Japan’s appetite for meat, particularly pork and beef, has been on a steady rise, transforming its agricultural import landscape. With domestic production covering only a fraction of its consumption, Japan relies heavily on imports, positioning the United States as a critical supplier. Recent trade agreements are poised to further reshape this dynamic, offering both opportunities and complexities for US exporters aiming to capture a larger share of the Japanese meat market. This analysis delves into the evolving Japanese beef and pork market, contrasting it with the dynamics of US exports and exploring the intricate web of trade agreements influencing this sector.

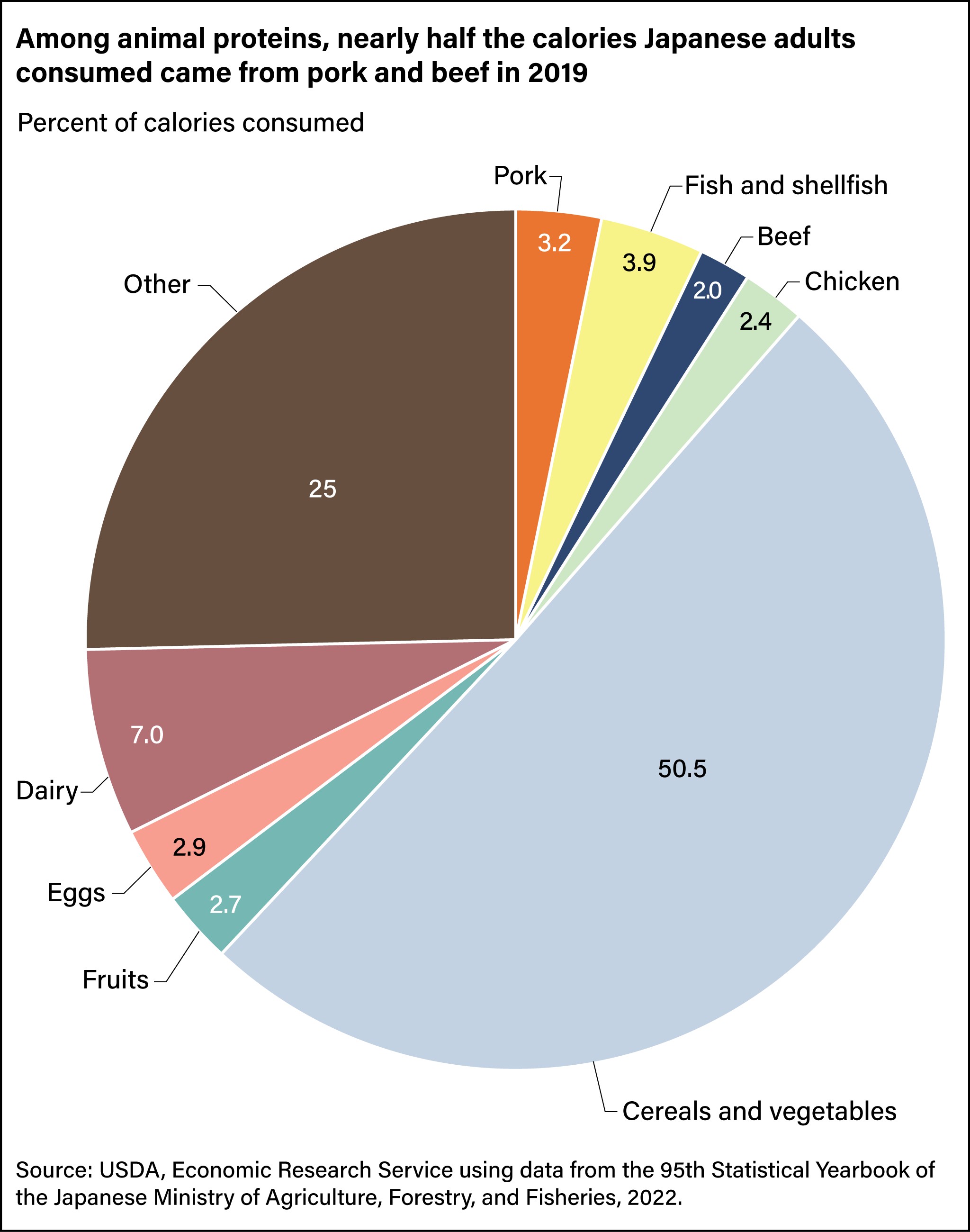

From 1990 to 2020, Japan witnessed a significant surge in meat consumption. Beef consumption climbed from 6.0 kilograms (13.2 pounds) per person annually to 7.6 kilograms (16.8 pounds), marking a 27.4 percent increase. Pork consumption also saw a substantial rise of 24.3 percent, growing from 13.0 kilograms (28.6 pounds) to 16.1 kilograms (35.5 pounds) per capita. This growth underscores pork’s position as a cornerstone of Japanese diets, second only to fish and shellfish in providing animal protein calories, according to data from the Japanese Government.

Despite growing demand, Japan’s domestic pork and beef production is shielded by tariff mechanisms designed to protect local producers from international competition. This protectionism has fostered a domestic industry, albeit at a relatively high cost. In 2021, domestic production met over 37 percent of Japan’s beef consumption and approximately 50 percent of its pork needs. The remaining demand is fulfilled through imports. Historically, Japan’s pork imports have been dominated by the United States, holding an average market share of about 38 percent, and Canada, with nearly 20 percent. For beef, Australia and the United States stand as the primary suppliers. In 2021, Australian beef accounted for 41 percent of Japan’s beef imports, closely followed by the United States at 40 percent. For the past three decades, Australia and the United States have collectively supplied over 90 percent of Japan’s beef import market.

