Comparing your financial status to others your age can offer insights into your progress and identify areas for improvement, and COMPARE.EDU.VN provides the resources to do just that. This comparison helps you understand where you stand in terms of financial planning, net worth comparison, and retirement readiness, ultimately guiding you toward better financial decisions. Leverage insights on financial security and wealth accumulation.

1. Understanding Financial Benchmarking

Financial benchmarking involves comparing your financial metrics against a standard or a peer group to evaluate your performance. This process helps you identify strengths and weaknesses in your financial strategy, providing a clearer picture of where you stand financially. By understanding the concept of financial benchmarking, you can better assess your progress and make informed decisions to improve your overall financial health.

1.1. What is Financial Benchmarking?

Financial benchmarking is the process of comparing your financial performance and metrics to those of a peer group or an established standard. This comparison can reveal areas where you excel and areas needing improvement. Benchmarking isn’t about competition but about understanding where you stand and identifying opportunities for growth and optimization. Key metrics often include income, savings rate, debt levels, net worth, and investment returns.

1.2. Why is it Important to Compare Financially?

Comparing your financial standing to others can provide valuable insights. It helps you gauge whether you’re on track for your financial goals, identify potential gaps in your financial strategy, and motivate you to make necessary adjustments. For instance, if you find that your savings rate is significantly lower than your peer group, it might prompt you to re-evaluate your spending habits and increase your savings efforts. This comparative analysis fosters financial awareness and encourages proactive financial planning.

1.3. Benefits of Financial Comparison

Financial comparison offers numerous benefits, including:

- Goal Setting: Benchmarking helps you set realistic and achievable financial goals based on what others in similar situations have accomplished.

- Identifying Strengths and Weaknesses: By comparing your financial metrics, you can identify areas where you are performing well and areas that need improvement.

- Motivation: Seeing how others are progressing can motivate you to improve your financial habits and work towards your goals.

- Informed Decision-Making: Comparative data can inform your financial decisions, helping you make choices that align with your financial goals and improve your financial health.

- Financial Awareness: The process of comparing your finances increases your overall financial awareness, leading to better financial management.

2. Key Metrics for Financial Comparison

To effectively compare your financial standing, focusing on specific metrics is crucial. These metrics provide a comprehensive view of your financial health and enable meaningful comparisons.

2.1. Income

Income is a fundamental metric for financial comparison. It represents the total amount of money you earn over a specific period, typically a year. When comparing income, consider factors such as education, occupation, and location, as these can significantly impact earning potential.

2.1.1. Understanding Income Levels by Age Group

Income levels vary considerably across different age groups. Early in your career, income tends to be lower as you gain experience and skills. As you progress, your earning potential typically increases until you reach your peak earning years, usually between the ages of 45 and 55. After this, income may plateau or decrease as you approach retirement.

2.1.2. Average vs. Median Income

When analyzing income data, understanding the difference between average and median income is essential. The average income is the sum of all incomes divided by the number of individuals. In contrast, the median income is the middle value when all incomes are arranged in ascending order. The median is often a better representation of typical income because it is less affected by extreme values.

2.2. Savings Rate

The savings rate is the percentage of your income that you save. A higher savings rate is generally indicative of better financial health, as it demonstrates your ability to live below your means and prepare for future financial needs.

2.2.1. Calculating Your Savings Rate

To calculate your savings rate, divide your total savings by your gross income and multiply by 100. For example, if you save $10,000 annually and your gross income is $50,000, your savings rate is 20%.

2.2.2. Ideal Savings Rate by Age

The ideal savings rate varies by age. Younger individuals should aim to save at least 15% of their income to take advantage of compounding interest over time. As you get older, you may need to increase your savings rate to catch up on retirement savings, especially if you started saving later in life.

2.3. Debt Levels

Debt levels can significantly impact your financial health. High levels of debt can strain your budget, limit your ability to save and invest, and increase financial stress.

2.3.1. Types of Debt to Consider

When evaluating debt levels, consider all types of debt, including:

- Mortgage Debt: The amount owed on your home loan.

