How Do I Compare To My Peers financially? Comparing your net worth to your age group and social circle is a natural human tendency, but it’s crucial to understand where you stand. COMPARE.EDU.VN offers insightful analyses and data to help you assess your financial position, covering financial well-being, asset allocation, and investment strategies. Let us explore how you measure up and find a roadmap to financial success using personal finance benchmarks.

1. Understanding the Drive to Compare

The human desire to compare ourselves to others is deeply ingrained. It’s a natural instinct that can stem from various sources, including:

- Social Comparison Theory: Developed by Leon Festinger, this theory suggests that individuals have an innate drive to evaluate themselves by comparing themselves to others. This comparison can be upward (comparing to those perceived as better off) or downward (comparing to those perceived as worse off).

- Evolutionary Perspective: From an evolutionary standpoint, comparing ourselves to others may have served as a survival mechanism. Assessing our status relative to our peers could have helped us secure resources, attract mates, and improve our overall chances of survival.

- Societal Influences: Modern society often reinforces the tendency to compare ourselves to others. Media portrayals of success, social media updates showcasing idealized lifestyles, and even casual conversations about careers and finances can all contribute to this phenomenon.

1.1 The Psychological Impact of Financial Comparisons

While comparing ourselves to our peers can be a source of motivation, it can also have negative psychological consequences if not approached with caution:

- Increased Stress and Anxiety: Constantly comparing your financial situation to that of others can lead to feelings of stress and anxiety, particularly if you perceive yourself as falling behind.

- Reduced Self-Esteem: Upward social comparison, where you compare yourself to those who appear more successful, can lower your self-esteem and make you feel inadequate.

- Financial Dissatisfaction: Even if you are in a comfortable financial position, comparing yourself to wealthier individuals can lead to dissatisfaction and a sense of always wanting more.

- Risky Financial Behavior: The desire to “keep up with the Joneses” can drive individuals to engage in risky financial behaviors, such as taking on excessive debt or investing in speculative assets, in an attempt to quickly improve their financial standing.

1.2 The Importance of Context in Financial Comparisons

It’s crucial to remember that financial comparisons are only meaningful when viewed within the proper context. Factors such as age, career path, family situation, geographic location, and personal values can all significantly impact an individual’s financial standing. A 25-year-old just starting their career will naturally have a different financial profile than a 50-year-old executive with decades of experience.

Comparing yourself to someone in a high-paying but stressful job might be misleading if you prioritize work-life balance and job satisfaction over maximizing income. Similarly, comparing yourself to someone living in a low-cost-of-living area can be misleading if you live in an expensive city with higher housing costs and taxes.

2. Net Worth Percentiles by Age: A Comprehensive Analysis

Understanding how your net worth compares to others in your age group can provide valuable insights into your financial progress. Data from sources like the Federal Reserve and DQYDJ.com offer a comprehensive look at net worth percentiles by age.

Net worth is defined as the total value of your assets minus your liabilities. Assets include everything you own that has monetary value, such as cash, investments, real estate, and personal property. Liabilities include everything you owe, such as mortgages, loans, and credit card debt.

2.1 Interpreting Net Worth Percentiles

Net worth percentiles divide the population into 100 groups, each representing 1% of the population. For example, if your net worth falls into the 75th percentile for your age group, it means you have a higher net worth than 75% of people in that age group.

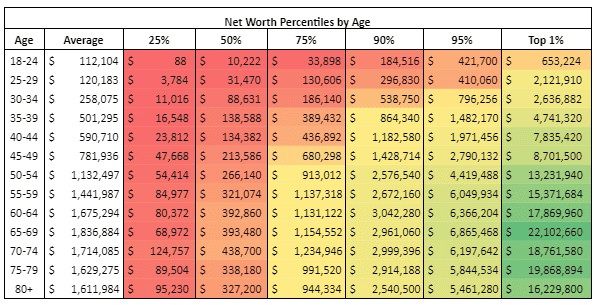

The following table presents net worth percentiles and averages by age group:

| Age Group | Average Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $83,900 | $7,200 | $24,400 | $73,800 | $220,000 | $444,000 | $1,620,000 |

| 25-34 | $229,700 | $28,300 | $98,400 | $323,700 | $774,700 | $1,400,000 | $4,350,000 |

