Balance sheet reconciliation Is The Process By Which A Company Compares Its Performance using financial records to the numbers on its balance sheet to ensure they align, a critical step for maintaining financial integrity. At COMPARE.EDU.VN, we simplify complex financial comparisons, offering clear insights into balance sheet reconciliation. Ensuring accuracy in financial reporting is paramount, so understanding the nuances of balance sheet reconciliation, financial accuracy, and regulatory compliance is essential for business owners and accountants alike.

1. Understanding Balance Sheet Reconciliations

Balance sheet reconciliations are an integral part of a company’s financial reporting process. They involve a detailed comparison of a company’s financial records against the figures presented on its balance sheet. This meticulous process ensures that assets, liabilities, and shareholders’ equity are accurately stated. By cross-referencing transaction records and supporting documents, any errors, discrepancies, or omissions in the financial statements can be identified. This is not just about ticking boxes; it’s about establishing a robust foundation for financial accuracy and adhering to regulatory standards. These reconciliations are typically performed at regular intervals as part of standard accounting procedures, ensuring continuous financial health monitoring.

1.1. The Role of Closing the Books

In accounting, “closing the books” is a term used to describe the end-of-period procedures, whether it’s monthly, quarterly, or annually. This is when accountants verify the accuracy of the financial statements. The reconciliation process generally starts with the balance sheet during this crucial closing phase. Accountants reconcile several key accounts, including cash, accounts receivable, accounts payable, credit cards, fixed assets, prepaid expenses, deferred revenue, debt, and equity. Each of these accounts provides a snapshot of the company’s financial health.

1.2. Comparing Balances with Supporting Documentation

Reconciliation involves comparing the balances in the general ledger with supporting documentation to confirm the accuracy of the general ledger balance. Supporting documentation may include bank statements, subsidiary ledgers, and payment schedules. When the general ledger balance doesn’t match the supporting documentation, these differences are called reconciling items, which need thorough examination. These items can arise from timing differences, such as when a check hasn’t cleared the bank, or from errors, like unrecorded journal entries or typos. Identifying and correcting these bookkeeping errors can be time-consuming, making the automation of the reconciliation process with tools like FloQast beneficial.

2. Step-by-Step Guide to Balance Sheet Account Reconciliation

While many accounting software solutions offer built-in modules for bank account reconciliation, other balance sheet accounts often require a manual approach. Here’s a detailed guide on how to conduct a balance sheet account reconciliation:

2.1. Reconciling Cash Accounts

Reconciling cash accounts is a critical process that ensures the accuracy of recorded cash balances against actual bank balances. This procedure involves several key steps, each designed to identify and rectify any discrepancies between the company’s records and the bank’s records.

2.1.1. Step 1: Printing the General Ledger

Begin by printing or downloading the general ledger for the cash account you intend to reconcile. The general ledger provides a detailed record of all cash transactions recorded by the company, including deposits, withdrawals, and other cash-related activities.

2.1.2. Step 2: Obtaining Bank Statements

Next, print or download the corresponding bank statements for the same cash account and period. Bank statements offer an independent record of all transactions processed by the bank, including deposits, withdrawals, fees, and interest earned.

2.1.3. Step 3: Comparing Transactions

Carefully compare each transaction listed in the general ledger against those in the bank statement. This step involves matching each deposit and withdrawal recorded by the company with the corresponding entry in the bank statement.

2.1.4. Step 4: Identifying Differences

Note all differences between the general ledger and the bank statement. These differences may include transactions recorded in the general ledger but not yet reflected in the bank statement (such as outstanding checks) or transactions appearing in the bank statement but not yet recorded in the general ledger (such as bank fees or interest).

2.1.5. Step 5: Investigating Discrepancies

Investigate each difference to determine the cause and appropriate resolution. This may involve contacting the bank to clarify transactions, reviewing supporting documentation to verify accuracy, or researching internal records to identify errors or omissions.

2.1.6. Step 6: Correcting the General Ledger

Make necessary corrections to the general ledger account to reconcile any discrepancies identified during the investigation. This may involve recording adjusting journal entries to reflect transactions omitted from the general ledger or correcting errors in transaction amounts or dates.

2.2. Reconciling Other Balance Sheet Accounts

Reconciling other balance sheet accounts involves a similar process but utilizes different supporting documents specific to each account type. The fundamental steps remain consistent, but the nature of the documentation varies.

