Are you trying to understand the landscape of wealth management fees? At COMPARE.EDU.VN, we help you navigate the complexities of financial planning. This article provides a detailed comparison of wealth management fee structures, enabling you to make informed decisions and secure your financial future. We’ll explore different fee models, including asset-based fees, flat fees, and performance-based fees.

1. What Exactly Are Wealth Management Fees?

Wealth management fees are the costs associated with hiring a professional to manage your finances. These fees cover a range of services, including investment management, financial planning, retirement planning, and estate planning. The fees can vary widely depending on the provider, the services offered, and the complexity of your financial situation.

1.1. Why Understanding Wealth Management Fees is Crucial

Understanding wealth management fees is crucial because these expenses directly impact your investment returns and overall financial health. High fees can erode your wealth over time, while transparent and reasonable fees ensure you receive value for the services provided. According to a study by the U.S. Securities and Exchange Commission (SEC), even small differences in fees can significantly affect long-term investment outcomes.

1.2. The Role of COMPARE.EDU.VN in Fee Transparency

COMPARE.EDU.VN is dedicated to providing clear, unbiased comparisons of wealth management fees. Our platform helps you evaluate different advisors and services, ensuring you find the best fit for your financial goals and budget.

2. Different Types of Wealth Management Fees

Wealth management firms employ various fee structures. Understanding these different models is essential for evaluating the cost-effectiveness of their services.

2.1. Asset-Based Fees (AUM)

Asset-based fees, also known as Assets Under Management (AUM) fees, are the most common fee structure in the wealth management industry. Advisors charge a percentage of the total assets they manage on your behalf.

2.1.1. How AUM Fees Work

AUM fees are typically calculated as a percentage of your total assets under management. For example, an advisor might charge 1% AUM annually. If they manage a $1 million portfolio for you, the annual fee would be $10,000.

2.1.2. Pros and Cons of AUM Fees

Pros:

- Simple and Transparent: Easy to understand and calculate.

- Aligned Interests: The advisor’s compensation increases as your portfolio grows.

Cons:

- Can Be Expensive: Percentage-based fees can be costly for larger portfolios.

- Potential for Overcharging: May not accurately reflect the complexity of the work involved.

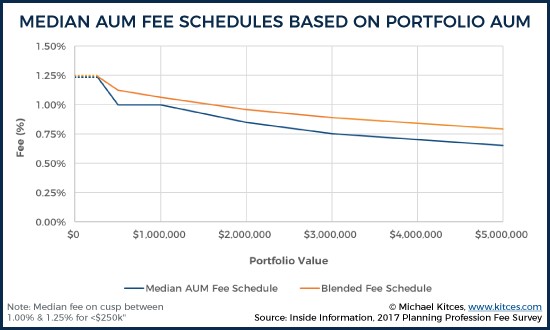

2.1.3. Average AUM Fee Rates

According to a 2023 study by AdvisoryHQ, the average AUM fee is around 1% for portfolios up to $1 million. However, this rate often decreases for larger portfolios. The following table shows typical AUM fee rates based on portfolio size:

| Portfolio Size | Average AUM Fee |

|---|---|

| Up to $1 million | 1.00% |

| $1 million – $5 million | 0.75% |

| $5 million – $10 million | 0.50% |

| Over $10 million | 0.25% |

Wealth management AUM fees based on portfolio size

Wealth management AUM fees based on portfolio size

2.2. Flat Fees

Flat fees involve a fixed annual or monthly charge for wealth management services, regardless of the size of your portfolio.

2.2.1. How Flat Fees Work

With a flat fee arrangement, you pay a set amount for a specific set of services. This fee is agreed upon in advance and remains consistent throughout the engagement.

2.2.2. Pros and Cons of Flat Fees

Pros:

- Predictable Costs: Easy to budget and plan for.

- Potentially Lower Cost: Can be more affordable for larger portfolios with simpler needs.

Cons:

- May Not Reflect Complexity: Fixed fee may not account for significant changes in your financial situation.

- Potential for Underservice: Advisors may be less motivated to provide comprehensive service.

2.2.3. Average Flat Fee Rates

Flat fees can range from a few thousand dollars per year for basic financial planning to tens of thousands for comprehensive wealth management services. A 2022 report by Financial Planning Association (FPA) found that average flat fees for financial planning range from $2,000 to $10,000 annually, depending on the scope of services.

