Understanding How Is Inflation In Us Compared To Other Countries is crucial for informed financial decisions, and COMPARE.EDU.VN provides the comparisons you need. By examining key economic indicators and policy responses, we shed light on the inflation landscape, offering a comparative analysis. Dive into this analysis to understand inflation trends, economic growth, and investment landscapes.

1. Introduction: The US Inflation Landscape Compared

The economic recovery following the COVID-19 pandemic has been unique across the globe, with the United States experiencing a distinctive trajectory compared to other G10 nations. Understanding how is inflation in US compared to other countries involves analyzing various factors such as fiscal support, labor market dynamics, and supply chain pressures. The U.S. adopted aggressive fiscal stimulus measures, which led to robust economic growth but also resulted in elevated inflation levels. In contrast, many other countries opted for more muted fiscal support, leading to slower growth but potentially lower inflation. This comparison highlights the trade-offs and policy choices made by different nations during the recovery period. Key concepts to consider include economic growth, inflation rates, and fiscal policy impacts.

2. The Unprecedented COVID-19 Recession and Recovery

The recession triggered by the COVID-19 pandemic was unlike any other in U.S. history. Starting in February 2020, it rapidly reached depths unseen in a century before quickly receding, lasting only two months according to the National Bureau of Economic Research. The swift and enduring U.S. recovery was jumpstarted by a combination of unprecedented fiscal support, rapid vaccine deployment, and structural economic resilience. As the economy continues to expand, two important characteristics have emerged: (i) the U.S. avoided the deep economic scarring that impacted millions of American households in the last recovery; and (ii) the U.S. recovery has far outpaced most of its G10 peer countries.

3. Avoiding Economic Scarring: A Comparison of Fiscal Policies

The prior recovery was marred by economic scarring that emerged from insufficient fiscal support for households and businesses. Following the Great Recession, consumption was very slow to return to its precrisis level, causing a large output gap to emerge, which held down inflation but also limited demand for labor. With employment depressed, millions of discouraged workers exited the labor force and many more would struggle to return to prerecession earnings levels. As a result, consumption and residential investment remained depressed and the output gap between potential and actual GDP persisted.

In the wake of the pandemic, many of the United States’ competitors repeated its mistake in the prior recovery. As the global economy remained disrupted by COVID-19 in 2021 and beyond, many foreign governments opted for premature fiscal consolidation in which the policy response was too muted and insufficient to help return their respective economies to prerecession form. By contrast, policymakers in the U.S. opted for more generous countercyclical support—including massive relief bills passed under both Democratic and Republican administrations that would provide assistance past even the omicron and delta waves of COVID-19. As a result, there is now no meaningful slack in the U.S., unlike in Europe where activity is once again falling behind its prepandemic trend. Perhaps most important, U.S. labor force participation has risen to record highs across major population groups, especially among prime-age women. Elevated inflation in 2021 and 2022 abated quickly and in recent years was driven more by supply constraints in the housing market than by fundamental imbalances in supply and demand. The steady fall in non-shelter year-over-year inflation, which now stands at just 1.1%, underscores that supply disruptions—not overheating—were by far the main driver of high inflation right after the pandemic. All told, the post-COVID recovery reaffirms the difficult choices made by policymakers and ultimately vindicates U.S. policy choices.

4. The Role of the Output Gap in the US and Other G10 Countries

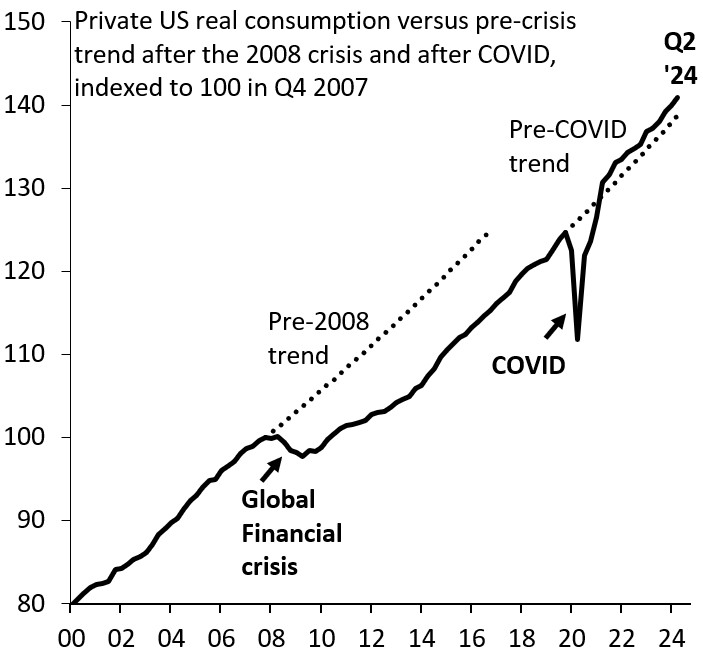

The key to the relative strength of the U.S. recovery has been the absence of a sizable output gap following the COVID-19 shock. Whereas the U.S. economy never regained its pre-2008 momentum after the global financial crisis, ample fiscal support in 2020 and 2021 helped preserve economic activity at prerecession levels save for a temporary drop following widespread lockdowns. While output gaps are notoriously difficult to measure, a simple extrapolation of the pre-2008 growth trend suggests there was substantial slack in the decade after the Great Recession (Figure 1). This large output gap meant chronically low inflation in the years that followed, but also prompted millions of discouraged workers to exit the labor force—which led to a sluggish recovery in both household balance sheets and the national housing market.