Account reconciliation depends on supporting documentation. Examples include:

| Balance Sheet Account | Supporting Document |

|---|---|

| Accounts Receivable | Subsidiary ledger, Client invoices |

| Prepaid Expenses | Subsidiary ledger, Vendor invoices |

| Accounts Payable | Subsidiary ledger, Vendor invoices |

| Credit Cards | Credit card statements |

| Fixed Assets | Subsidiary ledger, Vendor invoices |

| Deferred Revenue | Client invoices, Client contracts |

| Debt | Promissory note, Payment schedule |

3. The Importance of Balance Sheet Reconciliations

Accurate financial reporting hinges on a robust accounting process with solid internal controls. Balance sheet reconciliation is one of the most crucial internal controls. Without it, business owners cannot have confidence in their financial statements. It’s necessary to avoid inaccurate information and offers several key benefits.

3.1. Identifying Errors

Balance sheet reconciliations help in catching errors that may occur during financial transactions. This includes mistakes in recording amounts, incorrect categorization of transactions, or omissions of entries.

3.2. Spotting Weaknesses in Internal Controls

Through reconciliations, weaknesses in a company’s internal controls can be identified. This helps in strengthening these controls to prevent future errors and discrepancies.

3.3. Fraud Detection

Reconciliations can uncover fraudulent activities by detecting unauthorized transactions or manipulation of financial records. This ensures that financial assets are protected and used appropriately.

3.4. Cash Flow Management

By ensuring accuracy in financial records, reconciliations contribute to effective cash flow management. Accurate cash balances and transaction records enable businesses to make informed decisions about investments and expenditures.

Armed with a reconciled balance sheet, you’ll be more confident in making business decisions.

4. Real-World Examples of Balance Sheet Reconciliations

To better illustrate the practical application of balance sheet reconciliations, let’s examine a couple of straightforward examples: bank reconciliation and fixed asset reconciliation.

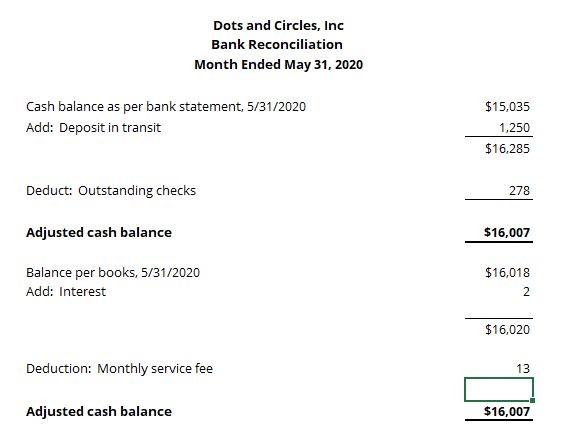

4.1. Bank Reconciliation Example

Here’s a quick look at what a simple bank reconciliation may look like:

You’ll notice the top of this reconciliation starts with the bank statement’s ending balance and then adds and subtracts entries you have on your general ledger that the bank hasn’t seen. And the bottom half of the reconciliation starts with the balance of the general ledger and then adds and subtracts entries that appear on the bank statement that you haven’t seen. In the end, the final adjusted cash balances should match. In our example, we’ll need to record journal entries with a debit of $2 for the interest revenue and a credit of $13 for the monthly service fee.

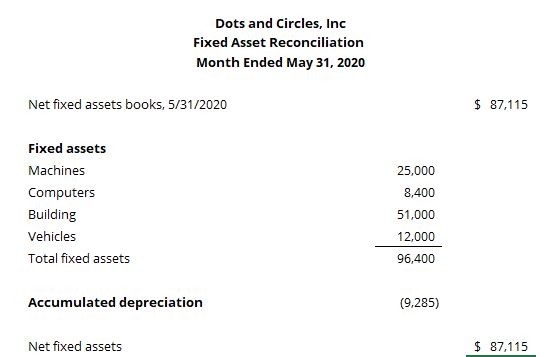

4.2. Fixed Asset Reconciliation

If you were reconciling fixed assets, a simple reconciliation might look like this:

In this example, the details on the fixed assets would be supported by invoices from when you purchased the assets. And the accumulated depreciation amount would come from your depreciation schedule.

5. Balance Sheet Reconciliation Template

To streamline your balance sheet reconciliation process, it’s helpful to start with a structured template. Using a trial balance as a starting point is an effective method.

