Understanding the landscape of taxes across the United States can be complex. When considering a move, evaluating business locations, or simply trying to understand where your tax dollars go furthest, comparing taxes between states is crucial. This in-depth guide, based on the latest research from the Tax Foundation, breaks down state and local tax burdens, offering a comprehensive comparison to help you make informed decisions.

{kind=link}

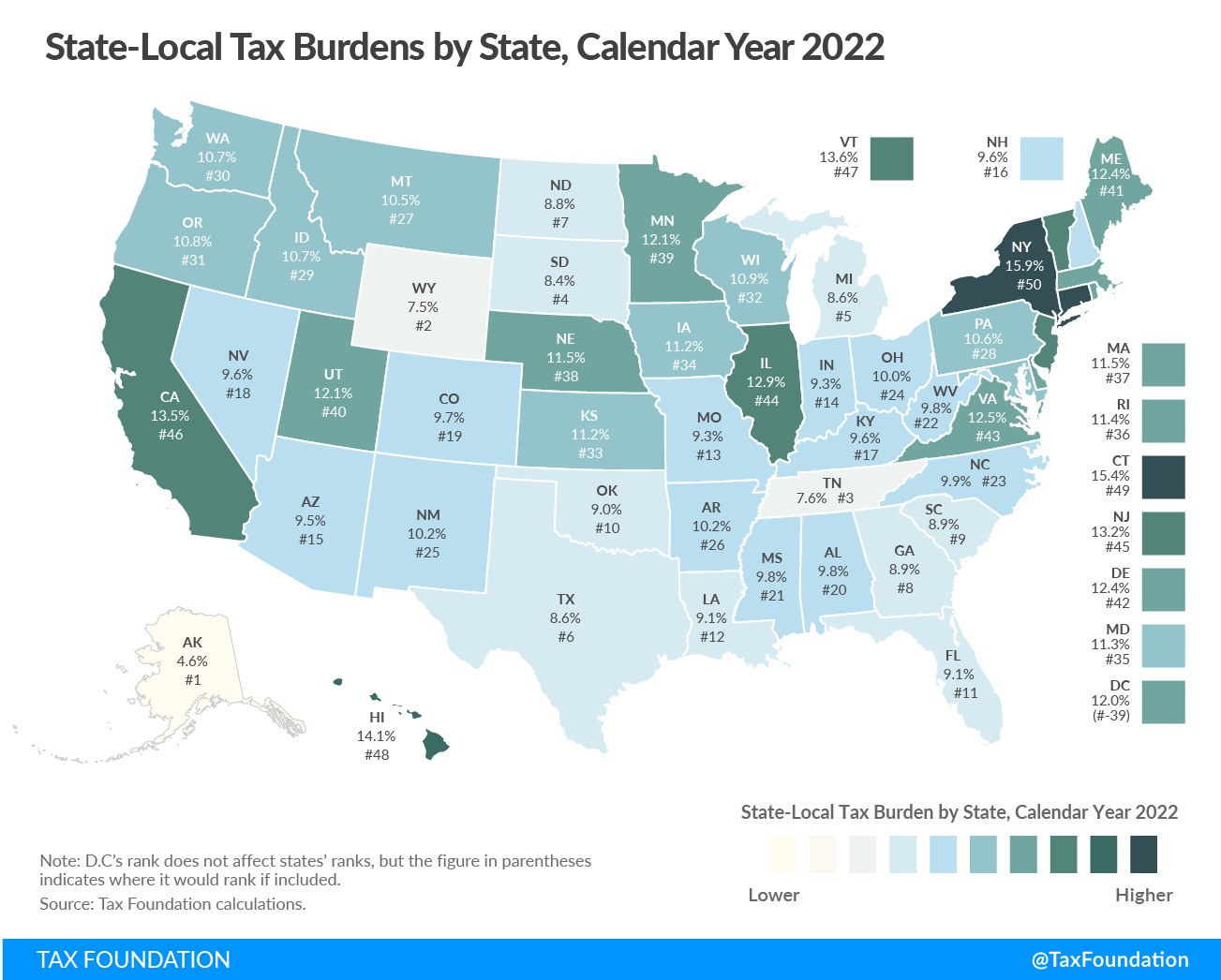

Image: Map of the United States illustrating the total state and local tax burden by percentage of income for each state in 2022, providing a visual comparison of tax burdens across the country.

Decoding State Tax Burdens: What They Really Mean

When we talk about comparing taxes between states, it’s essential to move beyond simply looking at tax rates. A more insightful metric is the state tax burden. This isn’t just about the taxes collected by a state, but rather the total amount of state and local taxes borne by a state’s residents, measured as a percentage of their income. This measure, developed and analyzed by experts at the Tax Foundation, accounts for taxes paid within the state as well as taxes paid to other states and localities due to economic activities across state lines.

