Comparable analysis is a powerful valuation tool, but How To Do Comparable Analysis effectively? COMPARE.EDU.VN offers a detailed guide, comparing similar entities to derive a fair valuation. This method, also known as “comps,” helps assess a company’s value by examining its peers. Discover how to conduct thorough comparative assessments and benchmark valuations with ease, and learn about its intricacies.

1. What is Comparable Company Analysis?

Comparable Company Analysis (CCA), at its core, is a relative valuation technique. It determines a company’s worth by comparing it to the current market prices of similar businesses. Essentially, it’s about finding “comps” – those companies that share key characteristics with the target company. This is a very important financial model.

Once you’ve identified your peer group – those similar companies – and the appropriate valuation multiples (we’ll get to those shortly), you can apply the median or average multiple from the peer group to the corresponding metric of your target company. This gives you a “comps-derived valuation” – an estimate of what the target company might be worth based on how the market values its peers. COMPARE.EDU.VN can guide you through each step, ensuring accuracy and reliability in your analysis.

Understanding comparable company analysis and how to calculate it.

2. Comparable Company Analysis: A Detailed Guide

Think of comparable company analysis as finding the fair market value (FMV) of a house. You research nearby houses with similar features that have recently sold. You’re essentially performing a basic “comps” analysis.

The principle behind comparable company analysis is simple: similar companies offer a useful reference point for estimating the value of the target company.

The valuation derived from “trading comps” (another name for this method) isn’t meant to be a precise calculation. Instead, it establishes parameters for the target company based on current market pricing of comparable firms. However, company valuation is way more complex. It requires in-depth understanding of various metrics and careful selection of comparison group.

3. Valuation Multiples in Trading Comps: A Quick Review

Valuation multiples are the cornerstone of comparable company analysis. They are ratios that compare a measure of value to an operating metric.

- Numerator: This is your value measure. Common examples include Enterprise Value (EV) and Equity Value.

- Denominator: This is the “value driver” – the metric that helps determine value. Common examples include EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), EBIT (Earnings Before Interest and Taxes), Net Income, and Earnings Per Share (EPS).

A critical rule is that the investor group represented in the numerator and denominator must match. In other words, you can’t mix and match. For example, Enterprise Value represents all capital providers (equity and debt holders), while Equity Value only represents common shareholders. Mismatched representation will cause the multiple to be inaccurate.

While the Price-to-Earnings (P/E) ratio is widely known and used among retail investors (and often taught in academic settings), industry professionals primarily use multiples based on Enterprise Value. These multiples are independent of the company’s capital structure and focus on its core operations.

COMPARE.EDU.VN provides detailed explanations of valuation multiples, helping you choose the right ones for your analysis.

4. Comparable Company Analysis: Step-by-Step Overview

Let’s break down the process of performing comparable company analysis into a series of steps.

-

### 4.1. Step 1: Compile Peer Group

The first and most crucial step is to create a peer group. This group should consist of publicly traded companies that are similar to the target company. Ideally, these companies should be competitors or operate in the same industry. Selecting the right peer group is important for the reliability of the analysis.

-

### 4.2. Step 2: Industry Research

Next, you need to gather information from public sources about the target company and the industry it operates in. Understand the market trends and the factors influencing how the market values companies in that industry. Good industry knowledge will improve the accuracy of the peer selection process.

-

### 4.3. Step 3: Input Financial Data

Collect financial data for each company in your peer group. This data should be “scrubbed,” meaning you need to adjust the financials to account for non-recurring items, accounting differences, leverage differences, and any cyclicality or seasonality. In some cases, you might also need to calendarize the financials to standardize the dates (e.g., convert different fiscal year-end dates to a common timeframe).

-

### 4.4. Step 4: Calculate Peer Group Multiples

With the financial data in place, you can calculate the valuation multiples for each company in the peer group. These multiples are then compared against each other. Generally, multiples are displayed on a Last Twelve Months (LTM) and Next Twelve Months (NTM) basis. You should also calculate and summarize the minimum, 25th percentile, median, mean, 75th percentile, and maximum for each metric.

