UnitedHealthcare and Blue Cross Blue Shield (BCBS) both provide extensive health coverage nationwide, but key differences exist. COMPARE.EDU.VN offers a detailed comparison, exploring network size, customer satisfaction, and plan options to help you make an informed choice. Discover which provider aligns best with your healthcare needs by examining factors like healthcare programs, health insurance marketplace options, and supplemental health insurance.

1. Understanding UnitedHealthcare and Blue Cross Blue Shield

Both UnitedHealthcare and Blue Cross Blue Shield (BCBS) are major players in the health insurance industry, offering a wide range of plans and services. Knowing their backgrounds can provide valuable context for comparing them.

1.1. UnitedHealthcare History

UnitedHealthcare’s parent company, UnitedHealth Group, was founded in 1977 by Richard Burke, who was then a health analyst at InterStudy. Burke collaborated with Dr. Paul Ellwood, a pioneer of the health maintenance organization (HMO) model, which aimed to reduce healthcare costs by changing how medical providers were compensated. This innovative approach laid the foundation for UnitedHealthcare’s growth and its focus on managed care solutions.

1.2. Blue Cross Blue Shield History

Blue Cross’s origins trace back to 1929 at Baylor University Hospital. Hospital administrators created a prepayment plan for Dallas public school teachers struggling to afford healthcare. For 50 cents per month, teachers secured coverage for up to 21 days of hospitalization per year. Blue Shield soon followed, with employers in the Pacific Northwest arranging for employees to receive care from specific medical practitioners for a monthly premium.

In the 1940s, Blue Cross and Blue Shield began partnering to offer more comprehensive major medical coverage to their members. The two formally merged to form the Blue Cross Blue Shield Association in 1982. As of 2024, the BCBSA includes 33 independent companies, each operating in specific regions. This decentralized structure allows for localized service but can also lead to variations in customer experience.

2. UnitedHealthcare vs. Blue Cross Blue Shield: A Detailed Comparison

To effectively evaluate “how does UnitedHealthcare compare to Blue Cross,” let’s examine several key aspects of their offerings. This comparison will cover plan structures, availability, network size, costs, coverage limits, policy management, and customer satisfaction.

2.1. Plan Structures

Both UnitedHealthcare and Blue Cross Blue Shield offer a diverse range of health insurance plans, catering to different needs and preferences. These include:

- HMO (Health Maintenance Organization): Requires members to choose a primary care physician (PCP) who coordinates their care and provides referrals to specialists.

- PPO (Preferred Provider Organization): Offers more flexibility, allowing members to see doctors and specialists without referrals, but at a higher cost for out-of-network care.

- EPO (Exclusive Provider Organization): Similar to HMOs but does not require a PCP. Members must stay within the network for coverage.

- POS (Point of Service): A hybrid of HMO and PPO, requiring a PCP but allowing out-of-network care with a referral (often at a higher cost).

- HMO-POS: Combines features of HMO and POS plans.

- CDHP (Consumer-Driven Health Plan): High-deductible health plans often paired with a health savings account (HSA) or flexible spending account (FSA).

- FSA (Flexible Spending Account): A pre-tax account used to pay for eligible healthcare expenses.

- HDHP (High-Deductible Health Plan): A health plan with a higher deductible than a traditional insurance plan.

- HSA (Health Savings Account): A tax-advantaged savings account used to pay for qualified medical expenses.

- Indemnity: Traditional health insurance that allows members to see any doctor or specialist without referrals, but typically has higher premiums.

- Medicaid: A government-funded health insurance program for low-income individuals and families.

- Medicare: A federal health insurance program for people 65 or older, certain younger people with disabilities, and people with End-Stage Renal Disease.