This approach is critical because it acknowledges that residents often pay taxes to governments outside their state of residence. This can happen through various mechanisms, including:

- Interstate Commerce: People working or traveling across state lines pay taxes in multiple states.

- Tax Incidence Shifting: The economic burden of a tax can fall on individuals or entities different from those legally obligated to pay it.

- Tax Exporting: States can shift their tax burden to non-residents, for example, through taxes on tourism or natural resource extraction.

Therefore, simply comparing tax collections within a state to its income provides an incomplete and potentially misleading picture of the true tax burden on its residents. To accurately Compare Taxes Between States, we need to consider this broader concept of tax burden, which reflects the economic incidence of taxation.

Tax Incidence and Economic Burden: Understanding Who Really Pays

To effectively compare taxes between states, it’s crucial to grasp the concept of tax incidence. Tax incidence refers to who ultimately bears the burden of a tax, which can differ significantly from who is legally required to pay it. There are two types of tax incidence:

- Legal Incidence: This refers to the entity or individual legally responsible for remitting tax payments to the government. For example, businesses have the legal incidence of corporate income tax.

- Economic Incidence: This refers to who ultimately bears the economic cost of the tax. This burden can manifest in various forms, such as higher consumer prices, lower wages for workers, or reduced returns for investors.

The economic incidence is often shifted from those with the legal obligation due to behavioral changes in response to taxes. For instance, while corporations legally pay corporate income tax, a portion of this burden might be passed on to consumers through higher prices or to employees through lower wages.

When comparing taxes between states, focusing on economic incidence is key. It provides a more accurate understanding of the real cost of taxes for residents, businesses, and the overall economy. This perspective is especially important when considering interstate tax comparisons, as the economic burden of state taxes can be distributed across state lines.

The Phenomenon of Tax Exporting: How States Shift Burdens

A significant aspect of comparing taxes between states is understanding tax exporting. This occurs when a portion of a state’s tax burden is shifted to non-residents. States employ various strategies to export taxes, effectively reducing the tax burden on their own residents while collecting revenue. Common methods of tax exporting include:

- Severance Taxes: States rich in natural resources, like Alaska, North Dakota, and Wyoming, levy severance taxes on resource extraction. A significant portion of these taxes are borne by investors and consumers outside the state, as global markets often determine resource prices.

- Tourism Taxes: States with popular tourist destinations, such as Florida, Nevada, and Hawaii, can tax non-residents through levies on hotel stays, rental cars, restaurant meals, and sales taxes in tourist areas.

- Income Taxes on Non-Resident Workers: States with major employment centers that attract commuters from neighboring states may collect income taxes from non-residents who work within their borders.

Alaska stands out as a prime example of tax exporting. In 2022, a remarkable 60 percent of Alaska’s state and local tax revenue originated from non-residents, primarily due to oil extraction taxes. This ability to export taxes significantly lowers the tax burden on Alaskan residents, making it crucial to consider tax exporting when comparing taxes between states. States that effectively export a large portion of their taxes can appear to have lower tax burdens for their residents, even if their overall tax collections are substantial.

{kind=link}

Image: Bar chart illustrating the distribution of total combined state and local tax collections by taxpayer type in 2022, visually representing the concept of tax exporting and the proportion of taxes collected from non-residents.

Tax Burdens vs. Tax Collections: Why the Difference Matters for State Comparisons

When comparing taxes between states, it’s vital to distinguish between tax burdens and tax collections. These two metrics provide different perspectives on state finances and have distinct implications for residents.

- Tax Collections: Tax collections represent the total amount of tax revenue received by state and local governments. This data, often reported by the Census Bureau, reflects the legal incidence of taxes – who directly pays the taxes to the government. Tax collection data is valuable for understanding government revenue streams and the overall size of the public sector in a state.

- Tax Burdens: As previously defined, tax burdens represent the economic incidence of taxes, reflecting the actual burden borne by a state’s residents, regardless of where the taxes are legally collected. Tax burden estimates, like those from the Tax Foundation, adjust tax collection data to account for tax exporting and interstate tax shifting.

For comparing taxes between states in terms of resident impact, tax burden is the more relevant metric. Tax collections alone can be misleading because they don’t capture the extent to which states export taxes or shift burdens across state lines. For example, a state with high tourism might show high tax collections due to sales taxes, but the actual burden on its residents might be lower than tax collection figures suggest because tourists contribute significantly to the revenue.

Conversely, states like Connecticut, where residents work in New York City, may see their residents paying significant taxes to New York, which would be reflected in New York’s tax collections, not Connecticut’s. However, when calculating tax burdens, these payments are attributed to Connecticut residents.