However, the landscape of Japan’s meat market is undergoing a transformation due to the ratification of four pivotal trade agreements between 2018 and 2021. These agreements are reshaping the competitive dynamics for beef and pork imports. With the implementation of these agreements, virtually all of Japan’s beef and pork imports now originate from countries that are trade agreement partners. These landmark agreements include:

- Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP): Initially conceived as the Trans-Pacific Partnership (TPP) with 12 nations representing about 40 percent of the global economy, the United States withdrew in January 2017, leading to its renaming as CPTPP. As of September 2022, the CPTPP is fully operational for Australia, Canada, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam. Brunei and Chile’s membership will commence 60 days after their respective ratifications.

- Japan-EU Economic Partnership Agreement (Japan-EU EPA): This agreement between Japan and the 27 European Union (EU) member states came into effect in February 2019.

- U.S.-Japan Trade Agreement (USJTA): A bilateral agreement between Japan and the United States, it was enacted in January 2020.

- Japan-UK Comprehensive Economic Partnership Agreement (Japan-UK EPA): This agreement between Japan and the United Kingdom (UK) took effect in January 2021.

These trade pacts are systematically reducing import tariffs for signatory nations from the previous World Trade Organization (WTO) rates, with annual reductions planned through Japan’s fiscal year (JFY) 2033, spanning from April to March. For instance, Japan’s WTO tariff on beef imports, set at 38.5 percent, will decrease to 23.3 percent for trade-agreement signatories in JFY 2023, and further plummet to 9.0 percent by JFY 2033. Similarly, tariffs on pork imports from WTO countries stand at 8.5 percent for processed pork and 4.3 percent for unprocessed pork. However, from JFY 2028 onwards, these tariffs will be eliminated entirely for imports from trade-agreement partners.

Beyond tariff reductions, the trade agreements incorporate diverse tariff mechanisms to manage the volume of pork and beef imports into Japan. Specifically for pork, Japan maintains a gate-price system. This system establishes a minimum import price; if imported pork falls below this threshold, an additional tariff is imposed, equivalent to the difference between the gate price and the import price. To illustrate, consider scenarios for pork carcass imports, which face a 4.3 percent import tariff and a gate price of $1.62 per pound.