- SNP (Special Needs Plan): A Medicare Advantage plan designed for individuals with specific health conditions or needs.

| Feature | UnitedHealthcare | Blue Cross Blue Shield |

|---|---|---|

| Plan Structures | HMO, PPO, EPO, POS, HMO-POS, CDHP, FSA, HDHP, HSA, Indemnity, Medicaid, Medicare, SNP | HMO, PPO, EPO, POS, HMO-POS, CDHP, FSA, HDHP, HSA, Indemnity, Medicaid, Medicare, SNP |

| Availability | 50 states + D.C. and U.S. Virgin Islands | 50 states + D.C. and Puerto Rico |

| Coverage Limit | Varies | Varies |

| Deductible | Varies | Varies |

| Maximum Benefit | Varies | Varies |

| Waiting Period | Varies | Varies |

| Telehealth | Yes | Yes |

| Policy Management | Mobile app, online account, phone | Mobile app, online account, phone |

2.2. Plan Availability

Both UnitedHealthcare and Blue Cross Blue Shield offer widespread availability, providing coverage in all 50 states, the District of Columbia, and select U.S. territories. UnitedHealthcare extends its reach to the U.S. Virgin Islands, while Blue Cross Blue Shield serves Puerto Rico. The availability of specific plans may vary by state.

2.3. In-Network Providers

The size of a health insurance company’s network is a crucial factor to consider. A larger network provides members with more choices and greater access to healthcare providers.

Blue Cross Blue Shield boasts the largest domestic network in the United States, with 1.7 million in-network providers. This extensive network ensures that members have access to a wide range of doctors, specialists, and hospitals across the country.

UnitedHealthcare also has a substantial network, with over 1.3 million doctors and healthcare professionals across more than 6,700 hospitals and medical facilities. While smaller than BCBS’s network, it still offers a significant number of options for members.

Choosing between these two insurers often hinges on whether your preferred doctors are in-network. Always verify network participation before enrolling.

2.4. Cost

Health insurance costs vary considerably based on factors such as coverage needs, location, age, and plan type. It’s challenging to provide average premium comparisons between UnitedHealthcare and Blue Cross Blue Shield due to these variables.

In 2024, the average monthly premium for a Marketplace benchmark plan is $477, while Medicare Advantage plans average $18.50 per month. These figures offer a general sense of health insurance costs, but individual rates will differ.

The Affordable Care Act (ACA) limits the factors that insurers can use to determine premiums:

- Age

- Location

- Tobacco use

- Individual vs. family plan

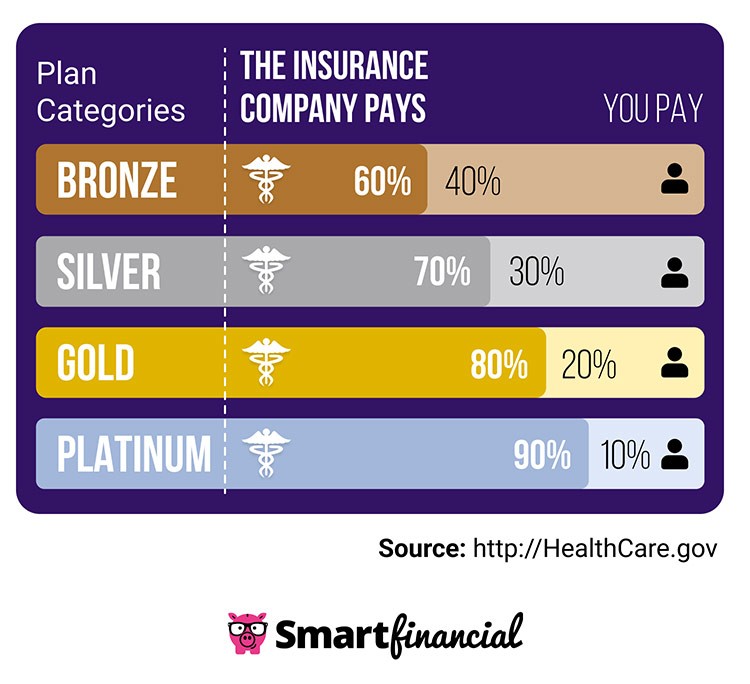

- Plan metal level (e.g., Bronze, Silver, Gold, Platinum)

To determine the most affordable option for you, it’s essential to compare specific plans and consider your individual healthcare needs and budget.

