Cigna and Blue Cross Blue Shield (BCBS) are leading health insurance providers, but determining which is better depends on individual needs and preferences, COMPARE.EDU.VN provides a detailed comparison to help you decide. This article will explore plan options, availability, provider networks, costs, and customer satisfaction to give you a complete overview. Discover the ideal health coverage by understanding key differences, financial security, and healthcare access, all critical aspects when choosing a health plan.

1. What Are The Key Differences Between Cigna and Blue Cross Blue Shield?

The primary differences between Cigna and Blue Cross Blue Shield (BCBS) lie in their availability, network size, and customer satisfaction ratings. BCBS offers individual and family plans in all 50 states, while Cigna’s individual and family plans are available in only 14 states. BCBS also boasts a larger in-network provider base, with 1.7 million providers compared to Cigna’s 1.5 million. In terms of customer satisfaction, BCBS generally receives higher ratings for its commercial health plans. This comparison, offered by COMPARE.EDU.VN, will help you in making an informed decision on healthcare coverage options, ensuring you find the best fit for your personal healthcare needs, budget considerations, and overall health benefits.

1.1 History and Background

- Blue Cross Blue Shield (BCBS): Originating in 1929, Blue Cross began as a partnership between Baylor University Hospital and its patients to make healthcare more affordable. The initial plan allowed patients to prepay 50 cents each month for up to 21 days of hospitalization per year. This innovative approach quickly gained popularity and expanded to include employees in other professions across Dallas. Over time, Blue Cross evolved into a nationwide network of independent companies, each providing health insurance plans tailored to their respective regions.

- Cigna: Cigna’s history dates back to 1792 with the founding of the Insurance Company of North America (INA). In 1982, INA merged with Connecticut General Life Insurance Company to create Cigna as it is known today. Cigna has grown into a global health service company offering a wide range of insurance and healthcare-related products and services.

1.2 Availability and Coverage Area

- BCBS: Offers individual and family plans in all 50 states, making it accessible to a broader range of customers across the United States. This extensive availability ensures that individuals and families, regardless of their location, can access BCBS plans and benefits.

- Cigna: Provides individual and family plans in only 14 states: Arizona, Colorado, Florida, Georgia, Illinois, Indiana, Mississippi, North Carolina, Pennsylvania, South Carolina, Tennessee, Texas, Utah, and Virginia. However, Cigna dental plans are available in all 50 states plus Washington, D.C., offering comprehensive dental coverage nationwide.

1.3 Provider Networks

- BCBS: Features a larger in-network provider base, with approximately 1.7 million healthcare providers. This extensive network ensures that policyholders have access to a wide range of doctors, specialists, and hospitals, facilitating convenient and comprehensive healthcare services.

- Cigna: Maintains a substantial provider network of 1.5 million providers globally. While slightly smaller than BCBS, Cigna’s network still offers a broad selection of healthcare professionals and facilities, ensuring policyholders can find suitable care options.

1.4 Customer Satisfaction

- BCBS: Generally receives higher customer satisfaction ratings for commercial health plans. Studies, such as those conducted by J.D. Power, often rank BCBS companies higher than Cigna in several regions. This indicates that BCBS policyholders are often more satisfied with their overall experience, including customer service, claims processing, and plan benefits.

- Cigna: In J.D. Power studies, Cigna ranked lower overall compared to BCBS companies but did rank higher in select regions. Customer satisfaction can vary based on specific plans, locations, and individual experiences.

1.5 Plan Structures and Offerings

Both Cigna and Blue Cross Blue Shield offer a variety of health insurance plans to meet different needs and preferences. Here’s a detailed comparison of the plan structures and offerings:

| Plan Type | Blue Cross Blue Shield | Cigna | Description |

|---|---|---|---|

| Individual & Family | ✓ | ✓ | Health insurance plans for individuals and families who do not receive coverage through an employer. |

| Medicare | ✓ | ✓ | Health insurance plans for individuals aged 65 and older, or those with certain disabilities, providing coverage for hospital stays, medical care, and prescription drugs. |

| Medicaid | ✓ | ✓ | Government-sponsored health insurance plans for low-income individuals and families, offering comprehensive medical benefits. |

| Dental | ✓ | ✓ | Insurance plans that cover dental care services such as routine check-ups, cleanings, fillings, and other dental procedures. |