-

### 4.5. Step 5: Apply Multiple to Target

Finally, apply the median or average multiple from the peer group to the corresponding metric of the target company. This gives you the comps-derived value of the target. Remember to consider the underlying drivers that impact valuation. It’s crucial to justify why a target should be valued at the lower (or higher) end of the range.

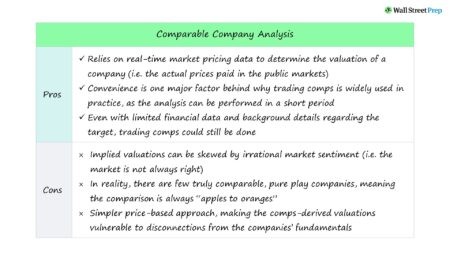

5. Pros and Cons of Comparable Company Analysis

Comparable company analysis is a valuable tool, but it’s not without its limitations. Understanding the pros and cons is important for using this method wisely.

The accuracy of trading comps analysis depends on the quality of the selected comparable companies.

Generally speaking, the more rigorous the screening process for comparable companies, the more reliable the trading comps valuation.

If there aren’t many comparable companies in the public markets, the screening process becomes less strict, which reduces the credibility of the comps valuation.

Trading comps offer a realistic view of market pricing because they’re based on actual prices in real-time. However, comps are susceptible to market inefficiencies – the market can misprice securities, especially those with smaller followings and less trading volume.

A common misconception is that comps don’t require as many assumptions as a Discounted Cash Flow (DCF) analysis. In reality, the same operating assumptions are made, but they’re implicit rather than explicit.

The core assumption behind comparable company analysis is that the market is composed of rational investors.

However, significant disconnects can occur between security prices and company fundamentals. This highlights the importance of using multiple valuation methods.

Given these drawbacks, trading comps should be used in conjunction with other valuation methods, such as the DCF, rather than as a standalone method. Think of it as a “sanity check.”

6. Comps Selection Criteria: Building a Peer Group

The “peer group” is the group of companies you’ll be comparing to your target company.

To maximize accuracy, the peer group should consist of companies that share various characteristics with the target company, including business characteristics, financials (cash flow drivers), and risks.

Here’s a breakdown of key peer group selection criteria:

-

### 6.1. Business Characteristics:

Consider factors like the product/service mix and the type of customer served.

-

### 6.2. Financials:

Look at metrics like revenue growth, operating margins, and EBITDA margins.

-

### 6.3. Risks:

Assess potential risks like changes in the regulatory landscape, industry headwinds, and the competitive landscape.

Ideally, the target company will have a readily available list of close competitors to serve as a starting point for building the peer group.

For example, if you’re compiling comparable companies for Microsoft (NASDAQ: MSFT), the peer group should include enterprise software companies with product offerings in related areas.

Selecting operationally similar companies should be your primary goal when creating a peer group, focusing the majority of your time and effort.

However, “pure-play” (exact) comparable companies are rare. It’s important to be realistic and flexible when screening and choosing peers, especially if the target company operates in a niche area.

7. Enterprise Value vs. Equity Value Multiples: The Key Difference

Enterprise Value and Equity Value, along with operating metrics like EBITDA, cannot be compared in their absolute forms. Valuation multiples standardize these values, enabling comparisons across companies of varying sizes and other differences.

To recap, Enterprise Value represents the total value of the company to all investors (debt and equity holders), while Equity Value represents the value attributable to shareholders.

8. Non-Recurring Items Adjustments

A common mistake is neglecting to adjust the financials of the peer group, often called “scrubbing” the financials.

Almost every company’s financials are affected by non-recurring income or expenses (e.g., one-time integration costs for a new acquisition or repair costs from a recent hurricane).

Since the goal is to compare the core operations of each company in the peer group, it’s important to remove the impact of these one-time items that won’t continue in the future.

Understanding the financial assumptions of trading comps model.