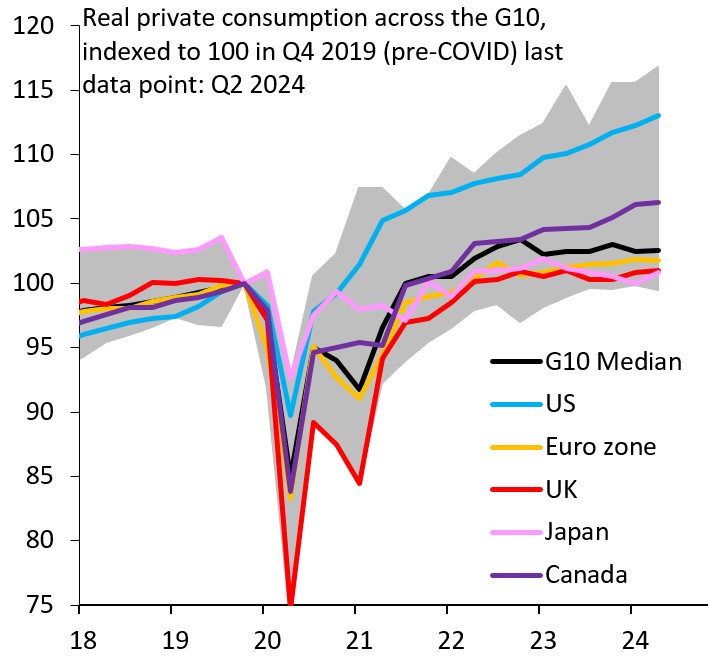

The pandemic threatened a repeat of that experience, especially as large parts of the services economy were shuttered. However, aggressive fiscal stimulus ensured that did not happen, as pandemic-relief legislation explicitly aimed to preserve payrolls while also providing generous financial and in-kind support to households. This support in the U.S. was far more generous compared to the rest of the G10 and—as a result—the U.S. has now meaningfully outperformed its peers. Indeed, private consumption has grown at a faster rate than in the rest of the G10, in absolute and per capita terms. If the U.S. economy had grown at the same rate as the G10 median since Q2 2021, U.S. GDP would be a cumulative three percentage points lower by Q2 2024. In other words, had U.S. policy not pursued its aggressive course, there would again be a material output gap.

Figure 1: Private US real consumption compared to the pre-crisis trend after the 2008 crisis and after COVID-19. Source: Haver Analytics

Figure 2: Real private consumption across the G10 nations highlights the variations in economic recovery. Source: Haver Analytics

