It’s natural to wonder how your financial standing measures up against others, especially your peers. This article delves into net worth percentiles and averages across different age groups, providing a comprehensive benchmark for comparison. The data is based on the Federal Reserve’s 2022 Survey of Consumer Finances, offering valuable insights into wealth distribution in the United States.

Understanding Net Worth and the Data

Before diving into the comparisons, it’s crucial to understand how “family” or “household” is defined in this context. According to the Federal Reserve, a household is divided into a primary economic unit (PEU), representing the economically dominant individual or couple and their financially dependent members. This distinction helps clarify the unit of analysis for the net worth data. Net worth, itself, represents the difference between your assets (what you own) and your liabilities (what you owe).

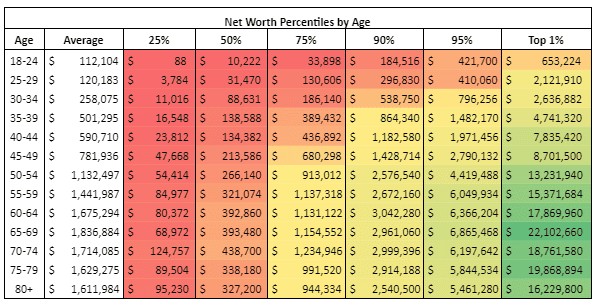

Net Worth Percentiles Across Age Groups

The following table illustrates net worth percentiles and averages for various age ranges. The average net worth for each age group is presented alongside the 25th, 50th (median), 75th, 90th, 95th, and 99th percentiles. Note the significant difference between the average and median net worth, highlighting the impact of high-wealth individuals on the average.

To visualize these figures, let’s examine several graphs. The first compares the average and median net worth by age. The average consistently surpasses the median, peaking in the late 60s, while the median peaks slightly later in the early 70s. This disparity underscores the skewed nature of wealth distribution, where a small percentage holds a disproportionate share of the total wealth.

Next, we compare the 25th, 50th, and 75th percentiles. All three peak in the early 70s, but the gap between the 75th and 50th percentile is notably larger than the gap between the 50th and 25th. This reflects the growing concentration of wealth at the higher end of the spectrum.

Finally, the 90th, 95th, and 99th percentiles are analyzed. The 90th percentile remains relatively stable between the early 50s and 80s, hovering around $2.5 million to $3 million. The 95th percentile experiences a slight peak just under $7 million in the late 60s, while the 99th percentile shows a sharp rise, peaking at over $22 million in the late 60s before declining.

Investable Net Worth: Excluding Home Equity

Now, let’s examine investable net worth, which excludes home equity. While not a complete measure of wealth, it offers insights into potential investment returns, as home equity typically doesn’t generate cash flow.

The patterns observed in total net worth are largely mirrored in investable net worth, with some key distinctions. Notably, the 25th and 50th percentiles peak at significantly lower values for investable net worth compared to total net worth. This difference diminishes as we move towards higher percentiles, indicating that home equity plays a smaller role in the wealth composition of the affluent.

The Role of Home Equity in Net Worth

By comparing the data on total and investable net worth, we can estimate average home equity across different age and net worth percentiles. Several patterns emerge:

-

Average and median home equity levels are closer than their net worth counterparts.

-

For lower percentiles, home equity becomes substantial after age 40 and continues to grow until the early 60s.

-

For the median, home equity climbs earlier, starting in the early 30s and peaking in the late 60s.

-

The 75th percentile sees home equity rising in the late 20s, peaking in the 70s after a slight dip in the 50s and 60s. This dip might be attributed to factors like supporting children’s education.

-

For the 90th and 95th percentiles, home equity largely increases with age, while for the 99th percentile, it peaks in the late 60s before a substantial decline, possibly due to downsizing in later years.

Home Equity as a Percentage of Net Worth

Analyzing home equity as a fraction of net worth reveals further insights. For the 25th percentile, home equity constitutes over half of net worth, reaching as high as 86% for the late 70s age group. This proportion gradually decreases as we move up the percentile ladder, with home equity representing a much smaller fraction of net worth for the wealthiest individuals. This trend is visually depicted in the following graphs.

Conclusion: Interpreting Your Wealth Comparison

This data provides a benchmark to see where you stand in the wealth distribution. However, it’s crucial to remember that comparing yourself to others can be both motivating and discouraging. Financial advisors emphasize the importance of focusing on personal financial goals and developing healthy financial habits rather than solely relying on comparisons. While understanding your relative wealth position can be informative, true financial well-being comes from aligning your finances with your individual circumstances and aspirations.