2.5. Coverage Limits

Coverage limits also vary from plan to plan, and finding one that matches your needs and budget is important. ACA-compliant plans cannot place limits on essential health benefits, including:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services and devices

- Laboratory services

- Preventive and wellness services and chronic disease management

- Pediatric services (including dental and vision care for children)

2.6. Policy Management

Both UnitedHealthcare and Blue Cross Blue Shield offer multiple ways to manage your policy, including by phone, online portal, or mobile app.

Blue Cross Blue Shield companies generally have their own mobile apps, so the user experience may vary depending on your location.

| App | Google Play Store Rating | Apple App Store Rating |

|---|---|---|

| UnitedHealthcare | 4.6/5 stars | 4.7/5 stars |

| Blue Connect Mobile NC | 4/5 stars | 4.3/5 stars |

| Blue Shield of California | 3.9/5 stars | 4.8/5 stars |

2.7. Medical Loss Ratio

ACA-compliant health insurers selling individual or small group health insurance must maintain a three-year rolling average medical loss ratio (MLR) of 80%. This means they must spend 80% of premium dollars on healthcare costs rather than administrative expenses or profits. Large group coverage carriers must have an MLR of 85%. Insurers failing to meet these standards must issue rebates to policyholders.

UnitedHealthcare and other UnitedHealth Group companies issued rebates in several states and markets in 2023. Eligibility for rebates among Blue Cross Blue Shield plan members varies, as each BCBS company operates independently.

2.8. Enrollment Process

Enrollment in UnitedHealthcare or Blue Cross Blue Shield plans typically occurs during open enrollment periods. For Health Insurance Marketplace plans, open enrollment generally runs from November 1 to January 15 in most states. Medicare Advantage plans have their own enrollment periods:

| Enrollment Period | What You Can Do |

|---|---|

| Three months before to three months after your Medicare coverage starts | Enroll in a Medicare Advantage plan if you’ve already signed up for Medicare Parts A and B. |

| October 15 to December 7 | Switch from Original Medicare to Medicare Advantage, switch between Medicare Advantage plans, or drop Medicare Advantage and return to Original Medicare. |

| January 1 to March 31 (or during your first three months on Medicare) | Switch between Medicare Advantage plans or drop Medicare Advantage and return to Original Medicare. |

Special Enrollment Periods (SEP) allow enrollment outside of the standard periods if you experience a qualifying life event, such as:

- Getting married, divorced, or separated

- Giving birth to or adopting a child

- Changing or losing your job

- Moving to a new home

- Losing existing health coverage due to a family member’s death

- Turning 26 and aging out of a parent’s health plan

- Becoming a U.S. citizen

- Leaving prison

2.9. Policyholder Experience

Customer satisfaction is a critical factor when choosing a health insurance provider. Blue Cross Blue Shield generally receives higher customer satisfaction ratings compared to UnitedHealthcare.

A 2024 J.D. Power study found that BCBS companies had the highest customer satisfaction ratings among health insurers in eight regions:

- Colorado

- Delaware/West Virginia/Washington, D.C.

- Heartland

- Illinois/Indiana

- Michigan

- New Jersey

- Northeast

- Southwest

UnitedHealthcare was not the highest-rated insurer in any region. The Better Business Bureau (BBB) gives Blue Cross Blue Shield an A+ rating, while UnitedHealthcare receives an F.

| Review Platform | UnitedHealthcare Rating | BCBS Rating |

|---|---|---|

| Better Business Bureau | No star rating | 1.13/5 stars |

| Best Company | 2/5 stars | 3.1/5 stars |

2.10. Filing Claims

UnitedHealthcare allows members to submit insurance claims through an online portal. The claims process for Blue Cross Blue Shield varies, but typically involves filling out a claim form and sending it to your BCBS company.

In-network providers usually file claims for you, but you may be responsible for filing claims if you visit an out-of-network provider.