2.3. Hourly Fees

Hourly fees involve paying an advisor for the time they spend working on your financial plan.

2.3.1. How Hourly Fees Work

Advisors track their time and bill you at an agreed-upon hourly rate. This fee structure is common for specific projects or consultations.

2.3.2. Pros and Cons of Hourly Fees

Pros:

- Pay for What You Need: Only pay for the specific services you use.

- Good for Limited Engagements: Ideal for one-time consultations or focused projects.

Cons:

- Unpredictable Costs: Difficult to estimate the total cost in advance.

- Potential for Overbilling: Requires careful monitoring of time spent by the advisor.

2.3.3. Average Hourly Fee Rates

Hourly rates for financial advisors typically range from $100 to $400 per hour, depending on their experience and credentials. A 2023 survey by NerdWallet found that the average hourly fee for a financial planner is around $250.

2.4. Performance-Based Fees

Performance-based fees, also known as incentive fees, are based on the performance of your investment portfolio. Advisors earn a percentage of the profits they generate for you.

2.4.1. How Performance-Based Fees Work

Advisors receive a fee based on the extent to which your portfolio’s returns exceed a predetermined benchmark. For example, an advisor might earn 20% of the profits above a specified index return.

2.4.2. Pros and Cons of Performance-Based Fees

Pros:

- Incentive for High Returns: Advisors are highly motivated to maximize your investment gains.

- Pay for Success: Only pay if the advisor delivers strong performance.

Cons:

- Higher Risk: Advisors may take on excessive risk to achieve higher returns.

- Potential for Conflict of Interest: Can incentivize short-term gains over long-term financial health.

2.4.3. Regulations for Performance-Based Fees

Performance-based fees are subject to specific regulations. In the United States, the Investment Advisers Act of 1940 restricts the use of performance fees to clients with a net worth of at least $2.2 million or assets under management of at least $1.1 million.

2.5. Commission-Based Fees

Commission-based fees involve advisors earning a commission on the financial products they sell to you.

2.5.1. How Commission-Based Fees Work

Advisors receive a percentage of the sale price of products like insurance policies, mutual funds, and annuities.

2.5.2. Pros and Cons of Commission-Based Fees

Pros:

- No Upfront Cost: You don’t pay directly for advice.

- Simple to Understand: Easy to see how the advisor is compensated.

Cons:

- Potential for Bias: Advisors may recommend products that generate higher commissions, even if they are not the best fit for your needs.

- Lack of Transparency: Difficult to assess the true cost of the advice.

2.5.3. The Shift Away from Commission-Based Fees

Due to the potential for conflicts of interest, there’s a growing trend away from commission-based fees in favor of fee-only advisors who act as fiduciaries, prioritizing your best interests.

3. Additional Costs to Consider

Beyond the primary fee structure, several additional costs can impact the overall expense of wealth management services.

3.1. Expense Ratios

Expense ratios are the annual fees charged by mutual funds and ETFs to cover their operating expenses. These fees are deducted directly from the fund’s assets and impact your investment returns.

3.1.1. How Expense Ratios Affect Returns

Even small differences in expense ratios can have a significant impact over time. For example, a fund with a 0.25% expense ratio will generate higher returns than a similar fund with a 1% expense ratio, assuming all other factors are equal.

3.1.2. Strategies for Minimizing Expense Ratios

Consider investing in low-cost index funds and ETFs to minimize expense ratios. These passively managed funds typically have lower fees compared to actively managed funds.

3.2. Transaction Costs

Transaction costs include brokerage fees, commissions, and other charges associated with buying and selling investments.

3.2.1. Impact of Transaction Costs

Frequent trading can lead to higher transaction costs, eroding your investment returns.

3.2.2. Minimizing Transaction Costs

Opt for a buy-and-hold investment strategy to reduce the frequency of trades. Additionally, consider using a brokerage that offers commission-free trading.

3.3. Custodial Fees

Custodial fees are charged by the financial institution that holds your assets. These fees cover the cost of account maintenance, reporting, and other administrative services.

3.3.1. Understanding Custodial Fees

Custodial fees can be a flat annual fee or a percentage of your assets. They vary depending on the custodian and the services provided.