| 35-44 | $524,900 | $72,200 | $206,200 | $636,400 | $1,500,000 | $2,610,000 | $7,510,000 |

| 45-54 | $828,900 | $123,100 | $315,800 | $963,000 | $2,250,000 | $4,100,000 | $11,900,000 |

| 55-64 | $1,179,400 | $175,300 | $439,400 | $1,390,000 | $2,780,000 | $5,180,000 | $14,700,000 |

| 65-74 | $1,267,500 | $195,400 | $454,700 | $1,580,000 | $3,100,000 | $5,700,000 | $16,300,000 |

| 75+ | $1,119,700 | $172,700 | $404,300 | $1,460,000 | $2,780,000 | $5,100,000 | $14,700,000 |

Note: These figures are based on data from the Federal Reserve and DQYDJ.com and may vary depending on the source and methodology used.

2.2 Key Observations from the Data

- The Average vs. the Median: Notice that the average net worth is consistently higher than the median net worth for each age group. This is because the average is skewed by the wealth of the top few percentiles, while the median represents the midpoint of the distribution.

- Wealth Accumulation Over Time: Net worth generally increases with age, reflecting the accumulation of assets and the repayment of debts over time. However, growth tends to slow down in later years as individuals enter retirement and begin drawing on their savings.

- Wide Disparities in Wealth: There are significant disparities in net worth within each age group, as evidenced by the wide range between the 25th and 99th percentiles. This highlights the impact of factors such as income, savings habits, investment decisions, and inheritance on wealth accumulation.

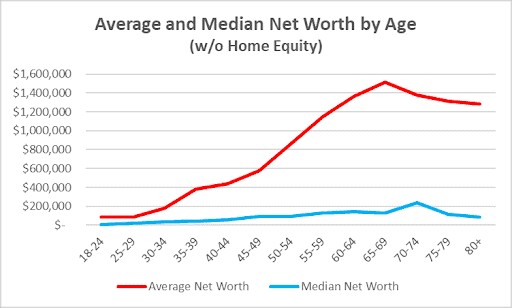

2.3 Excluding Home Equity: A Closer Look at Investable Assets

While total net worth provides a comprehensive picture of your financial standing, it’s also helpful to consider investable net worth, which excludes home equity. This metric can give you a better sense of the investment returns you might expect from your portfolio, as home equity doesn’t typically generate cash flow.

The following table presents investable net worth percentiles and averages by age group:

| Age Group | Average Investable Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $30,300 | $1,700 | $6,800 | $20,400 | $61,100 | $126,000 | $457,000 |

| 25-34 | $105,000 | $7,900 | $33,600 | $110,000 | $270,000 | $483,000 | $1,490,000 |

| 35-44 | $261,000 | $20,000 | $71,600 | $251,000 | $600,000 | $1,060,000 | $3,020,000 |

| 45-54 | $453,000 | $35,600 | $121,000 | $432,000 | $1,010,000 | $1,850,000 | $5,350,000 |

| 55-64 | $633,000 | $51,400 | $176,000 | $625,000 | $1,360,000 | $2,530,000 | $7,210,000 |

| 65-74 | $683,000 | $55,000 | $181,000 | $662,000 | $1,460,000 | $2,720,000 | $7,830,000 |

| 75+ | $599,000 | $48,000 | $158,000 | $593,000 | $1,280,000 | $2,350,000 | $6,740,000 |

Note: These figures are based on data from the Federal Reserve and DQYDJ.com and may vary depending on the source and methodology used.

2.4 Comparing Total Net Worth and Investable Net Worth

- Lower Investable Net Worth: Investable net worth is generally lower than total net worth, particularly for younger age groups. This is because home equity typically represents a larger portion of their wealth.

- Similar Patterns at Higher Percentiles: As you move up to the 75th percentile and higher, the difference between total net worth and investable net worth becomes less significant. This is because home equity plays a smaller role in wealth at these levels.