Therefore, when aiming to compare the true cost of state and local taxes for residents across different states, analyzing tax burdens provides a more accurate and insightful comparison than simply looking at tax collection figures.

What Taxes are Included in State Tax Burden Comparisons?

To ensure a comprehensive and accurate comparison of taxes between states, it’s important to understand which taxes are included in the tax burden calculations. The Tax Foundation’s analysis, and similar comprehensive comparisons, typically encompass a wide range of state and local taxes, drawing upon data from sources like the Census Bureau’s State and Local Government Finance division. These taxes generally include:

- Property Taxes: Taxes on real estate and tangible personal property, a major source of local government revenue.

- General Sales Taxes: Taxes on retail sales of goods and services.

- Excise Taxes: Taxes on specific goods or activities, such as alcohol, tobacco, motor fuels, and amusements.

- License Taxes: Taxes on various licenses, including vehicle licenses, business licenses, and professional licenses.

- Individual Income Taxes: Taxes on personal income.

- Corporate Income Taxes: Taxes on corporate profits.

- Estate, Inheritance, and Gift Taxes: Taxes on the transfer of wealth.

- Documentary and Transfer Taxes: Taxes on transactions like real estate transfers.

- Severance Taxes: Taxes on the extraction of natural resources.

- Special Assessments: Charges for property improvements.

- Miscellaneous Taxes: Taxes not categorized elsewhere.

By including this broad spectrum of taxes, comparisons of tax burdens between states offer a holistic view of the total tax pressure within each state and provide a robust basis for evaluating the relative tax climates across the U.S.

Limitations of Tax Burden Comparisons: What They Don’t Tell You

While comparing tax burdens between states offers valuable insights, it’s important to recognize the limitations of this analysis. Tax burden measures, such as those presented here, are not:

- Measures of Government Size: Tax burden as a percentage of income does not directly reflect the overall size of government spending or the scope of public services in a state. A state with a high tax burden might also provide extensive public services, while a low-tax state may offer fewer services.

- Complete Burden of Taxation: Tax burden calculations typically focus on the direct financial burden of taxes. They do not fully account for other costs associated with taxation, such as:

- Compliance Costs: The time and expense businesses and individuals incur to comply with tax laws.

- Economic Efficiency Losses: Taxes can distort economic decisions and lead to inefficiencies, which are not directly measured in tax burden calculations.

- Reflections of Individual Taxpayer Experience: Tax burden figures are aggregate measures, representing the average tax burden for all residents of a state. Individual taxpayers’ experiences can vary significantly based on their income level, consumption patterns, and other factors.

Furthermore, these comparisons do not inherently evaluate the benefits derived from taxation. The revenue generated through taxes funds public services like education, infrastructure, public safety, and healthcare. A comprehensive comparison of states would ideally consider both the tax burden and the quality and extent of public services provided in return. Therefore, while comparing tax burdens is a crucial step in understanding state tax landscapes, it should be complemented by other analyses to provide a complete picture.

2022 State Tax Burden Rankings: Key Findings and State-by-State Analysis

The Tax Foundation’s analysis of 2022 data reveals significant variations in state and local tax burdens across the United States. These rankings provide a clear picture for comparing taxes between states, highlighting which states impose the highest and lowest burdens on their residents.