3.3.2. Negotiating Custodial Fees

In some cases, you may be able to negotiate lower custodial fees, especially for larger accounts.

3.4. Hidden Fees

Hidden fees are charges that are not clearly disclosed or are buried in the fine print of your agreement with a wealth manager.

3.4.1. Examples of Hidden Fees

Examples include account maintenance fees, wire transfer fees, and inactivity fees.

3.4.2. How to Identify and Avoid Hidden Fees

Carefully review your agreement with the wealth manager and ask for a clear explanation of all fees and charges.

4. How to Compare Wealth Management Fees Effectively

Comparing wealth management fees requires a comprehensive approach. Consider the following steps to ensure you make an informed decision.

4.1. Define Your Financial Goals

Clearly define your financial goals and objectives. This will help you determine the types of services you need and the appropriate fee structure.

4.2. Understand Your Risk Tolerance

Assess your risk tolerance to ensure your investment strategy aligns with your comfort level.

4.3. Evaluate Different Fee Structures

Evaluate the pros and cons of each fee structure and determine which one best fits your needs and financial situation.

4.4. Compare Multiple Advisors

Get quotes from multiple advisors and compare their fees, services, and investment strategies.

4.5. Check Credentials and Reputation

Verify the credentials and reputation of the advisors you are considering. Look for certifications like Certified Financial Planner (CFP) and Chartered Financial Analyst (CFA).

4.6. Read Client Reviews

Read client reviews and testimonials to get a sense of the advisor’s service quality and client satisfaction.

4.7. Ask About Conflicts of Interest

Ask potential advisors about any conflicts of interest they may have. Fee-only advisors who act as fiduciaries are generally considered to have fewer conflicts of interest compared to commission-based advisors.

4.8. Review the Fine Print

Carefully review the fine print of your agreement with the wealth manager, including all fees, terms, and conditions.

5. Factors That Influence Wealth Management Fees

Several factors influence the fees charged by wealth management firms.

5.1. Portfolio Size

Larger portfolios typically qualify for lower AUM fee rates due to economies of scale.

5.2. Complexity of Services

More complex financial situations require more extensive planning and management, which can result in higher fees.

5.3. Advisor Experience and Credentials

More experienced and highly credentialed advisors often charge higher fees due to their expertise and track record.

5.4. Geographic Location

Fees can vary depending on the geographic location of the advisor, with some areas having higher costs of living and operating expenses.

5.5. Market Conditions

Market volatility and economic uncertainty can impact fees, as advisors may need to spend more time managing risk and adjusting investment strategies.

6. Negotiating Wealth Management Fees

Negotiating wealth management fees is possible, especially for larger portfolios or simpler financial situations.

6.1. Strategies for Negotiating Fees

- Do Your Research: Understand the average fees charged by advisors in your area.

- Be Prepared to Walk Away: Be willing to consider other advisors if you can’t reach an agreement on fees.

- Highlight Your Assets: Emphasize the size and simplicity of your portfolio.

- Ask for Discounts: Inquire about discounts for long-term clients or referrals.

- Consider Fee-Only Advisors: Fee-only advisors may be more willing to negotiate fees compared to commission-based advisors.

6.2. When to Consider a Different Advisor

If you are not satisfied with the fees or services provided by your current advisor, consider switching to a different firm that better aligns with your needs and budget.

7. The Future of Wealth Management Fees

The wealth management industry is evolving, with new technologies and business models impacting fee structures.

7.1. The Rise of Robo-Advisors

Robo-advisors are automated investment platforms that offer low-cost investment management services. These platforms typically charge AUM fees of 0.25% to 0.50%, significantly lower than traditional wealth managers.

7.1.1. How Robo-Advisors Are Disrupting the Industry

Robo-advisors are disrupting the industry by offering affordable and accessible investment management services to a wider range of investors.

7.1.2. Limitations of Robo-Advisors

Robo-advisors have limitations, including a lack of personalized advice and limited financial planning services.

7.2. The Growing Demand for Fee Transparency

Investors are increasingly demanding fee transparency and value for their money. This is driving a shift towards simpler and more transparent fee structures.

7.3. The Impact of Technology on Fees

Technology is helping to reduce costs and improve efficiency in the wealth management industry. This is leading to lower fees and better services for investors.