5. Labor Market Recovery in the US vs. Other Countries

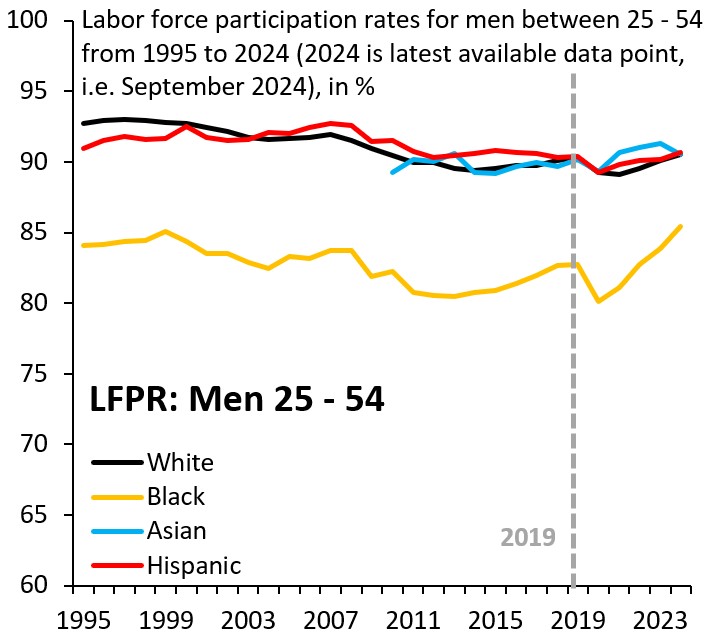

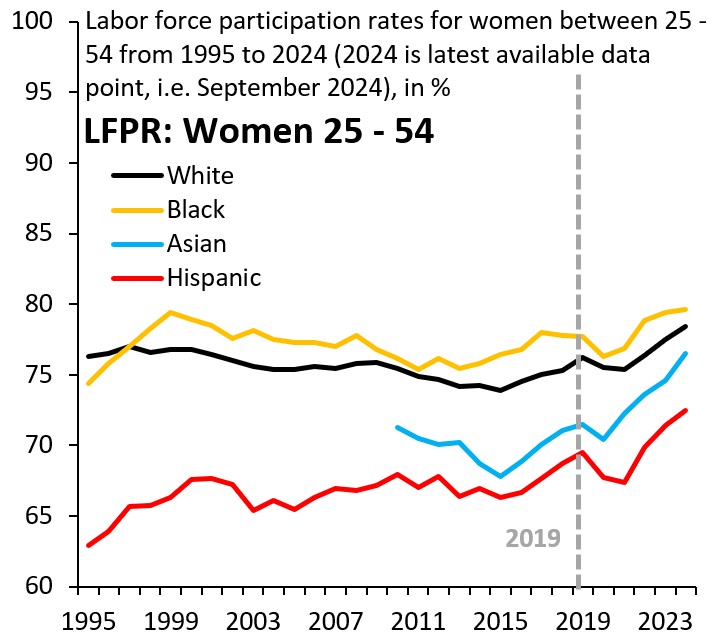

The absence of a sizable output gap in the U.S. led to a tight labor market and rapid growth in employment. Prime-age labor force participation among men and women has either fully recovered or risen above prepandemic levels. This recovery is a stark contrast from the decade after the global financial crisis, when discouraged workers exited the labor force, driving labor force participation down by several percentage points. Today the rise in prime-age female labor force participation across all demographic groups is especially notable, as women’s participation has risen to historic highs. The U.S. labor market does not exhibit the scarring that was so prominent after 2008, a remarkable success given that COVID-19 decimated many service-providing occupations.

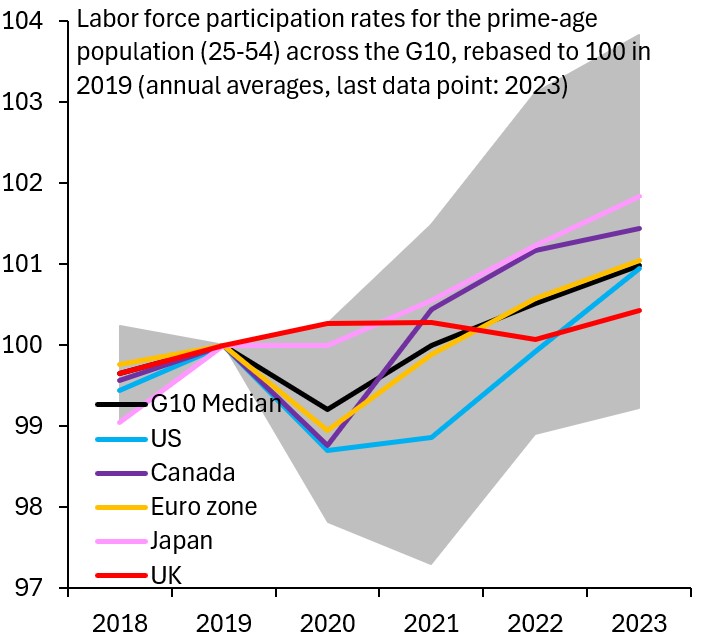

In an international comparison, the rebound in labor participation in the U.S. is especially strong following a more muted recovery in 2021. As can be seen in Figure 5 below, the decline in participation was widespread across the G10 in 2020 and the U.S. was slower to recover in 2021. However, U.S. participation rapidly rebounded in 2022 and 2023 and is now on par with G10 peers.

Figure 3: Labor force participation rates for men aged 25-54, showcasing the recovery in the U.S. labor market. Source: Haver Analytics

Figure 4: Labor force participation rates for women aged 25-54, indicating the rise in female participation to historic highs. Source: Haver Analytics

Figure 5: Labor force participation rates for the prime-age population (25-54) across the G10, highlighting the U.S. rebound. Source: Haver Analytics

6. Understanding the Inflation Trade-Off: A Detailed Analysis

The high post-pandemic inflation experienced in the U.S. can be divided into two phases. The first phase lasted from the end of the recession in April 2020 through June 2022. Here, core CPI grew at an annual rate of 4.8% and was driven largely by supply chain pressures owing to the pandemic. While many of the supply chain disruptions impacted other countries as well, weaker growth helped mute the rise in inflation relative to the U.S.