Table 1. State-Local Tax Burdens by State, Calendar Year 2022

| State | Effective Tax Rate | Rank |

|---|---|---|

| Alabama | 9.8% | 20 |

| Alaska | 4.6% | 1 |

| Arizona | 9.5% | 15 |

| Arkansas | 10.2% | 26 |

| California | 13.5% | 46 |

| Colorado | 9.7% | 19 |

| Connecticut | 15.4% | 49 |

| Delaware | 12.4% | 42 |

| District of Columbia | 12.0% | (39) |

| Florida | 9.1% | 11 |

| Georgia | 8.9% | 8 |

| Hawaii | 14.1% | 48 |

| Idaho | 10.7% | 29 |

| Illinois | 12.9% | 44 |

| Indiana | 9.3% | 14 |

| Iowa | 11.2% | 34 |

| Kansas | 11.2% | 33 |

| Kentucky | 9.6% | 17 |

| Louisiana | 9.1% | 12 |

| Maine | 12.4% | 41 |

| Maryland | 11.3% | 35 |

| Massachusetts | 11.5% | 37 |

| Michigan | 8.6% | 5 |

| Minnesota | 12.1% | 39 |

| Mississippi | 9.8% | 21 |

| Missouri | 9.3% | 13 |

| Montana | 10.5% | 27 |

| Nebraska | 11.5% | 38 |

| Nevada | 9.6% | 18 |

| New Hampshire | 9.6% | 16 |

| New Jersey | 13.2% | 45 |

| New Mexico | 10.2% | 25 |

| New York | 15.9% | 50 |

| North Carolina | 9.9% | 23 |

| North Dakota | 8.8% | 7 |

| Ohio | 10.0% | 24 |

| Oklahoma | 9.0% | 10 |

| Oregon | 10.8% | 31 |

| Pennsylvania | 10.6% | 28 |

| Rhode Island | 11.4% | 36 |

| South Carolina | 8.9% | 9 |

| South Dakota | 8.4% | 4 |

| Tennessee | 7.6% | 3 |

| Texas | 8.6% | 6 |

| Utah | 12.1% | 40 |

| Vermont | 13.6% | 47 |

| Virginia | 12.5% | 43 |

| Washington | 10.7% | 30 |

| West Virginia | 9.8% | 22 |

| Wisconsin | 10.9% | 32 |

| Wyoming | 7.5% | 2 |

Key Observations from the 2022 Rankings:

- Highest Tax Burdens: New York (15.9%), Connecticut (15.4%), and Hawaii (14.1%) consistently rank as the states with the highest tax burdens. These states often have higher expenditure levels and rely more heavily on various taxes.

- Lowest Tax Burdens: Alaska (4.6%), Wyoming (7.5%), and Tennessee (7.6%) exhibit the lowest tax burdens. These states often benefit from natural resource revenues (Alaska and Wyoming) or have chosen to forgo major taxes like state income tax (Tennessee, Alaska, Wyoming, South Dakota, Texas, Florida).

- National Average: The average state-local tax burden across the U.S. was approximately 11.6% in 2022, with a median of 10.2%. This indicates a clustering of states around the middle range, although significant disparities exist at the extremes.

- Impact of Pandemic Era: The data reflects the economic shifts during the pandemic, with overall tax burdens slightly increasing due to rising net national product and state and local tax collections.

Table 2. State-Local Tax Burdens by State (with Detailed Breakdown), Calendar Year 2022

| State | State-Local Effective Tax Rate | Rank | State-Local Tax Burden per Capita | Taxes Paid to Own State per Capita | Taxes Paid to Other States Per Capita |