| Vision | ✓ | ✓ | Insurance plans that cover eye exams, prescription glasses, and contact lenses. |

| Small Business | ✓ | ✓ | Health insurance plans designed for small businesses and their employees, offering a range of coverage options and benefits. |

| Self-Employed | ✓ | ✓ | Health insurance plans specifically designed for self-employed individuals, providing coverage similar to individual and family plans. |

| Short-Term | ✓ | ✓ | Temporary health insurance plans that offer coverage for a limited period, typically used to bridge gaps in coverage. |

| Student | ✓ | ✓ | Health insurance plans tailored for students, providing coverage for medical care and other health-related services while attending school. |

| Indemnity | ✓ | ✓ | Traditional health insurance plans that allow policyholders to seek medical care from any provider without needing referrals, but may require higher out-of-pocket costs. |

| CDHP (Consumer-Driven) | ✓ | ✓ | Health plans that combine a health savings account (HSA) or health reimbursement arrangement (HRA) with a high-deductible health plan, giving members more control over their healthcare spending. |

| EPO (Exclusive Provider Organization) | ✓ | ✓ | Health plans that require members to receive care from providers within the plan’s network, except in cases of emergency. |

| FSA (Flexible Spending Account) | ✓ | ✓ | Employer-sponsored accounts that allow employees to set aside pre-tax dollars for eligible healthcare expenses. |

| HDHP (High-Deductible Health Plan) | ✓ | ✓ | Health plans with higher deductibles and lower premiums, often paired with a health savings account (HSA). |

| HMO (Health Maintenance Organization) | ✓ | ✓ | Health plans that require members to choose a primary care physician (PCP) who coordinates their care and provides referrals to specialists within the plan’s network. |

| HMO-POS (HMO Point of Service) | ✓ | ✓ | A type of HMO plan that allows members to seek care from providers outside the plan’s network, but may require higher out-of-pocket costs and referrals. |

| HSA (Health Savings Account) | ✓ | ✓ | Tax-advantaged savings accounts that can be used to pay for qualified healthcare expenses, often paired with a high-deductible health plan (HDHP). |

| POS (Point of Service) | ✓ | ✓ | Health plans that allow members to choose between receiving care from in-network or out-of-network providers, with higher costs for out-of-network care. |

| PPO (Preferred Provider Organization) | ✓ | ✓ | Health plans that allow members to seek care from any provider without needing referrals, but offer lower costs for in-network care. |

2. Which Health Insurance Plan Offers Better Cost and Coverage?

Determining which health insurance plan offers better cost and coverage—Cigna or Blue Cross Blue Shield (BCBS)—depends on several factors, including plan type, location, and individual healthcare needs. Understanding these elements can help you make an informed decision. COMPARE.EDU.VN offers a comprehensive comparison, enabling you to weigh the costs and benefits of each option and find a plan that aligns with your specific requirements.

2.1 Cost Considerations

- Premiums: The monthly premium is the amount you pay each month to maintain your health insurance coverage. Premiums can vary significantly based on the plan type, coverage level, and your age and health status.

- Deductibles: The deductible is the amount you must pay out-of-pocket for healthcare services before your insurance begins to cover costs. Plans with lower premiums typically have higher deductibles, and vice versa.

- Copays: A copay is a fixed amount you pay for specific healthcare services, such as doctor’s visits or prescription drugs. Copays usually do not count toward your deductible.

- Coinsurance: Coinsurance is the percentage of healthcare costs you are responsible for after you meet your deductible. For example, if your coinsurance is 20%, you pay 20% of the costs, and your insurance covers the remaining 80%.

- Out-of-Pocket Maximum: The out-of-pocket maximum is the total amount you will pay for covered healthcare services in a plan year. Once you reach this limit, your insurance covers 100% of covered costs for the remainder of the year.