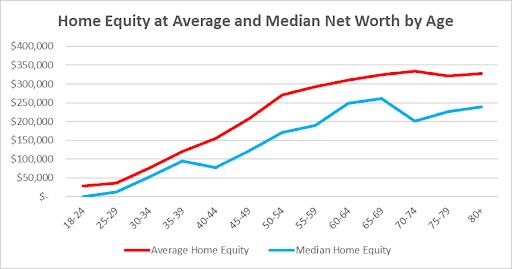

2.5 The Role of Home Equity

Home equity is the difference between the current market value of your home and the outstanding balance of your mortgage. It represents the portion of your home that you own outright.

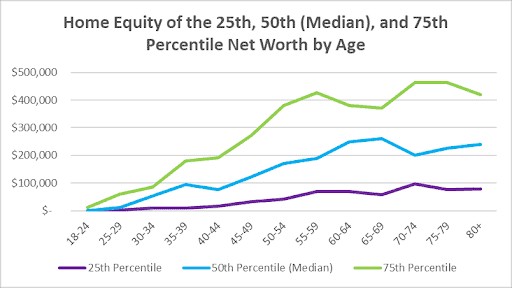

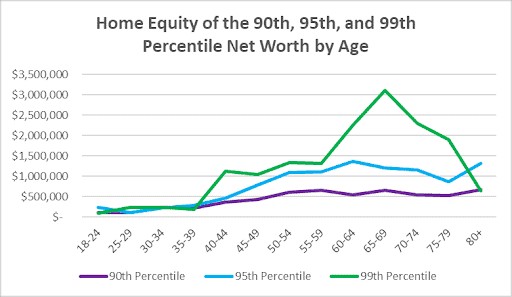

The following table shows the average home equity held by different net worth percentiles by age group:

| Age Group | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|

| 18-24 | $5,500 | $17,600 | $53,400 | $159,000 | $318,000 | $1,163,000 |

| 25-34 | $20,400 | $64,800 | $214,000 | $505,000 | $917,000 | $2,860,000 |

| 35-44 | $52,200 | $135,000 | $385,000 | $900,000 | $1,550,000 | $4,490,000 |

| 45-54 | $87,500 | $195,000 | $531,000 | $1,240,000 | $2,250,000 | $6,550,000 |

| 55-64 | $124,000 | $263,000 | $765,000 | $1,420,000 | $2,650,000 | $7,490,000 |

| 65-74 | $140,000 | $274,000 | $918,000 | $1,640,000 | $2,980,000 | $8,470,000 |

| 75+ | $125,000 | $246,000 | $867,000 | $1,500,000 | $2,750,000 | $7,960,000 |

Note: These figures are based on data from the Federal Reserve and DQYDJ.com and may vary depending on the source and methodology used.

2.6 Patterns in Home Equity Ownership

- Home Equity Growth with Age: Home equity generally increases with age, as individuals pay down their mortgages and home values appreciate.

- Home Equity and Net Worth Percentiles: Home equity levels tend to be higher for those in higher net worth percentiles, reflecting their ability to afford more expensive homes and pay down their mortgages more quickly.

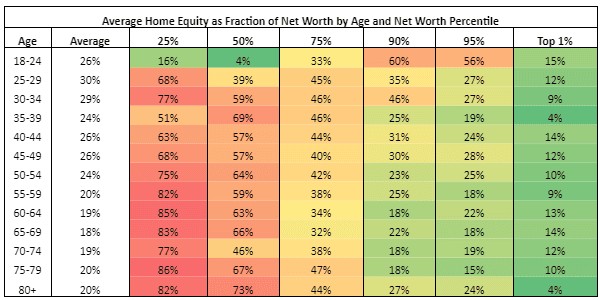

- Home Equity as a Fraction of Net Worth: Home equity represents a significant portion of net worth, especially for those in the lower net worth percentiles. As net worth increases, home equity tends to become a smaller fraction of overall wealth.

3. Factors Influencing Your Financial Standing

Several factors can influence where you stand financially compared to your peers. Understanding these factors can help you make informed decisions and set realistic financial goals.

3.1 Income

Income is a primary driver of wealth accumulation. Higher incomes allow individuals to save and invest more, accelerating their progress toward financial goals.

- Education and Skills: Higher levels of education and specialized skills often translate into higher earning potential.

- Career Choices: Some industries and professions offer significantly higher salaries than others.

- Negotiation and Advancement: The ability to negotiate salaries and advance within your career can have a substantial impact on your income over time.