|---|---|---|---|---|---|

| Alabama | 9.80% | 20 | $4,585 | $3,578 | $1,007 |

| Alaska | 4.60% | 1 | $2,943 | $1,527 | $1,416 |

| Arizona | 9.50% | 15 | $5,156 | $3,997 | $1,159 |

| Arkansas | 10.20% | 26 | $5,031 | $3,598 | $1,433 |

| California | 13.50% | 46 | $10,167 | $8,711 | $1,457 |

| Colorado | 9.70% | 19 | $6,699 | $5,010 | $1,689 |

| Connecticut | 15.40% | 49 | $12,151 | $9,883 | $2,268 |

| Delaware | 12.40% | 42 | $7,170 | $5,580 | $1,591 |

| District of Columbia | 12.00% | -39 | $11,654 | $9,060 | $2,594 |

| Florida | 9.10% | 11 | $5,406 | $3,533 | $1,873 |

| Georgia | 8.90% | 8 | $4,862 | $3,711 | $1,151 |

| Hawaii | 14.10% | 48 | $8,410 | $7,082 | $1,328 |

| Idaho | 10.70% | 29 | $5,402 | $4,140 | $1,262 |

| Illinois | 12.90% | 44 | $8,390 | $6,866 | $1,523 |

| Indiana | 9.30% | 14 | $5,030 | $3,965 | $1,064 |

| Iowa | 11.20% | 34 | $6,086 | $4,812 | $1,274 |

| Kansas | 11.20% | 33 | $6,353 | $4,971 | $1,382 |

| Kentucky | 9.60% | 17 | $4,669 | $3,679 | $990 |

| Louisiana | 9.10% | 12 | $4,762 | $3,705 | $1,056 |

| Maine | 12.40% | 41 | $6,906 | $5,712 | $1,194 |

| Maryland | 11.30% | 35 | $7,680 | $5,940 | $1,740 |

| Massachusetts | 11.50% | 37 | $9,405 | $7,565 | $1,840 |

| Michigan | 8.60% | 5 | $4,720 | $3,595 | $1,125 |

| Minnesota | 12.10% | 39 | $7,763 | $6,316 | $1,448 |

| Mississippi | 9.80% | 21 | $4,220 | $3,422 | $798 |

| Missouri | 9.30% | 13 | $4,953 | $3,666 | $1,287 |

| Montana | 10.50% | 27 | $5,795 | $4,200 | $1,595 |

| Nebraska | 11.50% | 38 | $6,720 | $5,327 | $1,393 |

| Nevada | 9.60% | 18 | $5,554 | $3,932 | $1,622 |

| New Hampshire | 9.60% | 16 | $6,593 | $4,784 | $1,809 |

| New Jersey | 13.20% | 45 | $9,648 | $7,696 | $1,952 |

| New Mexico | 10.20% | 25 | $4,835 | $3,859 | $977 |

| New York | 15.90% | 50 | $12,083 | $10,380 | $1,702 |

| North Carolina | 9.90% | 23 | $5,299 | $4,156 | $1,143 |

| North Dakota | 8.80% | 7 | $5,403 | $3,800 | $1,603 |

| Ohio | 10.00% | 24 | $5,530 | $4,380 | $1,149 |

| Oklahoma | 9.00% | 10 | $4,527 | $3,380 | $1,148 |

| Oregon | 10.80% | 31 | $6,572 | $5,191 | $1,381 |

| Pennsylvania | 10.60% | 28 | $6,723 | $5,354 | $1,369 |

| Rhode Island | 11.40% | 36 | $6,948 | $5,273 | $1,675 |

| South Carolina | 8.90% | 9 | $4,596 | $3,365 | $1,231 |

| South Dakota | 8.40% | 4 | $5,196 | $3,526 | $1,670 |

| Tennessee | 7.60% | 3 | $4,036 | $3,082 | $954 |

| Texas | 8.60% | 6 | $4,994 | $3,849 | $1,146 |

| Utah | 12.10% | 40 | $6,750 | $5,346 | $1,404 |

| Vermont | 13.60% | 47 | $7,958 | $6,532 | $1,426 |

| Virginia | 12.50% | 43 | $7,979 | $6,367 | $1,612 |

| Washington | 10.70% | 30 | $7,803 | $6,069 | $1,734 |

| West Virginia | 9.80% | 22 | $4,479 | $3,444 | $1,034 |

| Wisconsin | 10.90% | 32 | $6,231 | $4,911 | $1,320 |

| Wyoming | 7.50% | 2 | $4,691 | $2,647 | $2,045 |

This detailed breakdown further illustrates how tax burdens are composed, showing both taxes paid to a state’s own government and taxes paid to other states. States like Connecticut and New Jersey, while having high in-state tax payments, also see significant out-of-state tax burdens, contributing to their overall high rankings. Conversely, states like Alaska and Wyoming, despite lower in-state taxes, still have notable out-of-state tax burdens due to factors like severance taxes impacting residents nationwide through investment channels.