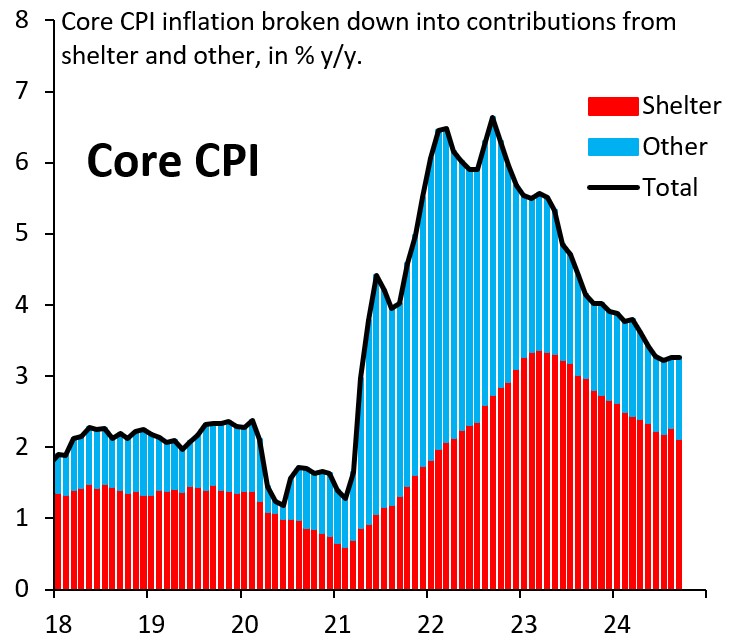

The second phase lasted from June 2022 through May 2024 and was driven primarily by rising shelter costs—not more generalized inflation. Over this period, core CPI in the U.S. was still elevated—ranging from 6.6% to 3.4% on a year-over-year basis—but the main culprit was the rising cost of housing (Figure 6). Rising housing costs were driven primarily by lack of housing construction over the pandemic and before, the result of idiosyncratic factors linked to the housing supply—such as stringent local zoning laws that depress new building and denser housing—and high mortgage rates which discouraged many incumbent homeowners from listing their homes.

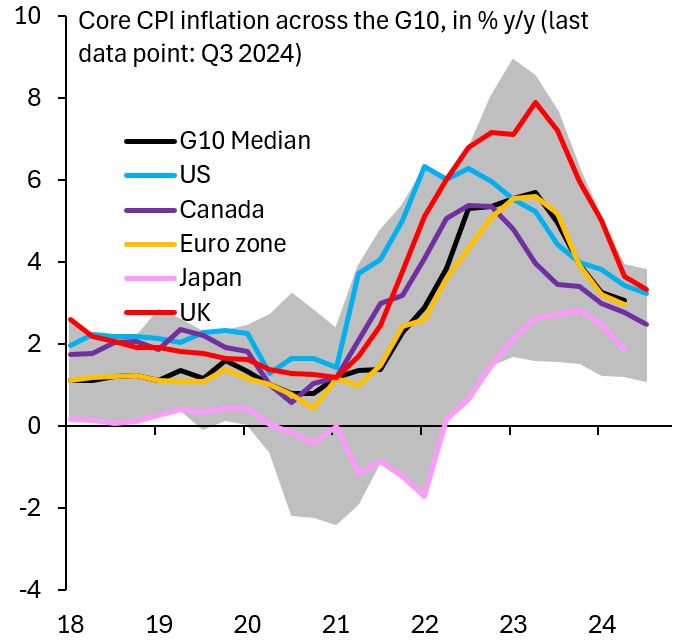

The international experience with inflation is shown in Figure 7 below. Here, inflation in the U.S. was elevated relative to the G10 for the first two years of the pandemic, but quickly reversed course at the start of 2022. Then, inflation began to fall and for a period was below the U.K., the eurozone, and the G10 median. Today, cumulative core inflation in the U.S. is approximately equal to all major competitors except Japan. However, what makes the U.S. experience so unique was that inflation was comparable across developed economies while growth in GDP, consumption, and employment was exceptional relative to competitors.

Figure 6: Core CPI inflation broken down into contributions from shelter and other factors, illustrating the impact of housing costs. Source: Haver Analytics

Figure 7: Core CPI inflation across the G10, showing the U.S. inflation relative to its peers. Source: Haver Analytics