9. Comparable Company Analysis (CCA) Process

Spreading comps can be a time-consuming process, with most of the effort spent on researching the target company, identifying the right comparable companies, and understanding the industry.

In comparison, building the trading comps valuation model is relatively simple. For our modeling exercise, we’ll focus on the mechanics of valuing a company using trading comps analysis.

In our scenario, we’ll use the financial assumptions of five different companies.

Since we have the valuation measures and financial metrics side-by-side, calculating the LTM (Last Twelve Months) multiples should be straightforward.

The process of calculating each valuation multiple involves dividing the valuation measure by the corresponding operating metric for each company.

For example, to calculate Company A’s TEV/EBITDA, we divide the $1.4 billion TEV by the $200 million in EBITDA, resulting in 7.0x.

- Minimum: “=MIN(Range of Multiples)”

- 25th Percentile: “=QUARTILE(Range of Multiples,1)”

- Median: “=MEDIAN(Range of Multiples)”

- Mean: “=AVERAGE(Range of Multiples)”

- 75th Percentile: “=QUARTILE(Range of Multiples,3)”

- Maximum: “=MAX(Range of Multiples)”

The question of whether to include or exclude the target company from the peer group is frequently debated. Some argue that including the target skews the multiple towards the target’s current valuation.

However, excluding the target from a “market-based” valuation contradicts the idea that the market is “right” on average, given that the target is part of the peer group. Of course, if the target is a private company, it would not be included in the calculation.

10. Trading Comps Analysis: An Example

Now, let’s look at how to value the target company by applying the median and mean multiples derived from the peer group.

After calculating the appropriate valuation multiples, you can apply the median or mean multiple to the target company to get an implied valuation.

A common question is whether to use the median or the mean.

- Median: Using the median eliminates the distortion caused by outliers, which becomes more important as the number of comparable companies increases.

- Mean: The mean can be preferable when the peer group has only a few comparable companies (less than 5) and no clear outliers.

Continuing our TEV/EBITDA example, if we apply the 6.0x median TEV/EBITDA multiple to our target’s EBITDA of $140 million, the implied TEV is $833 million.

Therefore, based on the peer group median and mean, the implied valuation of the target company is approximately $833 million or $819 million, respectively, assuming the TEV/EBITDA multiple is the appropriate multiple to use.

11. FAQs About Comparable Analysis

-

### 11.1. What is the primary purpose of comparable company analysis?

To estimate the value of a company by comparing it to similar publicly traded companies.

-

### 11.2. What are the key criteria for selecting comparable companies?

Business characteristics, financials, and risks.

-

### 11.3. What is a valuation multiple?

A ratio that compares a measure of value to an operating metric.

-

### 11.4. What’s the difference between Enterprise Value and Equity Value multiples?

Enterprise Value represents the total value to all investors, while Equity Value represents the value attributable to shareholders.

-

### 11.5. Why is it important to “scrub” the financials of comparable companies?

To remove the impact of non-recurring items.

-

### 11.6. Should the target company be included in the peer group when calculating multiples?

It’s debatable, but excluding the target contradicts the idea that the market is “right” on average.

-

### 11.7. When should the median multiple be used versus the mean multiple?

The median is best when there are outliers, while the mean is preferable with few comparable companies and no outliers.

-

### 11.8. What are the limitations of comparable company analysis?

It depends on the quality of comparable companies and is susceptible to market inefficiencies.

-

### 11.9. How can comparable company analysis be used in conjunction with other valuation methods?

As a “sanity check” to ensure the valuation is reasonable.

-

### 11.10. Where can I find more detailed information and tools for performing comparable company analysis?

COMPARE.EDU.VN offers comprehensive resources and guidance.

Comparable analysis is a complex process that requires careful consideration of various factors. However, by following the steps outlined in this guide, you can effectively use this method to derive a fair valuation for your target company.

Ready to make informed decisions? Visit compare.edu.vn at 333 Comparison Plaza, Choice City, CA 90210, United States or contact us via Whatsapp at +1 (626) 555-9090 for in-depth comparisons and expert insights to help you choose wisely.