3. Pros and Cons: UnitedHealthcare

Evaluating the advantages and disadvantages of each insurer provides a balanced perspective.

| Pros | Cons |

|---|---|

| Offers all major types of health insurance and operates nationwide | Slightly smaller provider network than Blue Cross Blue Shield |

| Mobile app has great reviews | Poor rating by the Better Business Bureau |

| Convenient online claims process available for all members |

4. Pros and Cons: Blue Cross Blue Shield

Understanding the strengths and weaknesses of Blue Cross Blue Shield helps in making an informed decision.

| Pros | Cons |

|---|---|

| Offers all major types of health insurance and operates nationwide | Mobile app, claims process, and other aspects of the customer experience can vary from state to state due to independent operation |

| Network includes 1.7 million providers | |

| Highest customer satisfaction rating in eight regions |

5. Making the Right Choice

Deciding between UnitedHealthcare and Blue Cross Blue Shield depends on your individual circumstances. If network size and customer satisfaction are paramount, BCBS may be the better choice. If you prioritize a highly-rated mobile app and a streamlined online claims process, UnitedHealthcare could be a good fit.

Visit COMPARE.EDU.VN for more detailed comparisons and to find the health insurance plan that best suits your needs. Our comprehensive resources help you make confident and informed decisions about your healthcare coverage.

COMPARE.EDU.VN is located at 333 Comparison Plaza, Choice City, CA 90210, United States. Contact us via Whatsapp at +1 (626) 555-9090.

6. Frequently Asked Questions (FAQs)

6.1. Is Blue Cross Blue Shield better than UnitedHealthcare?

Blue Cross Blue Shield is often considered slightly better due to its larger network and higher customer satisfaction ratings. However, the best choice depends on individual needs and preferences.

6.2. Who owns UnitedHealthcare?

UnitedHealthcare is a subsidiary of UnitedHealth Group.

6.3. Is UnitedHealthcare a good network?

Yes, UnitedHealthcare has a strong network that includes 1.3 million healthcare professionals.

6.4. How do I compare plans from UnitedHealthcare and Blue Cross Blue Shield?

Visit COMPARE.EDU.VN to compare plans side-by-side, considering factors like premiums, deductibles, and network coverage.

6.5. What factors affect the cost of health insurance?

Factors include age, location, tobacco use, individual or family plan, and plan metal level.

6.6. What are essential health benefits?

Essential health benefits include ambulatory patient services, emergency services, hospitalization, pregnancy care, mental health services, prescription drugs, and more.

6.7. How do I file a claim with UnitedHealthcare?

Submit claims through the online portal.

6.8. How do I file a claim with Blue Cross Blue Shield?

The process varies, but generally involves filling out a claim form and sending it to your BCBS company.

6.9. What is a Medical Loss Ratio (MLR)?

It’s the percentage of premium dollars an insurer spends on healthcare costs versus administrative expenses and profits.

6.10. When can I enroll in a health insurance plan?

Typically during open enrollment or a special enrollment period if you qualify.

7. Expert Insights on Choosing the Right Health Plan

Selecting the right health insurance plan involves more than just comparing costs. It requires a thorough understanding of your healthcare needs, risk tolerance, and financial situation. Experts recommend the following steps to make an informed decision:

-

Assess Your Healthcare Needs: Consider your medical history, current health status, and anticipated healthcare needs for the coming year. Do you have chronic conditions that require frequent doctor visits? Are you planning any major medical procedures or surgeries?

-

Evaluate Plan Types: Understand the differences between HMOs, PPOs, EPOs, and POS plans. HMOs typically have lower premiums but require you to choose a primary care physician and obtain referrals for specialists. PPOs offer more flexibility but may have higher out-of-pocket costs.

-

Check Network Coverage: Ensure that your preferred doctors, specialists, and hospitals are included in the plan’s network. Out-of-network care can be significantly more expensive.

-

Compare Costs: Consider premiums, deductibles, copays, and coinsurance. A plan with a lower premium may have a higher deductible, meaning you’ll pay more out-of-pocket before coverage kicks in.

-

Review Coverage Details: Understand what services are covered and any limitations or exclusions. Pay attention to coverage for prescription drugs, mental health services, and preventive care.