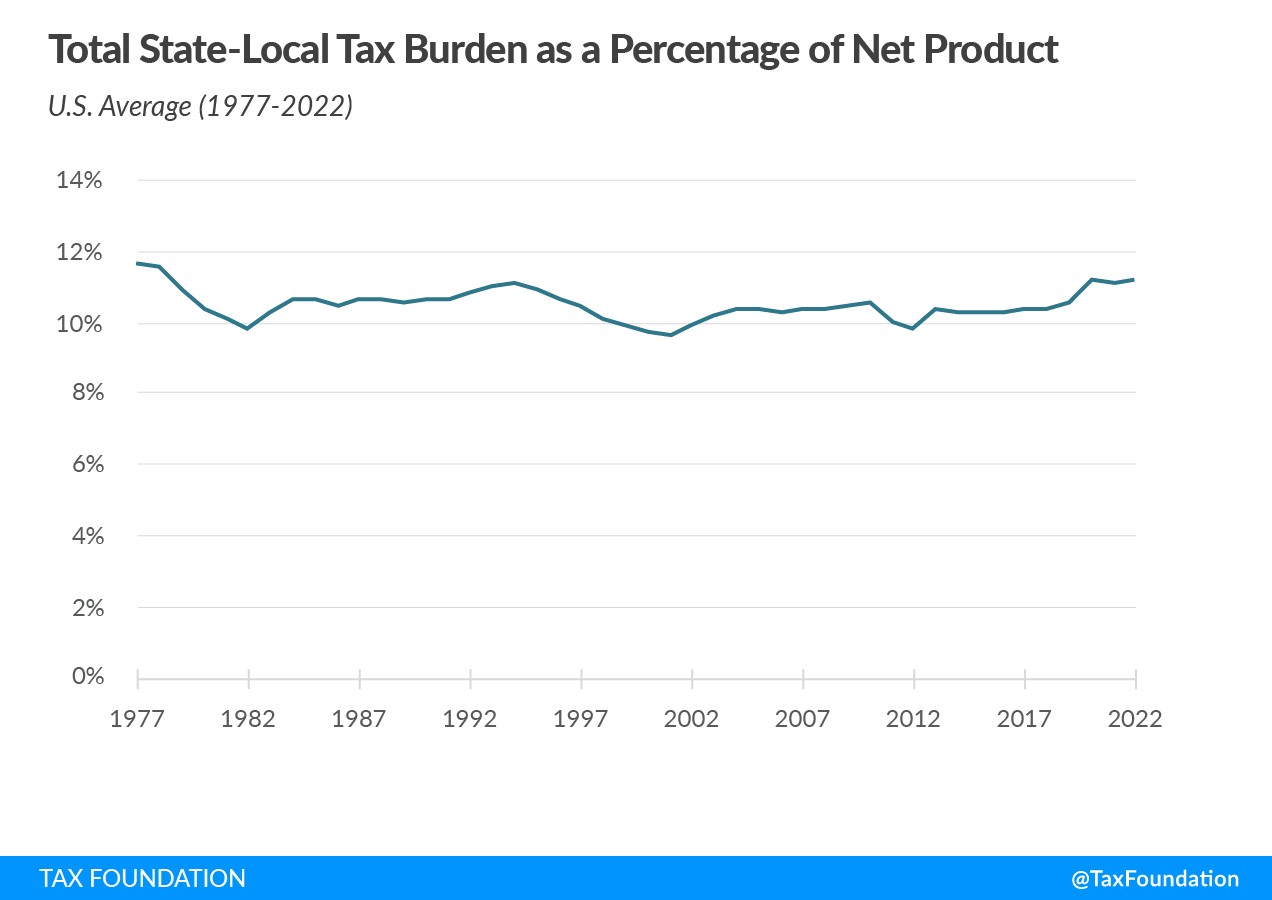

Long-Term Trends in State Tax Burdens: A Historical Perspective

Comparing taxes between states isn’t just about a snapshot in time. Examining historical trends provides valuable context and reveals how state tax burdens have evolved. Nationally, the average state-local tax burden as a percentage of income has seen some fluctuation, but has remained relatively stable over the long term.

Table 3. State-Local Tax Burdens as a Percentage of Net Product, 2020-2022

| Burden Percentages and Rankings |

|---|

| 2019 |

| State |

| U.S. Average |

| Alabama |

| Alaska |

| Arizona |

| Arkansas |

| California |

| Colorado |

| Connecticut |

| Delaware |

| District of Columbia |

| Florida |

| Georgia |

| Hawaii |

| Idaho |

| Illinois |

| Indiana |

| Iowa |

| Kansas |

| Kentucky |

| Louisiana |

| Maine |

| Maryland |

| Massachusetts |

| Michigan |

| Minnesota |

| Mississippi |

| Missouri |

| Montana |

| Nebraska |

| Nevada |

| New Hampshire |

| New Jersey |

| New Mexico |

| New York |

| North Carolina |

| North Dakota |

| Ohio |

| Oklahoma |

| Oregon |

| Pennsylvania |

| Rhode Island |

| South Carolina |

| South Dakota |

| Tennessee |

| Texas |

| Utah |

| Vermont |

| Virginia |

| Washington |

| West Virginia |

| Wisconsin |

| Wyoming |

Table 4. State-Local Tax Burdens as a Percentage of State Income by State, Selected Years

| State | 1977 | 1980 | 1990 | 2000 | 2010 | 2015 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|---|---|---|---|

| U.S. Average | 11.7% | 10.4% | 10.7% | 9.7% | 10.6% | 10.3% | 10.6% | 11.2% | 11.2% | 11.2% |

| Alabama | 10.1% | 9.3% | 9.5% | 8.8% | 9.2% | 8.7% | 9.1% | 10.0% | 10.0% | 9.8% |

| Alaska | 12.7% | 8.9% | 6.1% | 5.1% | 7.2% | 5.8% | 5.6% | 5.0% | 4.1% | 4.6% |

| Arizona | 11.7% | 10.2% | 10.7% | 8.9% | 9.2% | 8.9% | 9.4% | 9.8% | 9.6% | 9.5% |

| Arkansas | 9.4% | 9.2% | 9.3% | 9.4% | 10.8% | 10.4% | 10.3% | 10.9% | 10.7% | 10.2% |

| California | 13.3% | 11.4% | 11.3% | 10.7% | 12.0% | 11.4% | 12.2% | 12.9% | 13.3% | 13.5% |

| Colorado | 11.6% | 10.0% | 10.4% | 8.9% | 9.5% | 9.4% | 9.6% | 10.1% | 10.0% | 9.7% |

| Connecticut | 12.1% | 10.5% | 11.1% | 11.3% | 12.9% | 11.9% | 12.5% | 13.7% | 14.7% | 15.4% |

| Delaware | 10.9% | 10.3% | 9.2% | 8.6% | 9.7% | 9.7% | 11.3% | 12.2% | 12.2% | 12.4% |

| District of Columbia | 13.4% | 13.8% | 12.9% | 11.5% | 9.8% | 10.1% | 11.0% | 11.6% | 11.7% | 12.0% |

| Florida | 10.2% | 8.7% | 9.2% | 8.6% | 10.0% | 9.0% | 8.9% | 9.2% | 9.1% | 9.1% |