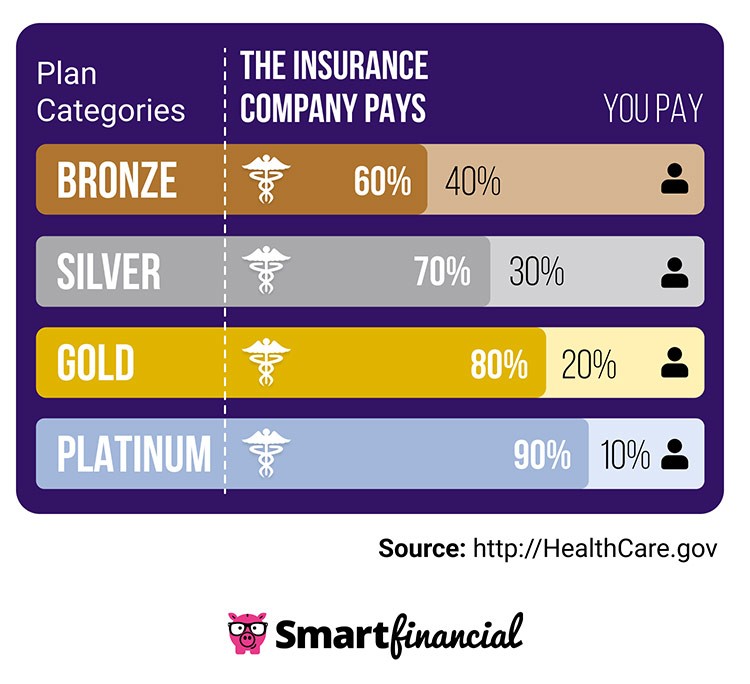

Health insurance rates are personalized and can vary significantly based on individual factors such as age, lifestyle, and the chosen plan. Both Cigna and BCBS use a tiered system, ranging from Bronze to Platinum, to determine costs. Bronze plans typically have the lowest premiums but the highest out-of-pocket costs, while Platinum plans have the highest premiums and the lowest out-of-pocket costs.

Health Insurance Tiers

Health Insurance Tiers

2.2 Coverage Limits and Essential Benefits

Both Cigna and BCBS are required to offer unlimited coverage for essential health benefits, as mandated by the Affordable Care Act (ACA). These essential benefits include:

- Outpatient and inpatient treatments

- Emergency care

- Laboratory work

- Mental health support

- Maternity and pediatric care

- Medication

- Chronic disease management

- Rehabilitation equipment

2.3 Plan Availability and Options

- Blue Cross Blue Shield: Offers a wide range of plans, including HMO, PPO, EPO, and POS options. They also provide specialized plans such as CDHP, FSA, HDHP, Indemnity, Medicaid, and Medicare. BCBS is available in all 50 states, providing more options for individuals and families across the country.

- Cigna: Offers similar plan types, including HMO, PPO, and EPO options. They also provide specialized plans such as CDHP, FSA, HDHP, Indemnity, Medicaid, and Medicare. However, Cigna’s individual and family plans are only available in 14 states.

2.4 Medical Loss Ratio (MLR)

The Medical Loss Ratio (MLR) indicates the percentage of premium income an insurance company spends on medical care and service quality improvement. Under the ACA, insurers must allocate at least 80% of individual plan premiums and 85% of group plan premiums to healthcare services. If they fall short, they are required to issue rebates to their policyholders.

- Blue Cross Blue Shield: MLR rebates can vary by state and year, as BCBS consists of independent regional entities. For example, BCBS of Montana did not issue rebates for the 2022 MLR reporting year, while BCBS of Massachusetts issued rebates to individuals and small group employers.

- Cigna: Cigna’s MLR ratio in 2023 was 81.3%, meaning no MLR rebates were issued for that year.

2.5 Example Scenario

Consider a scenario where a family of four resides in Texas. BCBS offers multiple plans with varying premiums, deductibles, and copays. A PPO plan might have a monthly premium of $1,200, a deductible of $5,000, and a copay of $30 for doctor’s visits. Cigna, also available in Texas, might offer a similar PPO plan with a monthly premium of $1,100, a deductible of $6,000, and a copay of $25 for doctor’s visits.

In this case, the Cigna plan has a lower monthly premium but a higher deductible. If the family anticipates needing frequent medical care, the BCBS plan might be more cost-effective due to the lower deductible. Conversely, if the family is generally healthy and does not anticipate needing frequent care, the Cigna plan might be a better option due to the lower monthly premium.

3. How Do the In-Network Providers of Cigna and Blue Cross Blue Shield Compare?

Comparing the in-network providers of Cigna and Blue Cross Blue Shield (BCBS) is essential for ensuring access to a wide range of healthcare professionals and facilities. BCBS boasts a slightly larger network, but both insurers offer substantial provider options. COMPARE.EDU.VN simplifies this comparison by providing comprehensive details on network size and accessibility, helping you choose a plan that aligns with your healthcare needs and preferences.