7. The US Investment Boom: A Bright Spot in the Economy

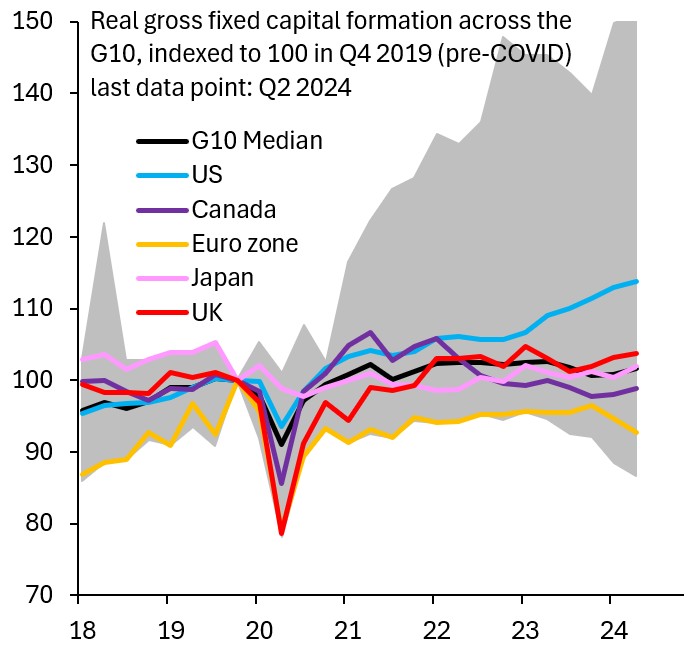

Investment in the U.S. has been a notable point of optimism relative to other G10 economies. Buoyed by the investment incentives in the Inflation Reduction Act (and to a lesser extent) the CHIPS and Science Act, coupled with broader optimism over the U.S. economy, the U.S. experienced a relative boom in investment compared to its competitors. As can be seen in Figure 8, investment—as measured by real gross capital formation—was especially high in Canada and the U.S. through 2022. Then, in 2023 and 2024, U.S. investment accelerated relative to its peers. Today, U.S. investment is 14% above its pre-COVID level, while investment in the eurozone has fallen by 7% over the same period.

The absolute rise in investment in the U.S. is especially notable when controlling for the business cycle. As noted in analysis by the U.S. Treasury Department, change in investment typically falls (as a share of GDP) in the period following a peak in the business cycle—typically falling by about 1 percentage point between six and 12 quarters from the peak. However, in the current recovery, aggregate investment has remained roughly constant—leading to an additional $430 billion in investment relative to historical norms.

Figure 8: Real gross fixed capital formation across the G10, demonstrating the U.S. investment boom. Source: Haver Analytics

8. Inflation and Monetary Policy: The US Federal Reserve’s Response

8.1 The Federal Reserve’s Dual Mandate

The Federal Reserve (also known as the Fed) operates under a dual mandate: to promote maximum employment and stable prices. These goals often require careful balancing, especially during periods of economic uncertainty like the post-pandemic recovery. The Fed’s primary tool for managing inflation is adjusting the federal funds rate, which influences interest rates throughout the economy.

8.2 Quantitative Easing and Tapering

In response to the COVID-19 pandemic, the Fed initially implemented quantitative easing (QE), purchasing large quantities of government bonds and mortgage-backed securities to inject liquidity into the financial system and lower long-term interest rates. As the economy recovered and inflation rose, the Fed began tapering these asset purchases, gradually reducing the amount of bonds it was buying.

8.3 Interest Rate Hikes

To further combat inflation, the Fed started raising the federal funds rate in early 2022. These rate hikes aimed to cool down the economy by making borrowing more expensive, thereby reducing demand and easing inflationary pressures. The pace and magnitude of these rate hikes were closely watched by economists and investors, as they can have significant impacts on economic growth and financial markets.

8.4 Forward Guidance and Communication

Effective communication is crucial for the Fed’s monetary policy. Through forward guidance, the Fed communicates its intentions, strategies, and outlook to the public, helping to shape expectations and reduce uncertainty. This communication plays a vital role in influencing financial market conditions and ensuring that the Fed’s policy actions are well understood.

8.5 Comparing the Fed’s Approach to Other Central Banks

Central banks around the world have adopted different strategies to address inflation. Some, like the Fed, have been aggressive in raising interest rates, while others have taken a more cautious approach. The effectiveness of these different strategies depends on the specific economic conditions and structural factors in each country.

Table 1: Central Bank Responses to Inflation

| Central Bank | Policy Response | Key Considerations |

|---|---|---|

| US Federal Reserve (The Fed) | Aggressive interest rate hikes | Dual mandate, strong labor market, high inflation |

| European Central Bank (ECB) | Gradual interest rate hikes | Concerns about economic growth, energy crisis, varying inflation rates across member states |

| Bank of England (BoE) | Significant interest rate hikes | High inflation, Brexit-related challenges, risk of recession |

| Bank of Japan (BoJ) | Maintaining ultra-loose monetary policy | Deflationary pressures, weak economic growth, aging population |

| Reserve Bank of Australia (RBA) | Moderate interest rate hikes | Balancing inflation with economic growth, housing market vulnerabilities |

| Bank of Canada (BoC) | Aggressive interest rate hikes | High inflation, strong economic growth, reliance on commodity exports |

9. Supply Chain Disruptions and Inflation: A Global Perspective

9.1 The Impact of Global Supply Chains

The COVID-19 pandemic exposed vulnerabilities in global supply chains, leading to widespread disruptions and shortages. These disruptions played a significant role in driving up inflation, as businesses faced higher costs for raw materials, components, and transportation. The interconnected nature of global supply chains meant that disruptions in one region could have ripple effects around the world.

