Individual income tax plays a pivotal role in state revenue systems across the United States, constituting a significant 38 percent of state tax collections. Unlike sales and excise taxes, which are often indirectly paid, individual income taxes require active filing and payment by individuals, making them a direct and visible aspect of state public policy.

Currently, 43 states impose individual income taxes, with the majority, 41 states, taxing wages and salary income. A few states take a different approach: New Hampshire focuses solely on dividend and interest income, while Washington taxes capital gains income. Notably, seven states forgo individual income tax altogether, relying on other forms of revenue.

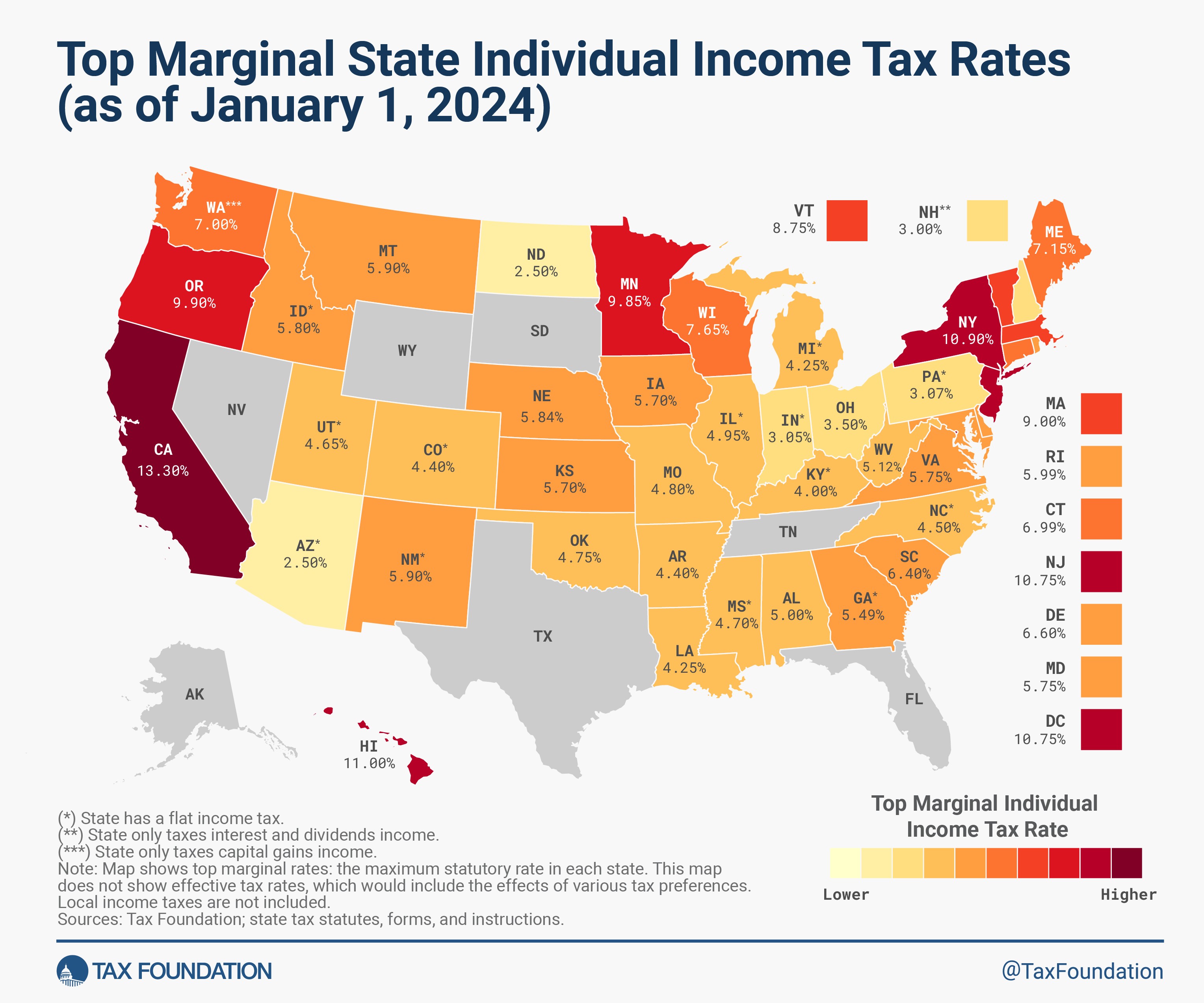

Among the states that tax wages, there are two primary structures: single-rate and graduated-rate systems. Twelve states employ a single-rate, or flat tax, structure, applying one uniform tax rate to all levels of taxable income. Conversely, 29 states, along with the District of Columbia, utilize graduated-rate income taxes. These systems feature multiple income brackets, each taxed at a progressively higher rate. The complexity of these graduated systems varies considerably. For instance, Montana operates with a simpler two-bracket system, while Hawaii presents a more intricate structure with 12 distinct tax brackets. The top marginal income tax rates across states range significantly, from a low of 2.5 percent in Arizona and North Dakota to a high of 13.3 percent in California. It’s important to note that California also levies an additional 1.1 percent payroll tax on wage income, pushing its effective top marginal rate to 14.4 percent.

2024 state income tax rates and states with no income tax

2024 state income tax rates and states with no income tax

In examining income tax brackets, some states cluster numerous brackets within a narrow income range. Virginia, for example, applies its highest tax bracket to taxable income as low as $17,000. In contrast, other states set much higher thresholds for their top rates. California, Massachusetts, New Jersey, New York, and the District of Columbia, for instance, only apply their top rates to income at or above $1 million (including surcharges like California’s “millionaire’s tax”).

To provide a clearer picture of the diverse income tax landscapes across the US, the following table categorizes states based on their income tax structures. You can easily compare states with no income tax, those with flat income taxes, and those with graduated-rate income taxes.

Income Tax Structures by State