| Georgia | 10.5% | 9.9% | 10.5% | 9.3% | 9.5% | 9.0% | 9.0% | 9.4% | 9.1% | 8.9% |

| Hawaii | 11.6% | 11.0% | 10.6% | 9.9% | 10.8% | 12.1% | 13.2% | 13.7% | 13.9% | 14.1% |

| Idaho | 11.7% | 10.5% | 11.0% | 10.2% | 10.0% | 9.7% | 9.5% | 10.2% | 10.8% | 10.7% |

| Illinois | 11.5% | 10.6% | 10.6% | 9.4% | 10.9% | 11.0% | 11.2% | 12.5% | 12.9% | 12.9% |

| Indiana | 9.4% | 8.3% | 9.5% | 8.4% | 9.9% | 8.9% | 9.0% | 9.3% | 9.3% | 9.3% |

| Iowa | 11.5% | 10.7% | 11.0% | 9.5% | 10.0% | 10.3% | 11.0% | 11.8% | 11.5% | 11.2% |

| Kansas | 10.6% | 9.6% | 10.3% | 9.6% | 10.1% | 9.1% | 10.2% | 10.8% | 11.1% | 11.2% |

| Kentucky | 10.7% | 9.8% | 10.3% | 10.0% | 9.7% | 9.7% | 9.8% | 10.2% | 10.0% | 9.6% |

| Louisiana | 8.6% | 8.0% | 8.5% | 8.4% | 8.2% | 8.4% | 8.9% | 9.3% | 9.1% | 9.1% |

| Maine | 11.4% | 10.9% | 11.5% | 10.9% | 10.9% | 11.2% | 11.6% | 12.1% | 12.4% | 12.4% |

| Maryland | 12.6% | 11.6% | 11.6% | 10.6% | 10.9% | 11.5% | 11.9% | 12.6% | 11.9% | 11.3% |

| Massachusetts | 13.4% | 12.1% | 11.4% | 10.0% | 10.9% | 10.7% | 10.8% | 11.4% | 11.4% | 11.5% |

| Michigan | 11.7% | 10.6% | 10.6% | 9.6% | 10.2% | 9.8% | 9.6% | 9.6% | 9.0% | 8.6% |

| Minnesota | 12.3% | 10.9% | 11.5% | 10.3% | 11.3% | 11.9% | 12.3% | 12.7% | 12.4% | 12.1% |

| Mississippi | 10.5% | 9.4% | 9.5% | 9.1% | 9.3% | 9.4% | 9.4% | 9.8% | 9.8% | 9.8% |

| Missouri | 10.3% | 9.4% | 9.9% | 9.3% | 9.5% | 9.0% | 9.0% | 9.5% | 9.4% | 9.3% |

| Montana | 10.8% | 9.6% | 10.0% | 8.9% | 9.5% | 10.1% | 10.2% | 10.8% | 10.7% | 10.5% |

| Nebraska | 12.1% | 10.8% | 10.3% | 9.6% | 10.2% | 10.1% | 10.8% | 11.7% | 11.7% | 11.5% |

| Nevada | 9.4% | 7.8% | 8.2% | 7.2% | 8.8% | 9.4% | 9.4% | 10.2% | 9.9% | 9.6% |

| New Hampshire | 9.9% | 8.5% | 8.6% | 7.7% | 8.8% | 9.8% | 9.2% | 9.4% | 9.5% | 9.6% |

| New Jersey | 13.9% | 12.1% | 11.9% | 11.0% | 13.0% | 11.5% | 11.9% | 12.8% | 13.0% | 13.2% |

| New Mexico | 10.1% | 9.3% | 10.8% | 9.9% | 9.1% | 9.3% | 10.5% | 11.6% | 10.5% | 10.2% |

| New York | 14.7% | 13.2% | 13.1% | 11.7% | 13.2% | 14.5% | 14.2% | 14.9% | 15.2% | 15.9% |

| North Carolina | 10.9% | 10.2% | 10.5% | 9.7% | 10.5% | 9.8% | 9.6% | 10.1% | 10.1% | 9.9% |

| North Dakota | 13.0% | 10.8% | 10.4% | 9.4% | 9.5% | 9.7% | 9.2% | 9.9% | 7.9% | 8.8% |

| Ohio | 9.9% | 9.2% | 10.5% | 10.2% | 10.2% | 10.1% | 10.1% | 10.6% | 10.4% | 10.0% |

| Oklahoma | 9.7% | 8.7% | 10.0% | 9.7% | 9.3% | 8.2% | 8.8% | 9.6% | 9.0% | 9.0% |

| Oregon | 12.4% | 11.2% | 11.8% | 10.1% | 10.9% | 11.2% | 11.7% | 11.9% | 11.1% | 10.8% |