9.2 Comparing Supply Chain Resilience

Some countries were better positioned to weather supply chain disruptions than others. Factors such as domestic production capacity, diversification of suppliers, and investment in logistics infrastructure influenced a country’s resilience. For example, countries with strong domestic manufacturing sectors were less reliant on imports and therefore less vulnerable to disruptions.

9.3 Policy Responses to Supply Chain Challenges

Governments and businesses adopted various strategies to mitigate the impact of supply chain disruptions. These included diversifying suppliers, increasing inventory levels, reshoring production, and investing in technology to improve supply chain visibility and efficiency.

9.4 The Role of Geopolitical Factors

Geopolitical tensions and trade disputes further complicated supply chain dynamics. Trade barriers, sanctions, and political instability added to the challenges of sourcing goods and materials, contributing to higher costs and inflation.

Table 2: Strategies for Mitigating Supply Chain Disruptions

| Strategy | Description | Benefits | Challenges |

|---|---|---|---|

| Diversifying Suppliers | Sourcing goods and materials from a wider range of suppliers | Reduces reliance on any single supplier, mitigating the impact of disruptions | Requires more complex supply chain management, may increase costs |

| Increasing Inventory Levels | Holding larger stocks of key materials and components | Provides a buffer against shortages, ensuring continuity of production | Increases storage costs, ties up capital, risk of obsolescence |

| Reshoring Production | Bringing manufacturing back to the home country | Reduces reliance on foreign suppliers, creates domestic jobs, strengthens domestic economy | May increase production costs, requires investment in infrastructure and skills |

| Investing in Technology | Using technology such as blockchain, IoT, and AI to improve supply chain visibility and efficiency | Enhances transparency, improves forecasting, optimizes logistics, reduces costs | Requires significant investment, may face integration challenges, requires skilled workforce |

| Building Strategic Reserves | Governments maintaining stockpiles of critical goods and materials | Ensures availability of essential supplies during emergencies, enhances national security | Requires significant investment, storage costs, risk of spoilage or obsolescence |

10. Housing Costs and Inflation: A Closer Look at the US Market

10.1 The Role of Housing in Inflation

Housing costs are a significant component of the Consumer Price Index (CPI) and play a crucial role in overall inflation. In the US, rising rents and home prices have contributed significantly to inflationary pressures in recent years.

10.2 Factors Driving Up Housing Costs

Several factors have contributed to rising housing costs, including:

- Limited Housing Supply: A shortage of available housing, particularly in high-demand areas, has driven up prices and rents.

- Increased Demand: Demographic trends, such as population growth and household formation, have increased demand for housing.

- Low Interest Rates: Historically low interest rates have made mortgages more affordable, increasing demand and driving up prices.

- Supply Chain Issues: Disruptions to supply chains have increased the cost of building materials, further limiting housing supply.

- Zoning Regulations: Restrictive zoning regulations and land-use policies have limited the construction of new housing in many areas.

10.3 Comparing Housing Affordability Across Countries

Housing affordability varies significantly across countries. Factors such as income levels, housing supply, interest rates, and government policies influence affordability. Some countries have implemented policies to address housing affordability, such as rent controls, subsidies for first-time homebuyers, and incentives for developers to build affordable housing.

Table 3: Factors Influencing Housing Affordability

| Factor | Impact on Housing Affordability | Examples of Government Policies |

|---|---|---|

| Income Levels | Higher incomes increase affordability, while lower incomes decrease affordability | Minimum wage laws, income tax policies, social welfare programs |

| Housing Supply | Increased supply improves affordability, while limited supply reduces affordability | Zoning reforms, incentives for developers, public housing programs |

| Interest Rates | Lower interest rates improve affordability, while higher interest rates decrease affordability | Monetary policy, mortgage interest tax deductions, government-backed mortgage programs |

| Government Policies | Policies can either improve or worsen affordability, depending on their design and implementation | Rent controls, subsidies for first-time homebuyers, property taxes, land-use regulations |

| Demographic Trends | Population growth and household formation increase demand, potentially reducing affordability | Immigration policies, urban planning strategies, incentives for developers to build affordable housing in growing areas |

10.4 Policy Options for Addressing Housing Inflation

Addressing housing inflation requires a multi-faceted approach that includes increasing housing supply, addressing demand factors, and implementing policies to improve affordability. Some potential policy options include:

- Zoning Reform: Relaxing zoning regulations to allow for denser housing development.

- Incentives for Affordable Housing: Providing incentives for developers to build affordable housing units.

- Rent Controls: Implementing rent controls to limit rent increases.