5.1. Starting with a Trial Balance

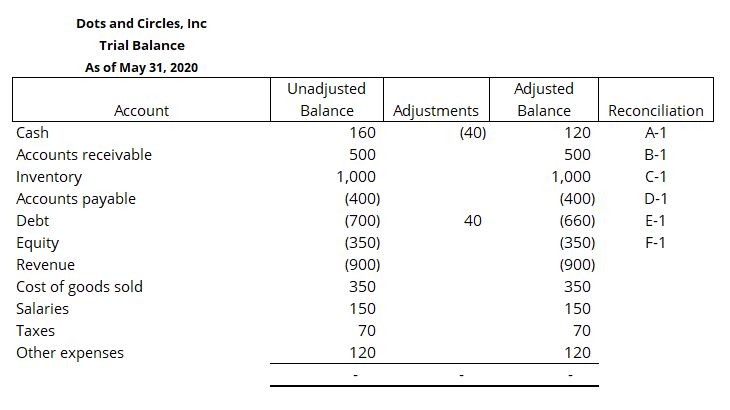

Begin with your trial balance as the launch point for your balance sheet reconciliation process. With all your accounts summarized into a column layout, you can go down the list, ensuring you have a reconciliation for each balance sheet account.

A simplified example might look like this:

The column on the far right represents where you completed the reconciliation. For cash, the bank reconciliation is located on a reconciliation labeled A-1.

5.2. Reconciling Income Statement Accounts

Income statement accounts usually aren’t reconciled. That’s because balance sheet accounts are an accumulation of transactions from day one at your business. In comparison, income statement accounts are zeroed out at the start of each year.

6. Automating Balance Sheet Reconciliations

The world of accounting is rapidly evolving, and clinging to manual processes can be a significant disadvantage. If you’ve been manually performing balance sheet reconciliations since the beginning of time, it doesn’t mean you’re stuck with it. With reconciliation software, you can put the spreadsheets, pencils, and papers away. Automating your reconciliations has several advantages:

6.1. Time Savings

Automation significantly reduces the time required to perform reconciliations, allowing accounting staff to focus on more strategic activities.

6.2. Cost Reduction

By automating the reconciliation process, businesses can reduce labor costs associated with manual data entry and error correction.

6.3. Risk Mitigation

Automated systems minimize the risk of human error, ensuring greater accuracy and reliability in financial reporting.

6.4. Increased Compliance

Automation helps businesses maintain compliance with regulatory requirements by providing a clear audit trail of reconciliation activities.

7. Key Considerations for Effective Balance Sheet Reconciliation

To ensure balance sheet reconciliations are accurate and effective, consider these best practices:

7.1. Frequency of Reconciliations

Perform reconciliations regularly, typically monthly, to catch errors early and maintain accurate financial records.

7.2. Segregation of Duties

Assign reconciliation responsibilities to individuals independent of transaction recording to prevent fraud and error.

7.3. Documentation

Maintain thorough documentation of all reconciliation procedures, including supporting documents and explanations for any discrepancies.

7.4. Review and Approval

Require independent review and approval of reconciliations to ensure accuracy and completeness.

7.5. Training and Education

Provide ongoing training and education to accounting staff on reconciliation procedures and best practices.

8. Common Challenges in Balance Sheet Reconciliation

Despite the importance of balance sheet reconciliation, several challenges can impede its effectiveness.

8.1. Inadequate Documentation

Insufficient or incomplete documentation can make it difficult to identify and resolve discrepancies.

8.2. Complex Transactions

Complex transactions, such as those involving foreign currencies or derivatives, can be challenging to reconcile accurately.

8.3. System Integration Issues

Lack of integration between accounting systems can lead to errors and inefficiencies in the reconciliation process.

8.4. High Volume of Transactions

A high volume of transactions can overwhelm accounting staff and increase the risk of errors.

8.5. Human Error

Human error, such as data entry mistakes or incorrect calculations, remains a significant challenge in balance sheet reconciliation.

9. The Role of Technology in Streamlining Reconciliation

Technology plays a crucial role in streamlining and enhancing the efficiency of balance sheet reconciliation processes.

9.1. Automated Matching

Automated matching algorithms can quickly identify and match transactions between the general ledger and supporting documents, reducing manual effort.

9.2. Real-Time Visibility

Real-time dashboards provide instant visibility into reconciliation status, allowing accounting staff to monitor progress and address issues promptly.

9.3. Workflow Automation

Workflow automation tools streamline the reconciliation process by automating tasks such as document retrieval, discrepancy resolution, and approval routing.