8. Case Studies: Comparing Wealth Management Fees in Practice

To illustrate the importance of comparing wealth management fees, let’s look at a few case studies.

8.1. Case Study 1: High-Net-Worth Investor

A high-net-worth investor with a $5 million portfolio is considering two wealth managers. Advisor A charges 1% AUM, while Advisor B charges 0.50% AUM. Over 20 years, the difference in fees could amount to hundreds of thousands of dollars.

8.2. Case Study 2: Young Professional

A young professional with a $100,000 portfolio is deciding between a traditional wealth manager and a robo-advisor. The robo-advisor charges 0.25% AUM, while the traditional advisor charges 1% AUM. The robo-advisor could save the investor $750 per year.

8.3. Case Study 3: Retirement Planning

An individual seeking retirement planning services is comparing two advisors. Advisor A charges an hourly fee of $300, while Advisor B charges a flat fee of $5,000. Depending on the complexity of the plan, the hourly fee could be more or less expensive than the flat fee.

9. Key Takeaways for Choosing a Wealth Manager

Choosing a wealth manager is a significant decision. Keep the following key takeaways in mind.

9.1. Understand Your Needs and Goals

Clearly define your financial needs and goals before hiring a wealth manager.

9.2. Compare Fees and Services

Compare the fees and services offered by multiple advisors.

9.3. Verify Credentials and Reputation

Check the credentials and reputation of potential advisors.

9.4. Look for Transparency

Look for advisors who are transparent about their fees and potential conflicts of interest.

9.5. Consider Fee-Only Fiduciaries

Consider working with fee-only advisors who act as fiduciaries.

10. Frequently Asked Questions (FAQs) About Wealth Management Fees

10.1. What is the average fee for a financial advisor?

The average fee for a financial advisor typically ranges from 1% to 2% of assets under management (AUM). However, this can vary based on the size of your portfolio and the complexity of the services provided.

10.2. Are wealth management fees tax deductible?

Yes, certain wealth management fees may be tax deductible. According to the IRS, you can deduct expenses for investment advice and other costs related to managing your investments, subject to certain limitations.

10.3. What is a fee-only financial advisor?

A fee-only financial advisor is compensated solely by the fees they charge their clients. They do not receive commissions from selling financial products, reducing potential conflicts of interest.

10.4. What is a fiduciary?

A fiduciary is legally obligated to act in the best interests of their clients. They must put their clients’ needs ahead of their own.

10.5. How can I lower my wealth management fees?

You can lower your wealth management fees by negotiating with your advisor, investing in low-cost index funds, and avoiding frequent trading.

10.6. What questions should I ask a potential wealth manager?

Ask about their fees, services, investment strategy, credentials, and potential conflicts of interest.

10.7. Is it worth paying for a wealth manager?

Whether it’s worth paying for a wealth manager depends on your financial situation and needs. A good wealth manager can provide valuable advice and help you achieve your financial goals, but it’s important to weigh the costs and benefits.

10.8. What is the difference between financial planning and wealth management?

Financial planning typically focuses on creating a comprehensive plan to achieve your financial goals, while wealth management involves managing your investments and assets to grow your wealth over time.

10.9. How do robo-advisors compare to traditional wealth managers?

Robo-advisors offer low-cost, automated investment management services, while traditional wealth managers provide personalized advice and a wider range of financial planning services.

10.10. What are the signs of a bad financial advisor?

Signs of a bad financial advisor include high-pressure sales tactics, lack of transparency, poor communication, and a failure to act in your best interests.

Conclusion

Understanding and comparing wealth management fees is essential for making informed financial decisions. By evaluating different fee structures, considering additional costs, and negotiating fees, you can find a wealth manager who provides value and helps you achieve your financial goals. Remember, COMPARE.EDU.VN is here to assist you in comparing various options and making the best choice for your financial future.

Ready to take control of your financial future? Visit COMPARE.EDU.VN today to Compare Wealth Management Fees and find the right advisor for your needs. Our comprehensive comparisons and unbiased reviews will help you make an informed decision. Contact us at 333 Comparison Plaza, Choice City, CA 90210, United States, or call us at Whatsapp: +1 (626) 555-9090. Start comparing today and secure your financial future with compare.edu.vn. Let us help you find the perfect wealth management solution.