- Subsidies for First-Time Homebuyers: Providing subsidies to help first-time homebuyers afford a down payment.

- Investment in Public Housing: Increasing investment in public housing programs.

11. The Role of Government Spending and Fiscal Policy

11.1 Fiscal Policy vs. Monetary Policy

Fiscal policy refers to the use of government spending and taxation to influence the economy, while monetary policy refers to actions taken by the central bank to manage the money supply and interest rates. Fiscal policy can be used to stimulate economic growth, combat inflation, or address other economic challenges.

11.2 The Impact of Government Spending on Inflation

Increased government spending can boost demand, potentially leading to higher inflation, especially if the economy is already operating near full capacity. However, government spending can also increase supply by investing in infrastructure, education, and technology, which can help to offset inflationary pressures.

11.3 Comparing Fiscal Policies Across Countries

Countries have adopted different fiscal policies in response to the COVID-19 pandemic. Some countries have implemented large stimulus packages, while others have taken a more cautious approach. The effectiveness of these different fiscal policies depends on the specific economic conditions and structural factors in each country.

11.4 The Sustainability of Government Debt

Increased government spending can lead to higher levels of government debt. The sustainability of government debt depends on factors such as economic growth, interest rates, and the government’s ability to manage its finances. High levels of government debt can create risks for the economy, such as higher interest rates, inflation, and financial instability.

Table 4: Impact of Government Spending on Inflation

| Type of Government Spending | Impact on Demand | Impact on Supply | Overall Impact on Inflation | Examples |

|---|---|---|---|---|

| Infrastructure Investment | Increases demand for construction materials and labor | Increases supply of transportation, energy, and communication infrastructure | Ambiguous; depends on the magnitude of the spending and the capacity of the economy to absorb it | Building highways, bridges, and airports |

| Education Spending | Increases demand for educational services and resources | Increases supply of skilled labor | Ambiguous; depends on the effectiveness of the spending and the responsiveness of the labor market | Funding schools, colleges, and vocational training programs |

| Research and Development (R&D) Spending | Increases demand for R&D services and equipment | Increases supply of new technologies and innovations | Ambiguous; depends on the success of the R&D projects and their impact on productivity | Supporting basic and applied research |

| Social Welfare Programs (e.g., unemployment benefits, food stamps) | Increases demand by providing income support to households | Little direct impact on supply | Increases inflation by boosting demand, especially if the economy is near full capacity | Providing unemployment benefits and food stamps |

| Defense Spending | Increases demand for military equipment and personnel | Little direct impact on supply | Increases inflation by boosting demand, especially if the economy is near full capacity | Purchasing military equipment and paying soldiers |

12. The Impact of the Russia-Ukraine War on Global Inflation

12.1 Disruption of Energy and Food Supplies

The Russia-Ukraine war has had a significant impact on global inflation by disrupting energy and food supplies. Russia is a major exporter of oil, natural gas, and coal, while Ukraine is a major exporter of wheat, corn, and vegetable oils. The war has led to reduced exports from both countries, causing prices for these commodities to rise sharply.

12.2 Impact on Energy Prices

The war has caused a spike in energy prices, particularly in Europe, which relies heavily on Russian natural gas. Higher energy prices have increased costs for businesses and consumers, contributing to overall inflation.

12.3 Impact on Food Prices

The war has also caused a spike in food prices, particularly for wheat and vegetable oils. Ukraine is a major exporter of these commodities, and the war has disrupted planting and harvesting activities, leading to reduced supplies. Higher food prices have disproportionately affected low-income countries and households, which spend a larger share of their income on food.

12.4 Policy Responses to the War’s Impact

Governments have adopted various policies to mitigate the impact of the war on inflation. These include:

- Releasing Strategic Reserves: Releasing strategic reserves of oil and natural gas to increase supply and lower prices.

- Diversifying Energy Sources: Investing in renewable energy and diversifying energy sources to reduce reliance on Russian gas.

- Supporting Farmers: Providing financial support to farmers to help them increase production of wheat and other crops.

- Providing Food Aid: Providing food aid to low-income countries and households to help them cope with higher food prices.

Table 5: Policy Responses to the Russia-Ukraine War’s Impact on Inflation

| Policy Response | Description | Benefits | Challenges |

|---|---|---|---|

| Releasing Strategic Reserves | Releasing strategic reserves of oil and natural gas to increase supply and lower prices | Increases supply, reduces prices | Reserves are limited, may not be sustainable in the long term |

| Diversifying Energy Sources | Investing in renewable energy and diversifying energy sources to reduce reliance on Russian gas | Reduces reliance on Russia, promotes energy independence | Requires significant investment, may take time to develop new energy sources |

| Supporting Farmers | Providing financial support to farmers to help them increase production of wheat and other crops | Increases supply of food, supports farmers | May be costly, may not be effective if weather conditions are unfavorable |

| Providing Food Aid | Providing food aid to low-income countries and households to help them cope with higher food prices | Helps vulnerable populations, prevents food insecurity | May be costly, may create dependency |

13. Future Outlook: What to Expect in the Coming Years

13.1 Factors That Will Influence Inflation

Several factors will influence inflation in the coming years, including:

- Monetary Policy: The actions of central banks will play a key role in managing inflation.