3.2 Savings Habits

Saving a significant portion of your income is crucial for building wealth. The more you save, the more you can invest and the faster your wealth will grow.

- Setting Financial Goals: Having clear financial goals, such as saving for retirement or a down payment on a home, can motivate you to save more consistently.

- Budgeting and Tracking Expenses: Creating a budget and tracking your expenses can help you identify areas where you can cut back and save more.

- Automating Savings: Automating your savings by setting up regular transfers from your checking account to your savings or investment accounts can make it easier to save consistently.

3.3 Investment Strategies

Smart investment decisions can significantly boost your wealth over time. Investing allows your money to grow through compounding and can help you achieve your financial goals faster.

- Asset Allocation: Diversifying your investments across different asset classes, such as stocks, bonds, and real estate, can help you reduce risk and improve returns.

- Risk Tolerance: Understanding your risk tolerance is essential for choosing investments that align with your comfort level and financial goals.

- Long-Term Perspective: Investing is a long-term game. Avoid making impulsive decisions based on short-term market fluctuations.

3.4 Debt Management

Managing debt effectively is crucial for maintaining a healthy financial standing. High levels of debt can hinder your ability to save and invest, slowing down your progress toward financial goals.

- Avoiding High-Interest Debt: Minimize your use of high-interest debt, such as credit cards and payday loans.

- Paying Down Debt Strategically: Develop a plan for paying down your debt, focusing on the highest-interest debts first.

- Debt Consolidation: Consider debt consolidation options, such as balance transfers or personal loans, to lower your interest rates and simplify your payments.

3.5 Lifestyle Choices

Your lifestyle choices can have a significant impact on your financial standing. Overspending on non-essential items can derail your savings goals and prevent you from building wealth.

- Mindful Spending: Be mindful of your spending habits and avoid impulse purchases.

- Living Below Your Means: Spend less than you earn to create a surplus that you can save and invest.

- Prioritizing Experiences Over Possessions: Focus on experiences and relationships rather than material possessions.

3.6 Unexpected Events

Unexpected events, such as job loss, illness, or natural disasters, can have a significant impact on your financial standing. Having an emergency fund and adequate insurance coverage can help you weather these storms.

- Emergency Fund: Aim to save at least 3-6 months’ worth of living expenses in an emergency fund.

- Health Insurance: Ensure you have adequate health insurance coverage to protect yourself from unexpected medical bills.

- Disability Insurance: Consider disability insurance to replace your income if you become unable to work due to illness or injury.

4. How to Use Comparison Data Effectively

While it’s tempting to focus solely on comparing your net worth to others, it’s important to use comparison data as a tool for self-assessment and motivation, not as a source of stress or competition.

4.1 Focus on Personal Financial Goals

The most important thing is to focus on your personal financial goals, rather than getting caught up in comparisons. What do you want to achieve financially? Do you want to retire early, buy a home, start a business, or travel the world? Set clear financial goals and create a plan to achieve them.

4.2 Identify Areas for Improvement

Use comparison data to identify areas where you can improve your financial standing. Are you saving enough? Are you investing wisely? Are you managing your debt effectively? Once you’ve identified areas for improvement, develop a plan to address them.

4.3 Celebrate Your Progress

Acknowledge and celebrate your progress along the way. Building wealth is a marathon, not a sprint. It’s important to recognize and appreciate the milestones you achieve, no matter how small they may seem.

4.4 Seek Professional Advice

Consider seeking professional advice from a financial advisor. A financial advisor can help you assess your financial situation, set realistic goals, and develop a personalized plan to achieve them.

5. Mindset Matters: Cultivating a Healthy Financial Perspective

Your mindset plays a crucial role in your financial success and well-being. Cultivating a healthy financial perspective can help you make informed decisions, manage stress, and enjoy the journey toward financial security.

5.1 Gratitude

Practice gratitude for what you have, rather than focusing on what you lack. Appreciating your current financial situation can help you feel more content and less stressed.

5.2 Financial Education

Continuously educate yourself about personal finance. The more you know about saving, investing, and debt management, the better equipped you’ll be to make informed decisions.

5.3 Patience

Be patient and persistent. Building wealth takes time and effort. Don’t get discouraged by short-term setbacks. Stay focused on your long-term goals and keep making progress.