- Student Loan Debt: The amount owed on student loans.

- Credit Card Debt: The outstanding balance on your credit cards.

- Auto Loan Debt: The amount owed on your car loan.

- Personal Loan Debt: The amount owed on personal loans.

2.3.2. Healthy Debt-to-Income Ratio

The debt-to-income (DTI) ratio is a key indicator of your ability to manage debt. To calculate your DTI, divide your total monthly debt payments by your gross monthly income. A DTI of 36% or less is generally considered healthy, while a DTI above 43% may indicate financial stress.

2.4. Net Worth

Net worth is a comprehensive measure of your overall financial health. It represents the difference between your assets and liabilities. A positive net worth indicates that you own more than you owe, while a negative net worth means you owe more than you own.

2.4.1. Calculating Your Net Worth

To calculate your net worth, add up all your assets (e.g., cash, investments, real estate) and subtract all your liabilities (e.g., mortgage, loans, credit card debt).

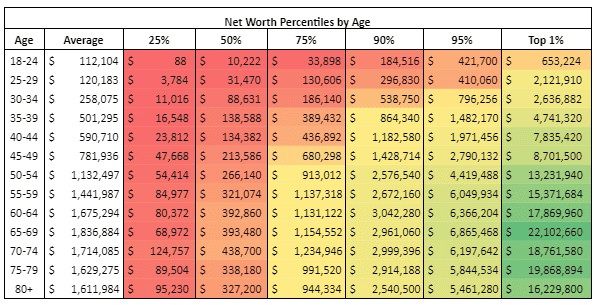

2.4.2. Average Net Worth by Age Group

Average net worth varies significantly by age group. Younger individuals typically have lower net worth due to less time to accumulate assets, while older individuals have had more time to build wealth. Understanding the average net worth for your age group can provide a benchmark for your own financial progress.

2.5. Investment Returns

Investment returns measure the profitability of your investments. Higher investment returns can accelerate wealth accumulation, helping you reach your financial goals faster.

2.5.1. Benchmarking Your Investment Performance

Benchmarking your investment performance involves comparing your returns to those of relevant market indices or peer groups. This comparison helps you assess whether your investment strategy is effective and identify areas for improvement.

2.5.2. Factors Influencing Investment Returns

Several factors can influence investment returns, including asset allocation, risk tolerance, and market conditions. Diversifying your portfolio and aligning your investments with your risk tolerance can help optimize your returns over the long term.

3. Understanding Net Worth Percentiles and Averages

Comparing your net worth to others involves understanding both percentiles and averages. These metrics provide different perspectives on wealth distribution and can help you gauge where you stand financially.

3.1. What are Net Worth Percentiles?

Net worth percentiles divide the population into 100 equal groups based on their net worth. For example, if your net worth is in the 75th percentile, it means you have a higher net worth than 75% of the population. Percentiles offer a more nuanced view of wealth distribution than averages, as they are less affected by extreme values.

3.2. What are Net Worth Averages?

Net worth averages represent the sum of all net worths divided by the number of individuals. While averages provide a general sense of wealth, they can be skewed by the very wealthy. Therefore, it’s essential to consider both averages and percentiles when comparing your net worth.

3.3. Comparing Average vs. Median Net Worth

The average net worth is often higher than the median net worth due to the influence of high-net-worth individuals. The median net worth provides a more accurate representation of the typical net worth for a given age group, as it is less affected by outliers.

3.4. Net Worth Percentiles by Age Group

Net worth percentiles vary by age group, reflecting the different stages of wealth accumulation. Younger individuals typically have lower net worth percentiles, while older individuals tend to have higher percentiles.

3.4.1. 25th Percentile

The 25th percentile represents the net worth of individuals who are in the bottom quartile of wealth distribution. This group often includes younger individuals just starting their careers and those with significant debt.

3.4.2. 50th Percentile (Median)

The 50th percentile, or median net worth, represents the middle value of net worth distribution. This metric provides a more accurate representation of typical net worth for a given age group.