Scenario A: Imported carcasses priced at $2.00 per pound, exceeding the gate price. Only the standard 4.3 percent tariff applies.

Scenario B: Imported carcasses priced at the gate price of $1.62 per pound. Again, only the 4.3 percent tariff is levied.

Scenario C: Imported carcasses priced at $1.24 per pound, below the gate price. A gate price tariff of $0.38 per pound ($1.62 – $1.24) is applied, in addition to the 4.3 percent tariff on the cumulative price of $1.62 per pound.

Scenario D: Imported carcasses priced at a low $0.05 per pound. The difference from the gate price is $1.57 ($1.62 – $0.05), but the gate price tariff is capped at $1.49 per pound. The importer pays this maximum gate price tariff plus the 4.3 percent tariff on the cumulative price of $1.54 per pound ($0.05 + $1.49).

In the beef sector, the trade agreements have leveled the playing field for Japan’s primary foreign beef suppliers regarding import tariff rates. However, variations exist in safeguard mechanisms across these agreements. Safeguards trigger increased tariff rates for at least 30 days when import volumes surpass a set threshold. This safeguard system potentially disadvantages US exporters. For example, the safeguard trigger level for the United States is set lower than for CPTPP countries, despite both regions supplying similar quantities of beef to Japan. The lower trigger for the US increases the likelihood of triggering the safeguard, as occurred in March 2021.

Conversely, CPTPP beef exports to Japan are less likely to reach their higher trigger volume. In JFY 2020, CPTPP exports were less than 54 percent of their trigger level. The CPTPP trigger was initially established under the TPP framework, which included the United States, and was based on combined imports from all TPP partners. After the US withdrawal, CPTPP exporters gained additional capacity to expand exports. This situation presents a dual challenge, increasing competition for both US beef exporters and Japan’s domestic beef producers.

Japan and the United States have sought to mitigate this issue. In March 2022, Japan renegotiated the safeguard for US beef imports, implementing a triple-trigger system. This new system requires all three conditions to be met before increased tariffs on US beef imports are activated:

- US imports must exceed the trigger level specified in the USJTA for that fiscal year.

- US beef imports must surpass the previous year’s import volume.

- Combined imports from the US and CPTPP countries must exceed the CPTPP trigger level for that fiscal year.

Despite this renegotiation, the probability of US exports triggering the safeguard mechanism annually remains significant, alongside the potential for CPTPP exports to expand beyond initial projections.

To assess the comprehensive impact of these trade agreement changes on Japan’s pork and beef market, researchers at USDA’s Economic Research Service employed the Global Trade Analysis Project (GTAP) model. Their analysis focused on JFY 2033, when all beef and pork tariff adjustments will be fully implemented, comparing these projections to 2018 levels, the year preceding the agreements’ enactment. The model projects a 17.2 percent decrease in Japan’s beef production and declines of 12.5 percent and 13.2 percent in unprocessed and processed pork production, respectively. Conversely, Japan’s imports are anticipated to increase by 26.6 percent for beef, 10.8 percent for unprocessed pork, and 12.8 percent for processed pork products.

Overall, the four trade agreements are expected to stimulate increased pork and beef exports to Japan by JFY 2033. The GTAP model indicates that the United States is poised to be the primary beneficiary in monetary terms. US unprocessed pork exports to Japan are projected to rise by $143.0 million, and processed pork exports by $93.1 million. US beef exports are also expected to expand significantly, with an estimated increase of $380.8 million. However, this beef export growth is estimated to be $33.1 million less than it would have been without accounting for the high likelihood of US exports triggering Japan’s safeguard mechanism.

In conclusion, while safeguard measures present some constraints on US beef exports to Japan, effectively capping potential volume, the United States is projected to maintain or even enhance its market share in both the Japanese beef and pork sectors. The evolving trade landscape, shaped by these new agreements, points towards a future where US meat exports play an even more prominent role in meeting Japan’s growing demand.