3.1 Network Size and Reach

- Blue Cross Blue Shield: Features an extensive network of approximately 1.7 million healthcare providers. This large network ensures that policyholders have access to a wide range of doctors, specialists, hospitals, and other healthcare facilities. The breadth of the BCBS network is particularly advantageous for those who require specialized care or live in areas with limited healthcare options.

- Cigna: Maintains a significant network of 1.5 million providers worldwide. While slightly smaller than BCBS, Cigna’s network still offers a substantial selection of healthcare professionals and facilities. Cigna’s global presence can be beneficial for individuals who travel frequently or require access to healthcare services in multiple locations.

3.2 Accessibility and Coverage

- BCBS: Accepted by 80% of doctors and 90% of hospitals in the U.S. This widespread acceptance ensures that policyholders can easily find in-network providers, reducing out-of-pocket costs and simplifying the process of receiving care. The extensive coverage makes BCBS a convenient choice for many individuals and families.

- Cigna: While Cigna’s network is smaller, it still provides broad access to healthcare services. The availability of in-network providers can vary by location, so it’s important to check whether your preferred doctors and hospitals are included in Cigna’s network before enrolling in a plan.

3.3 Impact on Costs

Choosing in-network providers is crucial for managing healthcare costs. Both Cigna and BCBS plans typically offer lower copays, coinsurance, and deductibles when you receive care from providers within their respective networks. Out-of-network care usually results in higher out-of-pocket expenses, making it important to select a plan with a network that aligns with your healthcare needs.

3.4 Provider Directories and Search Tools

Both Cigna and BCBS offer online provider directories and search tools to help policyholders find in-network doctors and facilities. These tools allow you to search by specialty, location, and other criteria, making it easier to identify providers who meet your specific needs. Regularly updating these directories ensures accurate information and simplifies the process of finding the right healthcare professionals.

3.5 Telehealth Services

Both Cigna and BCBS cover telehealth services, providing convenient access to healthcare from the comfort of your home. Telehealth can be a cost-effective and time-saving option for routine consultations, prescription refills, and other non-emergency medical needs. The availability and specific coverage details for telehealth services can vary by plan and location.

4. How Do Cigna and Blue Cross Blue Shield Handle Policy Management?

Policy management is a crucial aspect of health insurance, and both Cigna and Blue Cross Blue Shield (BCBS) offer digital platforms and mobile applications to help users manage their policies effectively. These tools provide convenient access to policy information, claims tracking, and healthcare provider searches. COMPARE.EDU.VN offers insights into the user experience of these platforms, aiding you in selecting an insurer that provides seamless and efficient policy management.

4.1 Digital Platforms and Mobile Applications

Both Cigna and BCBS provide digital platforms and mobile applications that allow users to:

- Manage their policies

- Search for healthcare providers

- Monitor claims

- Access policy documents

- Pay premiums

- Request ID cards

These digital tools aim to streamline policy management and provide users with easy access to essential information.

4.2 User Experience

The user experience for these apps can vary by location and platform. For example, Cigna has the same Apple App Store star rating as Blue Shield of California and Florida Blue, but its star rating is higher than BCBS of Illinois. Meanwhile, Cigna has a lower Google Play Store star rating than all three of the aforementioned BCBS companies.

| Company | Google Play Store | Apple App Store |

|---|---|---|

| Cigna | 2.5/5 stars | 4.8/5 stars |

| Blue Cross and Blue Shield of Illinois | 3.3/5 | 3.2/5 |

| Blue Shield of California | 4.0/5 | 4.8/5 |

| Florida Blue | 4.6/5 | 4.8/5 |

These ratings indicate that the user experience can differ significantly depending on the specific BCBS company and the mobile platform used.

4.3 Policy Management Features

Key policy management features offered by both Cigna and BCBS include:

- Claims Tracking: Real-time updates on the status of submitted claims, including details on processing and payment.

- Provider Search: Tools to locate in-network healthcare providers, including doctors, specialists, and hospitals.

- Policy Documents: Access to digital versions of policy documents, including coverage details, terms and conditions, and plan summaries.

- Premium Payments: Options to pay premiums online, set up automatic payments, and view payment history.

- ID Cards: Digital ID cards that can be accessed through the mobile app, eliminating the need to carry physical cards.