3.4.3. 75th Percentile

The 75th percentile represents the net worth of individuals who are in the top quartile of wealth distribution. This group often includes individuals who have been saving and investing consistently over time.

3.4.4. 90th Percentile

The 90th percentile represents the net worth of individuals who are in the top 10% of wealth distribution. This group often includes high-income earners and those who have made strategic investment decisions.

3.4.5. 95th Percentile

The 95th percentile represents the net worth of individuals who are in the top 5% of wealth distribution. This group often includes affluent individuals with significant assets and investments.

3.4.6. 99th Percentile

The 99th percentile represents the net worth of individuals who are in the top 1% of wealth distribution. This group often includes the wealthiest individuals in society, with substantial assets and investments.

4. The Impact of Home Equity on Net Worth

Home equity, the difference between the current market value of your home and the outstanding balance on your mortgage, plays a significant role in net worth. Understanding how home equity affects your financial standing is crucial for accurate comparison.

4.1. What is Home Equity?

Home equity represents the portion of your home that you own outright. As you pay down your mortgage and your home’s value increases, your home equity grows.

4.2. How Home Equity Affects Net Worth

Home equity is considered an asset and is included in your net worth calculation. A higher home equity can significantly boost your net worth, providing a sense of financial security and potential for future borrowing.

4.3. Excluding Home Equity for Investment Comparisons

When comparing investment returns and financial performance, excluding home equity can provide a clearer picture of your investment portfolio’s effectiveness. This is because home equity doesn’t typically generate cash flow like other investments.

4.4. Home Equity Trends by Age and Net Worth Percentile

Home equity trends vary by age and net worth percentile. Younger individuals often have lower home equity due to recent home purchases, while older individuals tend to have higher equity due to mortgage paydown and home appreciation.

4.4.1. Lower Net Worth Percentiles

For individuals in lower net worth percentiles, home equity often makes up a significant portion of their net worth. This is because they may have fewer other assets and rely heavily on their home as a primary source of wealth.

4.4.2. Higher Net Worth Percentiles

For individuals in higher net worth percentiles, home equity typically represents a smaller portion of their overall net worth. These individuals often have more diversified assets, including investments, stocks, and bonds, reducing the relative importance of home equity.

4.5. Home Equity as a Fraction of Net Worth

The fraction of net worth represented by home equity varies by age and net worth percentile. In lower net worth percentiles, home equity can account for more than half of net worth, while in higher percentiles, it may account for only a small fraction.

5. Factors Influencing Financial Standing

Several factors can influence your financial standing, including education, career choices, lifestyle, and financial habits. Understanding these factors can help you make informed decisions to improve your financial health.

5.1. Education

Education plays a significant role in earning potential and financial success. Higher levels of education often lead to higher-paying jobs and greater opportunities for career advancement.

5.1.1. Impact of Education on Income

Individuals with higher levels of education tend to earn more over their lifetimes than those with less education. This is because education equips individuals with the skills and knowledge needed to succeed in higher-paying professions.

5.1.2. Managing Student Loan Debt

Student loan debt can impact your financial health, especially in the early stages of your career. Managing student loan debt effectively through strategies such as refinancing and income-driven repayment plans can help you free up cash flow for savings and investments.

5.2. Career Choices

Your career choices significantly influence your income and financial prospects. Choosing a career that aligns with your skills, interests, and market demand can lead to greater job satisfaction and financial success.

5.2.1. High-Earning Professions

Certain professions, such as medicine, law, engineering, and finance, tend to offer higher earning potential. Pursuing a career in one of these fields can significantly boost your income and accelerate wealth accumulation.

5.2.2. Career Advancement Strategies

Career advancement strategies, such as pursuing advanced degrees, obtaining certifications, and developing in-demand skills, can help you increase your earning potential over time.

5.3. Lifestyle

Your lifestyle choices can significantly impact your financial health. Living below your means and making conscious spending decisions can help you save more and achieve your financial goals faster.

5.3.1. Living Below Your Means

Living below your means involves spending less than you earn and saving the difference. This approach allows you to build wealth over time and prepare for future financial needs.