9.4. Data Analytics

Data analytics capabilities enable accounting staff to identify patterns and trends in financial data, facilitating proactive identification of errors and anomalies.

9.5. Cloud-Based Solutions

Cloud-based reconciliation solutions offer scalability, accessibility, and collaboration features, enabling accounting teams to work more efficiently and effectively.

10. Future Trends in Balance Sheet Reconciliation

As technology continues to evolve, several trends are poised to shape the future of balance sheet reconciliation.

10.1. Artificial Intelligence (AI)

AI-powered reconciliation solutions will automate complex tasks such as discrepancy resolution and fraud detection, improving accuracy and efficiency.

10.2. Robotic Process Automation (RPA)

RPA will automate repetitive tasks such as data entry and document retrieval, freeing up accounting staff to focus on higher-value activities.

10.3. Blockchain Technology

Blockchain technology will enhance transparency and security in financial reporting by providing a tamper-proof ledger of transactions.

10.4. Continuous Auditing

Continuous auditing techniques will enable real-time monitoring of financial data, allowing for proactive identification and resolution of errors and anomalies.

10.5. Predictive Analytics

Predictive analytics will forecast potential reconciliation issues, allowing accounting staff to take preventive measures and minimize financial risks.

11. Frequently Asked Questions (FAQ) About Balance Sheet Reconciliation

To provide further clarity and address common queries related to balance sheet reconciliation, here are some frequently asked questions:

11.1. What is the primary purpose of balance sheet reconciliation?

The primary purpose of balance sheet reconciliation is to ensure the accuracy and reliability of financial statements by verifying that the balances in the general ledger match supporting documentation.

11.2. How often should balance sheet reconciliations be performed?

Balance sheet reconciliations should be performed regularly, typically monthly, to catch errors early and maintain accurate financial records.

11.3. Who is responsible for performing balance sheet reconciliations?

Balance sheet reconciliations are typically performed by accounting staff, such as accountants, bookkeepers, or financial analysts.

11.4. What types of accounts require balance sheet reconciliation?

All balance sheet accounts, including cash, accounts receivable, accounts payable, fixed assets, and debt, require balance sheet reconciliation.

11.5. What supporting documents are needed for balance sheet reconciliation?

Supporting documents for balance sheet reconciliation may include bank statements, subsidiary ledgers, vendor invoices, client invoices, and payment schedules.

11.6. What steps are involved in the balance sheet reconciliation process?

The balance sheet reconciliation process typically involves printing the general ledger, obtaining supporting documents, comparing transactions, identifying differences, investigating discrepancies, and correcting the general ledger.

11.7. How are discrepancies resolved during balance sheet reconciliation?

Discrepancies are resolved by investigating the cause of the difference, reviewing supporting documentation, and making necessary corrections to the general ledger.

11.8. What are the benefits of automating balance sheet reconciliation?

The benefits of automating balance sheet reconciliation include time savings, cost reduction, risk mitigation, and increased compliance.

11.9. What challenges are commonly encountered during balance sheet reconciliation?

Common challenges encountered during balance sheet reconciliation include inadequate documentation, complex transactions, system integration issues, high volume of transactions, and human error.

11.10. How can technology enhance the efficiency of balance sheet reconciliation?

Technology can enhance the efficiency of balance sheet reconciliation through automated matching, real-time visibility, workflow automation, data analytics, and cloud-based solutions.

12. Finding Balance Sheet Solutions at COMPARE.EDU.VN

Navigating the complexities of financial management requires reliable tools and resources. At COMPARE.EDU.VN, we provide comprehensive comparisons to help you make informed decisions about your financial processes. Whether you’re comparing accounting software, seeking cost-effective solutions, or improving overall accounting accuracy, COMPARE.EDU.VN is your go-to source.

12.1. Enhance Your Financial Accuracy Today

Ready to enhance your financial accuracy and streamline your balance sheet reconciliation process? Visit COMPARE.EDU.VN for detailed comparisons and expert insights. Our platform helps you find the best tools and strategies to meet your specific business needs.

12.2. Contact Us

For more information or assistance, please contact us.

- Address: 333 Comparison Plaza, Choice City, CA 90210, United States

- WhatsApp: +1 (626) 555-9090

- Website: COMPARE.EDU.VN

Discover how compare.edu.vn can help you achieve financial excellence with accurate and efficient balance sheet reconciliations.