- Fiscal Policy: Government spending and taxation policies will also influence inflation.

- Supply Chain Developments: The resolution of supply chain disruptions will help to ease inflationary pressures.

- Geopolitical Factors: Geopolitical tensions and trade disputes could continue to disrupt supply chains and increase inflation.

- Wage Growth: Rising wages could contribute to inflation if they outpace productivity growth.

13.2 Potential Scenarios

Several potential scenarios could play out in the coming years:

- Scenario 1: Soft Landing: Central banks successfully manage to bring inflation down without causing a recession.

- Scenario 2: Recession: Aggressive monetary policy leads to a recession, which in turn brings down inflation.

- Scenario 3: Stagflation: Inflation remains high while economic growth stagnates.

- Scenario 4: Deflation: The economy enters a period of deflation, with falling prices and wages.

13.3 Implications for Investors and Consumers

The future path of inflation will have significant implications for investors and consumers. Investors will need to adjust their portfolios to account for changing inflation expectations. Consumers will need to manage their budgets carefully to cope with rising prices.

Table 6: Potential Scenarios for Inflation in the Coming Years

| Scenario | Description | Implications for Investors | Implications for Consumers |

|---|---|---|---|

| Soft Landing | Central banks successfully manage to bring inflation down without causing a recession | Equities may perform well, but bond yields may rise | Consumers may see moderate price increases, but the economy will remain healthy |

| Recession | Aggressive monetary policy leads to a recession, which in turn brings down inflation | Equities may perform poorly, but bond yields may fall | Consumers may face job losses and lower wages, but prices will eventually fall |

| Stagflation | Inflation remains high while economic growth stagnates | Equities and bonds may perform poorly | Consumers may face high prices and job losses |

| Deflation | The economy enters a period of deflation, with falling prices and wages | Bonds may perform well, but equities may perform poorly | Consumers may see falling prices, but wages may also fall, leading to lower overall demand |

14. Conclusion: Key Takeaways and Future Considerations

In conclusion, the U.S. recovery from the COVID-19 pandemic has been unique compared to other G10 countries. The aggressive fiscal stimulus adopted by the U.S. led to robust economic growth and a tight labor market but also resulted in elevated inflation levels. In contrast, many other countries opted for more muted fiscal support, leading to slower growth but potentially lower inflation. Going forward, policymakers will need to carefully balance the goals of maintaining economic growth and controlling inflation. Supply chain developments, geopolitical factors, and wage growth will also play a key role in determining the future path of inflation.

Understanding how is inflation in US compared to other countries requires analyzing various factors and policy choices. COMPARE.EDU.VN provides comprehensive comparisons to help you make informed decisions.

Make smarter choices with COMPARE.EDU.VN. Visit our website at compare.edu.vn to explore more comparisons and gain the insights you need. Our team at 333 Comparison Plaza, Choice City, CA 90210, United States, is here to assist you. Contact us via Whatsapp at +1 (626) 555-9090 for personalized support.

15. FAQ Section: Understanding Inflation and Its Impact

15.1 What is inflation?

Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling.

15.2 What causes inflation?

Inflation can be caused by various factors, including increased demand, supply chain disruptions, and expansionary monetary and fiscal policies.

15.3 How is inflation measured?

Inflation is commonly measured using the Consumer Price Index (CPI) or the Personal Consumption Expenditures (PCE) price index.

15.4 What is the Federal Reserve’s role in controlling inflation?

The Federal Reserve (the Fed) uses monetary policy tools, such as adjusting interest rates, to manage inflation and maintain price stability.

15.5 How does inflation affect consumers?

Inflation reduces the purchasing power of consumers, making goods and services more expensive.

15.6 How does inflation affect businesses?

Inflation can increase businesses’ costs but also potentially increase their revenues if they can raise prices.

15.7 What is the difference between core inflation and headline inflation?

Core inflation excludes volatile food and energy prices, providing a more stable measure of underlying inflation trends. Headline inflation includes all items in the CPI.

15.8 What is stagflation?

Stagflation is a condition of slow economic growth and relatively high unemployment (economic stagnation) accompanied by rising prices (inflation).

15.9 What are some strategies to protect against inflation?

Strategies to protect against inflation include investing in assets that tend to hold their value during inflationary periods, such as real estate, commodities, and inflation-indexed securities.

15.10 How does globalization impact inflation?

Globalization can impact inflation by increasing competition, lowering production costs, and facilitating supply chain efficiencies, but also by making economies more susceptible to global shocks.