4.4 Customer Support

Both Cigna and BCBS offer customer support through various channels, including:

- Phone

- Online chat

- In-person assistance (depending on location)

The quality and responsiveness of customer support can significantly impact the overall policy management experience.

5. How Do Customer Reviews Compare for Cigna and Blue Cross Blue Shield?

Customer reviews provide valuable insights into the overall satisfaction and experience of policyholders with Cigna and Blue Cross Blue Shield (BCBS). Comparing these reviews across multiple sources can help you make an informed decision. COMPARE.EDU.VN presents a balanced overview of customer feedback, enabling you to assess the strengths and weaknesses of each insurer and choose a plan that aligns with your expectations.

5.1 Ratings from Various Sources

Customer reviews and ratings can vary depending on the source. Here’s a comparison of ratings from several reputable platforms:

| Company | Blue Cross Blue Shield Rating | Cigna |

|---|---|---|

| BestCompany | 3.0/5 stars | 1.9/5 stars |

| Affordable Health Insurance | 4.6/5 | 4.2/5 |

| BBB (Better Business Bureau) | 1.16/5 | 1.07/5 |

These ratings indicate that BCBS generally receives higher customer reviews compared to Cigna, particularly on BestCompany and Affordable Health Insurance.

5.2 J.D. Power Study

In a 2023 J.D. Power study that measured commercial health plan member satisfaction, BCBS outperformed Cigna in several regions. In 18 of the 20 regions where both BCBS and Cigna were among the top companies, a BCBS company ranked higher than Cigna. However, since BCBS is a collection of multiple companies, there were some cases in which Cigna ranked below one BCBS company but higher than another. Notably, Cigna was the top-ranked company in New Jersey.

5.3 Common Themes in Customer Reviews

- Blue Cross Blue Shield: Customers often praise BCBS for its extensive network, reliable coverage, and customer service. Positive reviews frequently mention the ease of finding in-network providers and the helpfulness of customer support representatives.

- Cigna: While some customers appreciate Cigna’s plan options and digital tools, others express concerns about claims processing, coverage denials, and customer service responsiveness.

5.4 Factors Influencing Customer Satisfaction

Several factors can influence customer satisfaction with health insurance providers, including:

- Claims Processing: The speed and accuracy of claims processing can significantly impact customer satisfaction. Delays or denials can lead to frustration and negative reviews.

- Customer Service: The quality of customer service, including the responsiveness and helpfulness of representatives, is a key factor in customer satisfaction.

- Network Coverage: The availability of in-network providers and the ease of accessing care can influence customer satisfaction.

- Plan Benefits: The comprehensiveness of plan benefits and the extent of coverage for medical services can affect customer satisfaction.

6. How Does the Enrollment Process Differ Between Cigna and Blue Cross Blue Shield?

Understanding the enrollment process for Cigna and Blue Cross Blue Shield (BCBS) is essential for securing timely health coverage. Both insurers offer enrollment during open enrollment periods, but also provide special enrollment periods for qualifying life events. COMPARE.EDU.VN offers a streamlined overview of these processes, empowering you to navigate enrollment smoothly and ensure continuous health coverage.

6.1 Open Enrollment Period

To purchase a BCBS or Cigna plan from your state’s health insurance marketplace, you will typically need to enroll during the open enrollment period in the fall or winter:

| Open Enrollment Period | Coverage Start Date |

|---|---|

| Nov. 1 to Dec. 15 | Jan. 1 |

| Dec. 16 to Jan. 15 | Feb. 1 |

During this period, anyone can enroll in a new health insurance plan or make changes to their existing coverage.

6.2 Special Enrollment Period

If you miss open enrollment, it’s still possible to purchase an ACA plan any time of the year if you experience a qualifying life event. Qualifying life events trigger what’s called a special enrollment period, and these events typically include:

- Changing jobs

- Moving to a new zip code

- Having a child

- Losing existing health coverage

- Getting married or divorced

The special enrollment period typically lasts 60 days from the date of the qualifying life event.

6.3 Medicare Enrollment Periods

For those looking to enroll in a Medicare Advantage plan, separate Medicare enrollment periods exist:

| Period | Action |

|---|---|

| 3 months before you turn 65 to 3 months after | Enroll in a Medicare Advantage plan (if you have both Medicare Part A and B) |

| October 15 to December 7 for coverage starting on January 1 | Switch from Original Medicare to a Medicare Advantage plan; switch from one Medicare Advantage plan to another Medicare Advantage plan |

| January 1 to March 31 for coverage starting on the 1st of the month after the company receives your request | Switch from one Medicare Advantage plan to another Medicare Advantage plan; drop your Medicare Advantage plan and return to Original Medicare |

These enrollment periods ensure that individuals have opportunities to enroll in or change their Medicare coverage.