5.3.2. Conscious Spending Habits

Conscious spending habits involve making deliberate choices about where your money goes and aligning your spending with your values and priorities. This approach can help you avoid impulse purchases and make more informed financial decisions.

5.4. Financial Habits

Your financial habits, such as budgeting, saving, and investing, play a crucial role in your financial success. Developing good financial habits early in life can set you on the path to financial security.

5.4.1. Budgeting and Financial Planning

Budgeting and financial planning involve creating a roadmap for your finances, outlining your income, expenses, savings goals, and investment strategies. This approach can help you stay on track and achieve your financial objectives.

5.4.2. Saving and Investing Early

Saving and investing early allows you to take advantage of compounding interest, which can significantly boost your wealth over time. Even small amounts saved regularly can grow into substantial sums with the power of compounding.

6. Strategies for Improving Your Financial Standing

If you find that you are not where you want to be financially, several strategies can help you improve your standing. These strategies involve making informed financial decisions and developing good financial habits.

6.1. Creating a Budget

Creating a budget is the first step towards taking control of your finances. A budget helps you track your income and expenses, identify areas where you can cut back, and allocate your money towards your financial goals.

6.1.1. Tracking Income and Expenses

Tracking your income and expenses is essential for creating an effective budget. You can use budgeting apps, spreadsheets, or traditional pen and paper to monitor your cash flow and identify spending patterns.

6.1.2. Setting Financial Goals

Setting financial goals, such as saving for a down payment, paying off debt, or investing for retirement, provides a clear direction for your budget. Make sure your goals are specific, measurable, achievable, relevant, and time-bound (SMART).

6.2. Increasing Your Income

Increasing your income can significantly improve your financial standing by providing more resources for saving, investing, and debt repayment.

6.2.1. Pursuing Higher Education or Training

Pursuing higher education or vocational training can enhance your skills and knowledge, leading to higher-paying job opportunities.

6.2.2. Seeking Promotions or New Job Opportunities

Seeking promotions or new job opportunities within your field can help you increase your income and advance your career.

6.2.3. Starting a Side Hustle

Starting a side hustle, such as freelancing, consulting, or selling products online, can provide an additional income stream to supplement your primary earnings.

6.3. Reducing Debt

Reducing debt can free up cash flow, lower your financial stress, and improve your overall financial health.

6.3.1. Prioritizing High-Interest Debt

Prioritize paying off high-interest debt, such as credit card debt, to minimize interest charges and accelerate debt repayment.

6.3.2. Debt Consolidation Strategies

Debt consolidation strategies, such as balance transfers and personal loans, can help you combine multiple debts into a single loan with a lower interest rate, making it easier to manage and repay your debt.

6.4. Saving More

Saving more money allows you to build wealth, prepare for emergencies, and achieve your financial goals faster.

6.4.1. Automating Savings

Automating your savings by setting up automatic transfers from your checking account to your savings or investment accounts can help you save consistently without having to think about it.

6.4.2. Cutting Unnecessary Expenses

Cutting unnecessary expenses, such as dining out, entertainment, and subscription services, can free up more money for savings and investments.

6.5. Investing Wisely

Investing wisely can help you grow your wealth over time and achieve your long-term financial goals.

6.5.1. Diversifying Your Investments

Diversifying your investments across different asset classes, such as stocks, bonds, and real estate, can help reduce risk and optimize returns.

6.5.2. Seeking Professional Financial Advice

Seeking professional financial advice from a qualified financial advisor can help you develop a personalized investment strategy that aligns with your financial goals, risk tolerance, and time horizon.

7. Resources for Financial Comparison

Several resources are available to help you compare your financial standing to others your age. These resources provide valuable data and insights that can inform your financial decisions.

7.1. Online Calculators and Tools

Online calculators and tools can help you assess your financial health, calculate your net worth, and compare your financial metrics to those of your peer group.

7.2. Government and Industry Reports

Government and industry reports, such as those published by the Federal Reserve and financial institutions, provide valuable data on income, savings, debt, and net worth trends.

7.3. Financial Planning Websites

Financial planning websites offer articles, guides, and resources on various financial topics, including benchmarking and financial comparison.