5.4 Self-Compassion

Be kind to yourself. Everyone makes financial mistakes from time to time. Don’t beat yourself up over them. Learn from your mistakes and move on.

5.5 Focus on What You Can Control

Focus on what you can control, such as your savings habits, investment decisions, and spending choices. Don’t worry about things you can’t control, such as market fluctuations or economic conditions.

5.6 Define Success on Your Own Terms

Define success on your own terms, rather than letting society dictate what it means to be financially successful. What’s important to you? What do you want to achieve with your money? Focus on living a life that aligns with your values and priorities.

6. Resources for Financial Comparison and Planning

COMPARE.EDU.VN is a valuable resource for comparing various financial products and services, as well as accessing educational content and tools to help you make informed decisions.

6.1 Wealthtender’s Advisor Directory

Wealthtender’s advisor directory offers a platform to connect with qualified financial advisors who can provide personalized guidance and support.

6.2 Government Resources

Government websites, such as the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA), offer valuable information and resources on investing and financial planning.

6.3 Non-Profit Organizations

Non-profit organizations, such as the National Foundation for Credit Counseling (NFCC) and the Association for Financial Counseling & Planning Education (AFCPE), provide financial education and counseling services.

7. Call to Action: Take Control of Your Financial Future

Ready to gain clarity on your financial standing and take control of your future? Visit COMPARE.EDU.VN today for comprehensive comparisons, expert insights, and personalized tools to help you make informed decisions. Whether you’re comparing investment options, exploring debt management strategies, or seeking guidance on retirement planning, COMPARE.EDU.VN is your trusted partner on the path to financial success. Don’t wait, empower yourself with knowledge and start building the future you deserve!

Remember, financial success is a journey, not a destination. By focusing on your personal goals, making informed decisions, and cultivating a healthy financial perspective, you can achieve financial security and live a fulfilling life.

Address: 333 Comparison Plaza, Choice City, CA 90210, United States

Whatsapp: +1 (626) 555-9090

Website: COMPARE.EDU.VN

8. Frequently Asked Questions (FAQ)

8.1 What is net worth?

Net worth is the total value of your assets minus your liabilities. Assets include everything you own that has monetary value, such as cash, investments, real estate, and personal property. Liabilities include everything you owe, such as mortgages, loans, and credit card debt.

8.2 How is net worth calculated?

To calculate your net worth, add up the value of all your assets and then subtract the total amount of your liabilities.

8.3 What is a good net worth for my age?

A “good” net worth depends on various factors, including your income, savings habits, investment decisions, lifestyle choices, and financial goals. Use the net worth percentiles by age data provided in this article as a benchmark, but remember to focus on your personal goals rather than getting caught up in comparisons.

8.4 What is investable net worth?

Investable net worth excludes home equity from your total net worth. This metric can give you a better sense of the investment returns you might expect from your portfolio, as home equity doesn’t typically generate cash flow.

8.5 Why is the average net worth higher than the median net worth?

The average net worth is skewed by the wealth of the top few percentiles, while the median represents the midpoint of the distribution.

8.6 How can I improve my net worth?

You can improve your net worth by increasing your income, saving more, investing wisely, managing your debt effectively, and making conscious lifestyle choices.

8.7 What is the role of home equity in net worth?

Home equity represents a significant portion of net worth, especially for those in the lower net worth percentiles. As net worth increases, home equity tends to become a smaller fraction of overall wealth.

8.8 Should I compare my net worth to others?

Comparing your net worth to others can be a useful tool for self-assessment and motivation, but it’s important to use comparison data with caution and focus on your personal financial goals.

8.9 What resources are available to help me with financial planning?

COMPARE.EDU.VN, Wealthtender’s advisor directory, government websites, and non-profit organizations offer valuable information and resources on investing and financial planning.

8.10 When should I seek professional financial advice?

Consider seeking professional advice from a financial advisor if you’re unsure how to assess your financial situation, set realistic goals, or develop a personalized plan to achieve them.

compare.edu.vn is dedicated to providing unbiased and comprehensive comparisons to empower you in making informed decisions. Our commitment lies in offering clarity and insights, guiding you towards choices that align with your unique needs and aspirations. Start exploring today and experience the confidence that comes with well-informed decisions.