Comparable company analysis (CCA), also known as “comps,” is a crucial valuation method used to estimate the value of a company by comparing it to similar publicly traded companies. This guide provides a comprehensive breakdown of how to perform a comparable company analysis, a skill essential for financial analysts in various fields.

Identifying Comparable Companies: The Foundation of CCA

The first step in conducting a CCA involves identifying appropriate comparable companies. This requires in-depth research to find publicly traded companies with similar characteristics to the target company. Key factors to consider include:

- Industry Classification: Ensure comparables operate within the same industry sector. Using industry classification codes (e.g., GICS or ICB) can help refine the search.

- Geography: Consider the geographical markets in which the companies operate, as regional economic factors can impact valuation.

- Size: Compare companies with similar revenue, assets, and market capitalization to ensure a relevant comparison.

- Growth Rate: Look for companies with comparable historical and projected growth rates in revenue and earnings.

- Margins and Profitability: Analyze key profitability metrics such as gross margin, operating margin, and net income margin to ensure comparability. Resources like CapIQ and Bloomberg can streamline this process.

Comparable Company Analysis Factors

Comparable Company Analysis Factors

Gathering Financial Data: Building Your Comps Table

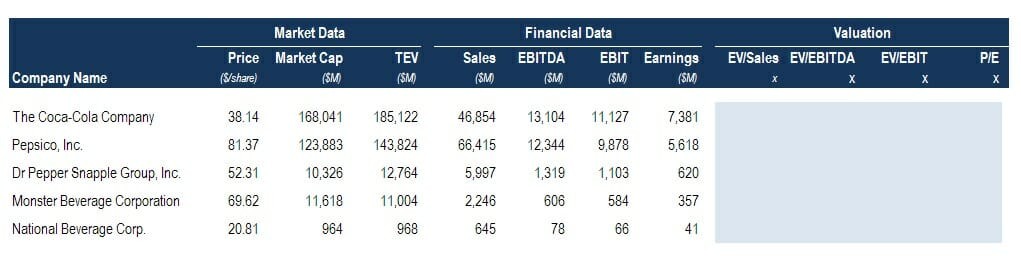

Once potential comparables are identified, gather their financial data. Sources like SEC filings (10-K, 10-Q), company annual reports, and financial databases (Bloomberg, Capital IQ) are invaluable. Essential data points include:

- Market Data: Current share price, number of shares outstanding, market capitalization, and enterprise value (EV).

- Financial Data: Key financial metrics from the income statement, balance sheet, and cash flow statement for the past three to five years. These include revenue, gross profit, EBITDA, EBIT, net income, total assets, total debt, and operating cash flow. You’ll also need analyst estimates for future performance.

Calculating Valuation Multiples: Unveiling Relative Value

With the financial data compiled, calculate key valuation multiples. Common multiples used in CCA include:

- EV/Revenue: Measures the enterprise value relative to revenue.

- EV/Gross Profit: Assesses the enterprise value relative to gross profit.

- EV/EBITDA: A widely used multiple that compares enterprise value to earnings before interest, taxes, depreciation, and amortization.

- Price-to-Earnings (P/E): Compares the market price per share to earnings per share.

- Price-to-Book (P/B): Measures the market price relative to book value of equity.

Organize these multiples in a comps table, clearly separating market data, financial data, and calculated multiples for each comparable company. Calculate the average or median multiple for each metric, often excluding outliers to improve accuracy.

Applying Multiples to the Target Company: Determining Valuation

Apply the calculated average or median multiples to the corresponding financial metrics of the target company. This provides a range of potential valuations for the target company. For example, if the average EV/EBITDA multiple for the comparable group is 10x, and the target company’s EBITDA is $10 million, the estimated enterprise value of the target company would be $100 million.

Interpreting the Results: Beyond the Numbers

The final step involves interpreting the results and drawing conclusions about the target company’s valuation. Remember that CCA provides a relative valuation, not an absolute one. Analyze why certain multiples differ between comparable companies. Consider factors like growth rates, risk profiles, capital expenditure requirements, and market sentiment. This qualitative analysis is crucial for informed decision-making.

Conclusion: The Power of Comparable Company Analysis

Comparable company analysis is a powerful tool for valuing companies, particularly in the context of M&A transactions, IPOs, and investment decisions. By systematically comparing a target company to its peers, CCA provides a market-based perspective on its relative value. While quantitative analysis is central to CCA, qualitative factors and in-depth understanding of the industry and individual companies are crucial for accurate and insightful valuation. This comprehensive guide provides a solid foundation for performing effective comparable company analysis.