6.4 Application Process

The application process for Cigna and BCBS plans typically involves:

- Visiting the Health Insurance Marketplace: Access the official website for your state’s health insurance marketplace (or the federal marketplace at HealthCare.gov if your state does not have its own).

- Creating an Account: Create an account and provide the necessary information, including your name, address, date of birth, and Social Security number.

- Completing the Application: Fill out the application form, providing details about your household income, family members, and any existing health coverage.

- Comparing Plans: Review the available plans from Cigna, BCBS, and other insurers, comparing premiums, deductibles, copays, and coverage benefits.

- Selecting a Plan: Choose the plan that best meets your needs and budget.

- Enrolling: Complete the enrollment process and submit your application.

- Paying Your Premium: Pay your first month’s premium to activate your coverage.

7. Filing Claims with Cigna and Blue Cross Blue Shield: What You Need to Know?

Knowing how to file claims with Cigna and Blue Cross Blue Shield (BCBS) is essential for receiving proper reimbursement for healthcare services. While in-network providers usually handle the claims process, understanding the steps for out-of-network services is crucial. COMPARE.EDU.VN offers a clear guide on how to navigate the claims process with both insurers, ensuring you can confidently manage your healthcare expenses.

7.1 In-Network vs. Out-of-Network Claims

- In-Network Claims: When you see an in-network healthcare provider, they typically manage the insurance claims process on your behalf. The provider submits the claim directly to the insurance company, and you are only responsible for paying your copay, coinsurance, or deductible.

- Out-of-Network Claims: If you use out-of-network services, you’ll need to file the insurance claim yourself. This involves gathering the necessary documentation and submitting it to the insurance company for reimbursement.

7.2 Steps for Filing an Out-of-Network Claim

- Obtain a Claim Form: Both Cigna and BCBS have designated forms for submitting out-of-network claims. You can typically download these forms from their websites or request them by contacting customer service.

- Gather Documentation: Collect all relevant documentation, including:

- The completed claim form

- An itemized bill from the healthcare provider

- Proof of payment (if you have already paid the bill)

- Any other supporting documents, such as referral forms or medical records

- Complete the Claim Form: Fill out the claim form accurately and completely, providing all required information.

- Submit the Claim: Mail the completed claim form and supporting documentation to the specified address for Cigna or BCBS.

- Track Your Claim: You can track the status of your claim through your insurer’s online portal or mobile app. This allows you to monitor the progress of your claim and receive updates on its processing.

7.3 Contact Information

For specific claim submission addresses and contact information, refer to the Cigna and BCBS websites or contact their customer service departments.

7.4 Tips for Successful Claims Filing

- Review Your Policy: Familiarize yourself with your policy’s coverage details, including deductibles, copays, coinsurance, and any limitations or exclusions.

- Keep Accurate Records: Maintain accurate records of all healthcare services received and payments made.

- Submit Claims Promptly: File your claims as soon as possible after receiving healthcare services to ensure timely processing.

- Follow Up: If you don’t receive a response within a reasonable timeframe, follow up with the insurance company to check on the status of your claim.

- Seek Assistance: If you have questions or need assistance with the claims process, contact Cigna or BCBS customer service for guidance.

7.5 Avoiding Common Pitfalls

- Incomplete Forms: Ensure that your claim form is complete and accurate, providing all required information.

- Missing Documentation: Include all necessary documentation, such as itemized bills and proof of payment.

- Untimely Filing: Submit your claims within the specified timeframe to avoid denial.

- Out-of-Network Restrictions: Be aware of any restrictions on out-of-network coverage and the potential for higher out-of-pocket costs.

By following these steps and tips, you can navigate the claims process with Cigna and BCBS more effectively, ensuring you receive the reimbursements you are entitled to.

8. Conclusion: Cigna vs. Blue Cross Blue Shield – Which Is Right for You?

Choosing between Cigna and Blue Cross Blue Shield (BCBS) requires careful consideration of your individual needs, preferences, and circumstances. Both insurers offer a range of plans and benefits, but key differences in availability, network size, customer satisfaction, and policy management can influence your decision.