7.4. Financial Advisors

Financial advisors can provide personalized advice and guidance on how to improve your financial standing and achieve your financial goals.

8. The Role of COMPARE.EDU.VN in Financial Comparison

COMPARE.EDU.VN offers a comprehensive platform for comparing various financial products, services, and strategies. By leveraging COMPARE.EDU.VN, you can gain valuable insights and make informed decisions to improve your financial health.

8.1. Comparing Financial Products and Services

COMPARE.EDU.VN allows you to compare financial products and services, such as credit cards, loans, insurance policies, and investment accounts, to find the best options for your needs and budget.

8.2. Accessing Expert Reviews and Ratings

COMPARE.EDU.VN provides access to expert reviews and ratings of financial products and services, helping you make informed decisions based on objective assessments.

8.3. Using COMPARE.EDU.VN to Make Informed Decisions

By using COMPARE.EDU.VN, you can gather the information you need to make informed financial decisions, optimize your financial strategies, and improve your overall financial standing.

9. Avoiding Common Pitfalls in Financial Comparison

While financial comparison can be helpful, it’s essential to avoid common pitfalls that can lead to stress, anxiety, and poor financial decisions.

9.1. Focusing Too Much on Others

Focusing too much on others can lead to feelings of inadequacy and dissatisfaction. Remember that everyone’s financial situation is unique, and it’s essential to focus on your own goals and progress.

9.2. Ignoring Your Own Goals and Values

Financial comparison should not overshadow your own goals and values. Make sure your financial decisions align with what’s important to you and your long-term objectives.

9.3. Making Unrealistic Comparisons

Making unrealistic comparisons, such as comparing yourself to individuals with significantly different circumstances, can be demotivating and lead to poor financial decisions.

9.4. Taking on Too Much Risk

Taking on too much risk in an attempt to catch up financially can backfire and jeopardize your financial security. Make sure your investment decisions align with your risk tolerance and time horizon.

10. Frequently Asked Questions (FAQ)

Q1: How often should I compare my financial standing to others?

A: Comparing your financial standing annually is a good practice to track progress and make necessary adjustments.

Q2: What is a good net worth for my age?

A: A good net worth depends on several factors, including income, savings rate, and lifestyle. Use net worth percentiles and averages as benchmarks, but focus on your own goals and progress.

Q3: How can I increase my savings rate?

A: Increase your savings rate by cutting unnecessary expenses, automating savings, and increasing your income.

Q4: What is a healthy debt-to-income ratio?

A: A debt-to-income ratio of 36% or less is generally considered healthy.

Q5: How does home equity affect my net worth?

A: Home equity is considered an asset and is included in your net worth calculation.

Q6: What are the best investment strategies for long-term growth?

A: Diversifying your investments and aligning your investments with your risk tolerance are key strategies for long-term growth.

Q7: How can a financial advisor help me improve my financial standing?

A: A financial advisor can provide personalized advice and guidance on budgeting, saving, investing, and debt management.

Q8: What are some common financial mistakes to avoid?

A: Common financial mistakes include overspending, taking on too much debt, and not saving for retirement.

Q9: How can I create a budget that works for me?

A: Track your income and expenses, set financial goals, and prioritize your spending to create a budget that aligns with your needs and values.

Q10: Where can I find reliable financial information and resources?

A: You can find reliable financial information and resources on government websites, financial planning websites, and from qualified financial advisors.

Conclusion

Comparing your financial standing to others your age can provide valuable insights and motivation to improve your financial health. By focusing on key metrics, understanding net worth percentiles and averages, and leveraging resources like COMPARE.EDU.VN, you can make informed decisions and achieve your financial goals. Remember to avoid common pitfalls and focus on your own unique circumstances and objectives.

For further assistance and personalized financial comparisons, visit compare.edu.vn at COMPARE.EDU.VN or contact us at 333 Comparison Plaza, Choice City, CA 90210, United States, or via Whatsapp at +1 (626) 555-9090. Our team is ready to help you make informed financial decisions.