2024 State Individual Income Tax Structures

| States with No Income Tax | States with a Flat Income Tax | States with a Graduated-Rate Income Tax |

|---|---|---|

| Alaska | Arizona | Alabama |

| Florida | Colorado | Arkansas |

| Nevada | Georgia | California |

| South Dakota | Idaho | Connecticut |

| Tennessee | Illinois | Delaware |

| Texas | Indiana | Hawaii |

| Wyoming | Kentucky | Iowa |

| Michigan | Kansas | |

| Mississippi | Louisiana | |

| New Hampshire* | Maine | |

| North Carolina | Maryland | |

| Pennsylvania | Massachusetts | |

| Utah | Minnesota | |

| Washington** | Missouri | |

| Montana | ||

| Nebraska | ||

| New Jersey | ||

| New Mexico | ||

| New York | ||

| North Dakota | ||

| Ohio | ||

| Oklahoma | ||

| Oregon | ||

| Rhode Island | ||

| South Carolina | ||

| Vermont | ||

| Virginia | ||

| West Virginia | ||

| Wisconsin | ||

| Washington, DC |

Notes: *Applies to interest and dividends income only. **Applies to capital gains income of high-earning individuals.

Sources: Tax Foundation; state tax statutes, forms, and instructions.

Beyond the basic structure and rates, states also differ significantly in other aspects of their income tax systems. Some states implement measures to mitigate the “marriage penalty” by doubling single-filer bracket widths for married filers. Inflation indexing is another area of divergence, with some states adjusting tax brackets, exemptions, and deductions annually to account for inflation, while many others do not. The approach to standard deductions and personal exemptions also varies widely. Some states directly link these to the federal tax code, while others establish their own state-specific amounts or offer none at all.

The Tax Cuts and Jobs Act (TCJA) brought significant changes to federal income tax rules, notably increasing the standard deduction and temporarily suspending personal exemptions. These federal changes have had ripple effects on state income tax systems, particularly for states that conform to the federal tax code. In response to the TCJA, many states have updated their conformity statutes, choosing to either adopt the federal changes, maintain their pre-TCJA deduction and exemption amounts, or create entirely separate state-level systems.

To provide a comprehensive comparison of state income taxes, the following tables present the most current data available on state individual income tax rates, brackets, standard deductions, and personal exemptions for both single and joint filers. Following these detailed tables, we outline notable changes to state individual income tax policies that took effect in 2024.

