advantage

Kinder Morgan operates within the midstream sector of the energy industry. This crucial segment focuses on the infrastructure vital for energy movement, including pipelines, storage facilities, and transportation assets. Primarily focused on North America, Kinder Morgan generates revenue through fees charged to companies utilizing its extensive network. The midstream sector is often recognized as a stable cash flow generator within the energy landscape.

Essentially, Kinder Morgan functions as an energy toll road. Its financial performance is more closely tied to the demand for oil, natural gas, and other transported products than to the fluctuating prices of these commodities themselves. Energy demand tends to remain robust even during price downturns due to the fundamental role of oil and natural gas in economic activity.

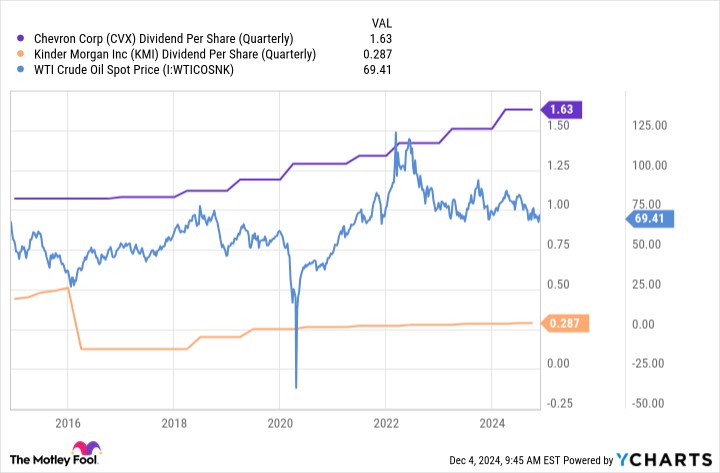

Chevron CVX Quarterly Dividend Per Share Growth Chart – NYSE CVX Compare

Chevron CVX Quarterly Dividend Per Share Growth Chart – NYSE CVX Compare

Chevron: An Integrated Energy Behemoth

Chevron presents a significantly broader scope as an integrated energy company. It operates across the entire energy value chain, encompassing upstream (oil and gas exploration and production), midstream (pipelines and transportation), and downstream (refining and chemicals). Each of these segments reacts differently to economic cycles. While the midstream offers relative stability, the upstream and downstream sectors are inherently more volatile and influenced by commodity prices. However, the upstream and downstream segments can also act as counterbalances, as oil and natural gas serve as essential inputs for the refining and chemical industries.

This comprehensive exposure across the energy sector tends to moderate the cyclical highs and lows characteristic of the energy market. Furthermore, Chevron maintains a historically conservative approach to its balance sheet. This fiscal prudence allows Chevron to strategically leverage debt during industry downturns, ensuring continued business operations and consistent dividend payouts. For investors seeking exposure to oil and gas production with a degree of stability, Chevron stands out as a more conservative option within the energy sector.

Why Chevron Currently Outshines Kinder Morgan

The midstream sector is often considered fertile ground for high-yield dividend stocks. Kinder Morgan’s dividend yield, currently slightly above 4%, is indeed attractive when compared to the S&P 500 index’s average yield of around 1.2% and the broader energy sector’s average of 3.3%. However, some of Kinder Morgan’s direct competitors offer even higher yields, reaching 6% or more.

The comparison becomes particularly compelling when considering Chevron’s dividend yield, which is also approximately 4%. While their business models differ significantly, Chevron boasts an impressive track record of increasing its dividend annually for 37 consecutive years. This consistent growth has been achieved despite the inherent volatility of its diversified operations. In stark contrast, Kinder Morgan infamously slashed its dividend in 2016. This cut was particularly jarring as it followed prior assurances to investors of a potential 10% dividend increase. Kinder Morgan’s dividend history further includes another instance in 2020 where a promised 25% increase materialized as a mere 5%.

The years 2016 and 2020 coincided with periods of significant headwinds in the energy sector. Precisely when investors might have relied on Kinder Morgan for stable income, the company reduced its dividend. Chevron, despite its substantial exposure to fluctuating energy prices, maintained its dividend commitment throughout these challenging times. This demonstrates Chevron’s superior reliability as a dividend stock.

Chevron: A Potentially Stronger Choice for Income Investors

Considering the comparable dividend yields of Chevron and Kinder Morgan, it becomes difficult to argue that Kinder Morgan is the superior energy investment, especially for investors prioritizing income. This is especially true when examining their divergent dividend histories. For those seeking high-yield energy investments, the risk-reward profile appears to favor Chevron. Alternatively, investors inclined towards the midstream sector and initially considering Kinder Morgan should explore higher-yielding peers like Enterprise Product Partners and Enbridge, both of which possess more consistent records regarding investor income streams.