-

Read Customer Reviews: Research customer satisfaction ratings and reviews for different insurers. This can provide insights into the quality of customer service and claims processing.

-

Seek Professional Advice: If you’re unsure which plan is right for you, consider consulting with a health insurance broker or advisor. They can help you navigate the complex world of health insurance and find a plan that meets your needs and budget.

By following these steps and carefully evaluating your options, you can choose a health insurance plan that provides the coverage and peace of mind you need.

8. The Role of Telehealth in Modern Health Insurance

Telehealth, also known as telemedicine, has become an increasingly important component of modern health insurance plans. It allows patients to consult with doctors and other healthcare providers remotely, using video conferencing, phone calls, or mobile apps. Telehealth offers several benefits:

- Convenience: Patients can receive care from the comfort of their homes, saving time and travel costs.

- Accessibility: Telehealth expands access to care for individuals in rural areas or with mobility issues.

- Cost-Effectiveness: Telehealth visits are often less expensive than in-person visits.

- Timeliness: Patients can often schedule telehealth appointments more quickly than in-person appointments.

Both UnitedHealthcare and Blue Cross Blue Shield offer telehealth services as part of their health insurance plans. These services may include:

- Virtual Doctor Visits: Consultations with primary care physicians or specialists via video conferencing.

- Mental Health Counseling: Therapy sessions with licensed therapists or counselors via video conferencing or phone calls.

- Remote Monitoring: Use of wearable devices or mobile apps to track vital signs and other health data.

- Chronic Disease Management: Support for individuals with chronic conditions such as diabetes or heart disease.

When comparing health insurance plans, consider the availability and scope of telehealth services. Telehealth can be a valuable tool for managing your health and accessing care when you need it.

9. Navigating the Health Insurance Marketplace

The Health Insurance Marketplace, also known as the exchange, is a government-run platform where individuals and families can shop for and enroll in health insurance plans. The Marketplace offers several benefits:

- Choice: You can compare plans from different insurers side-by-side.

- Financial Assistance: You may be eligible for subsidies to help lower your monthly premiums.

- Standardized Coverage: All plans offered on the Marketplace must cover essential health benefits.

- Enrollment Assistance: You can receive help from trained navigators or brokers.

To enroll in a plan through the Health Insurance Marketplace, you’ll need to provide information about your income, household size, and health status. You can then compare plans based on premiums, deductibles, coverage details, and network.

Both UnitedHealthcare and Blue Cross Blue Shield offer plans on the Health Insurance Marketplace. When choosing a plan, consider your healthcare needs, budget, and eligibility for financial assistance.

10. Supplemental Health Insurance: Filling the Gaps

Supplemental health insurance plans can help fill the gaps in your primary health insurance coverage. These plans provide additional benefits for specific healthcare needs, such as:

- Dental Insurance: Covers dental care services like cleanings, fillings, and orthodontics.

- Vision Insurance: Covers vision care services like eye exams, glasses, and contact lenses.

- Critical Illness Insurance: Provides a lump-sum payment if you’re diagnosed with a serious illness like cancer or heart attack.

- Accident Insurance: Provides coverage for medical expenses resulting from an accident.

- Hospital Indemnity Insurance: Pays a fixed amount for each day you’re hospitalized.

Supplemental health insurance plans can help you manage out-of-pocket costs and provide financial protection in case of unexpected healthcare expenses.

Both UnitedHealthcare and Blue Cross Blue Shield offer supplemental health insurance plans. Consider your individual healthcare needs and risk tolerance when deciding whether to purchase supplemental coverage.

By carefully considering these factors and comparing your options, you can choose a health insurance plan that meets your needs and provides the coverage and peace of mind you deserve. Remember to visit COMPARE.EDU.VN for more information and resources to help you make informed decisions about your healthcare coverage.

Remember, compare.edu.vn is your trusted resource for comparing health insurance options and making informed decisions. We are located at 333 Comparison Plaza, Choice City, CA 90210, United States. Contact us via Whatsapp at +1 (626) 555-9090.