- Availability: BCBS offers individual and family plans in all 50 states, making it a more accessible option for individuals and families across the country. Cigna’s individual and family plans are available in only 14 states.

- Network Size: BCBS boasts a larger in-network provider base, with 1.7 million providers compared to Cigna’s 1.5 million. This extensive network ensures broad access to healthcare professionals and facilities.

- Customer Satisfaction: BCBS generally receives higher customer satisfaction ratings, indicating a more positive overall experience for policyholders. However, customer satisfaction can vary based on specific plans, locations, and individual experiences.

- Policy Management: Both Cigna and BCBS offer digital platforms and mobile applications for policy management, but user experience can vary.

Ultimately, the best choice depends on your specific needs and priorities.

For those seeking comprehensive and objective comparisons, visit COMPARE.EDU.VN at 333 Comparison Plaza, Choice City, CA 90210, United States, or contact us via Whatsapp at +1 (626) 555-9090. We are dedicated to helping you make informed decisions.

9. FAQs About Cigna and Blue Cross Blue Shield

9.1 Is Cigna the same as UnitedHealthcare?

Cigna and UnitedHealthcare are two different health insurance companies, each with its own provider network and plan availability.

9.2 Is Cigna Healthcare any good?

Whether or not Cigna is good can be subjective. In a 2023 J.D. Power study, Cigna ranked lower overall in terms of customer reviews compared to BCBS companies but did rank higher in select regions.

9.3 Is Blue Shield different from Blue Cross Blue Shield?

Blue Shield is a part of the Blue Cross Blue Shield Association. There are 33 locally operated companies within the association, with BCBS trademarks and names in over 170 countries.

9.4 What are the key differences between HMO and PPO plans offered by Cigna and BCBS?

HMO plans typically require you to choose a primary care physician (PCP) who coordinates your care and provides referrals to specialists within the plan’s network. PPO plans offer more flexibility, allowing you to see specialists without referrals, but may have higher out-of-pocket costs.

9.5 How do I find a doctor in the Cigna or BCBS network?

Both Cigna and BCBS offer online provider directories and search tools to help you find in-network doctors and facilities. You can search by specialty, location, and other criteria.

9.6 What is a deductible, and how does it affect my health insurance costs?

A deductible is the amount you must pay out-of-pocket for healthcare services before your insurance begins to cover costs. Plans with lower premiums typically have higher deductibles, and vice versa.

9.7 What is coinsurance, and how does it work?

Coinsurance is the percentage of healthcare costs you are responsible for after you meet your deductible. For example, if your coinsurance is 20%, you pay 20% of the costs, and your insurance covers the remaining 80%.

9.8 What is an out-of-pocket maximum, and why is it important?

The out-of-pocket maximum is the total amount you will pay for covered healthcare services in a plan year. Once you reach this limit, your insurance covers 100% of covered costs for the remainder of the year, providing financial protection against high medical expenses.

9.9 Can I change my health insurance plan outside of the open enrollment period?

You can change your health insurance plan outside of the open enrollment period if you experience a qualifying life event, such as changing jobs, moving to a new zip code, or having a child. These events trigger a special enrollment period, allowing you to enroll in a new plan or make changes to your existing coverage.

9.10 How do I file a complaint with Cigna or BCBS if I am dissatisfied with their service?

Both Cigna and BCBS have procedures for filing complaints. You can typically file a complaint online, by phone, or in writing. Be sure to provide all relevant details and documentation to support your complaint.

Sources

- Insurance quotes /

- Health /

- Company Comparisons /

- Blue Cross Blue Shield vs. Cigna

[

Derek San Filippo

Health Insurance Expert ](/author/derek-san-filippo)

Derek has over 10 years of experience writing web content for a variety of online publications. His pieces range from finances and entertainment to religion and philosophy. For the past three years, Derek has focused on writing financial literacy articles for credit unions throughout the country. He prides himself on being able to take complex topics and make them accessible to the general public.

Ready to make an informed decision about your health insurance? Visit compare.edu.vn today for comprehensive comparisons and personalized recommendations. Our detailed analyses help you weigh the pros and cons of each option, ensuring you find the best plan for your unique needs and budget. Don’t navigate the complexities of health insurance alone—let us help you find the perfect fit.