| Pennsylvania | 11.5% | 10.7% | 10.6% | 9.9% | 10.6% | 10.1% | 10.4% | 10.8% | 10.7% | 10.6% |

| Rhode Island | 12.7% | 11.6% | 11.4% | 11.1% | 11.4% | 11.2% | 11.4% | 12.0% | 11.7% | 11.4% |

| South Carolina | 10.3% | 9.7% | 10.2% | 9.1% | 8.8% | 9.0% | 9.2% | 9.9% | 9.4% | 8.9% |

| South Dakota | 10.1% | 8.9% | 8.3% | 7.2% | 7.9% | 8.7% | 8.6% | 8.8% | 8.7% | 8.4% |

| Tennessee | 9.1% | 8.0% | 8.1% | 7.0% | 7.9% | 7.2% | 6.9% | 7.6% | 7.7% | 7.6% |

| Texas | 8.9% | 7.7% | 8.7% | 7.5% | 8.4% | 8.2% | 8.4% | 8.7% | 8.4% | 8.6% |

| Utah | 11.7% | 11.1% | 11.2% | 10.4% | 10.0% | 9.6% | 10.9% | 11.8% | 11.9% | 12.1% |

| Vermont | 13.0% | 10.8% | 11.1% | 10.1% | 10.8% | 11.7% | 12.0% | 12.8% | 13.4% | 13.6% |

| Virginia | 11.4% | 10.4% | 10.5% | 9.8% | 10.0% | 9.7% | 10.9% | 12.4% | 12.4% | 12.5% |

| Washington | 10.8% | 9.6% | 10.1% | 8.6% | 9.9% | 9.9% | 10.6% | 11.4% | 11.0% | 10.7% |

| West Virginia | 10.8% | 10.2% | 10.0% | 9.7% | 10.5% | 9.8% | 10.0% | 10.7% | 10.1% | 9.8% |

| Wisconsin | 14.1% | 12.2% | 12.3% | 11.5% | 11.7% | 10.5% | 10.8% | 11.6% | 11.3% | 10.9% |

| Wyoming | 9.0% | 7.9% | 6.9% | 6.7% | 8.3% | 8.8% | 7.9% | 9.3% | 8.3% | 7.5% |

Key Trends Over Time:

- Overall Stability: While there are year-to-year fluctuations, the national average tax burden has remained relatively consistent over several decades.

- State-Level Shifts: Individual states have experienced more dramatic changes. Alaska and North Dakota, for example, have seen significant decreases in tax burdens, largely due to resource revenue. Connecticut and Hawaii have seen notable increases over the long term.

- Pandemic Impact: The recent data shows a slight uptick in tax burdens across many states, influenced by economic changes related to the COVID-19 pandemic.

{kind=link}

Image: Line graph showing the trend of total state and local tax burden as a percentage of net product in the U.S. average from 1977 to 2022, illustrating the historical changes in tax burdens over time.

States with Dramatic Changes:

- Alaska: Alaska’s tax burden has plummeted dramatically since the late 1970s due to oil revenue, making it consistently the lowest-tax state.

- North Dakota: Similar to Alaska, North Dakota has also seen a significant decrease in tax burden over time.

- Connecticut and Hawaii: These states have experienced the largest increases in tax burdens since 1977, indicating shifts in their fiscal policies or economic structures.

These historical trends underscore that while national averages provide a broad overview, the tax landscape at the state level is dynamic and subject to significant changes driven by policy choices, economic conditions, and resource availability.

Conclusion: Making Informed Decisions Based on State Tax Comparisons

Comparing taxes between states is a complex but essential undertaking for individuals and businesses alike. By understanding the concept of tax burden, recognizing the nuances of tax incidence and tax exporting, and analyzing comprehensive data like that provided by the Tax Foundation, you can gain a much clearer picture of the true tax landscape across the United States.

Key takeaways for informed decision-making:

- Look Beyond Tax Rates: Focus on effective tax burdens, which provide a more accurate reflection of the total taxes borne by residents.

- Consider Tax Exporting: Understand how states may shift burdens to non-residents, influencing the apparent tax burden for residents.

- Recognize Limitations: Tax burden comparisons are valuable but don’t capture all aspects of government services or the full costs of taxation.

- Utilize Historical Data: Examine long-term trends to understand the stability and potential future trajectory of state tax burdens.

Ultimately, a thorough comparison of taxes between states should be a crucial component of any decision-making process involving relocation, business expansion, or simply understanding the fiscal environment in different parts of the country. By using the data and insights presented here, you can move beyond simplistic tax rate comparisons and make truly informed choices based on a comprehensive understanding of state and local tax burdens.

Stay informed on the tax policies impacting you. Subscribe to get insights from trusted experts delivered straight to your inbox.

Share this article