2024 State Income Tax Rates and Brackets

State Individual Income Tax Rates and Brackets, as of January 1, 2024

| State | Single Filer Rates | Single Filer Brackets | Married Filing Jointly Rates | Married Filing Jointly Brackets | Standard Deduction (Single) | Standard Deduction (Couple) | Personal Exemption (Single) | Personal Exemption (Couple) | Personal Exemption (Dependent) |

|---|---|---|---|---|---|---|---|---|---|

| Alabama (a, b, c) | 2.00% | > $0 | 2.00% | > $0 | $3,000 | $8,500 | $1,500 | $3,000 | $1,000 |

| Alabama | 4.00% | > $500 | 4.00% | > $1,000 | |||||

| Alabama | 5.00% | > $3,000 | 5.00% | > $6,000 | |||||

| Alaska | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Arizona (e, f, u) | 2.50% | > $0 | 2.50% | > $0 | $14,600 | $29,200 | n.a. | n.a. | $100 credit |

| Arkansas (g, h, bb, ll) | 2.00% | > $0 | 2.00% | > $0 | $2,340 | $4,680 | $29 credit | $58 credit | $29 credit |

| Arkansas | 4.00% | > $4,400 | 4.00% | > $4,400 | |||||

| Arkansas | 4.40% | > $8,800 | 4.40% | > $8,800 | |||||

| California (a, h, j, k, l, m, n, oo) | 1.00% | > $0 | 1.00% | > $0 | $5,363 | $10,726 | $144 credit | $288 credit | $446 credit |

| California | 2.00% | > $10,412 | 2.00% | > $20,824 | |||||

| California | 4.00% | > $24,684 | 4.00% | > $49,368 | |||||

| California | 6.00% | > $38,959 | 6.00% | > $77,918 | |||||

| California | 8.00% | > $54,081 | 8.00% | > $108,162 | |||||

| California | 9.30% | > $68,350 | 9.30% | > $136,700 | |||||

| California | 10.30% | > $349,137 | 10.30% | > $698,274 | |||||

| California | 11.30% | > $418,961 | 11.30% | > $837,922 | |||||

| California | 12.30% | > $698,271 | 12.30% | > $1,000,000 | |||||

| California | 13.30% | > $1,000,000 | 13.30% | > $1,396,542 | |||||

| Colorado (a, o) | 4.40% | > $0 | 4.40% | > $0 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| Connecticut ((i, p, q, r) | 2.00% | > $0 | 2.00% | > $0 | n.a. | n.a. | $15,000 | $24,000 | $0 |

| Connecticut | 4.50% | > $10,000 | 4.50% | > $20,000 | |||||

| Connecticut | 5.50% | > $50,000 | 5.50% | > $100,000 | |||||

| Connecticut | 6.00% | > $100,000 | 6.00% | > $200,000 | |||||

| Connecticut | 6.50% | > $200,000 | 6.50% | > $400,000 | |||||

| Connecticut | 6.90% | > $250,000 | 6.90% | > $500,000 | |||||

| Connecticut | 6.99% | > $500,000 | 6.99% | > $1,000,000 | |||||

| Delaware (a, h, m, s) | 2.20% | > $2,000 | 2.20% | > $2,000 | $3,250 | $6,500 | $110 credit | $220 credit | $110 credit |

| Delaware | 3.90% | > $5,000 | 3.90% | > $5,000 | |||||

| Delaware | 4.80% | > $10,000 | 4.80% | > $10,000 | |||||

| Delaware | 5.20% | > $20,000 | 5.20% | > $20,000 | |||||

| Delaware | 5.55% | > $25,000 | 5.55% | > $25,000 | |||||

| Delaware | 6.60% | > $60,000 | 6.60% | > $60,000 | |||||

| Florida | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Georgia | 5.49% | > $0 | 5.49% | > $0 | $12,000 | $24,000 | n.a. | n.a. | $3,000 |

| Hawaii (m, t) | 1.40% | > $0 | 1.40% | > $0 | $2,200 | $4,400 | $1,144 | $2,288 | $1,144 |

| Hawaii | 3.20% | > $2,400 | 3.20% | > $4,800 | |||||

| Hawaii | 5.50% | > $4,800 | 5.50% | > $9,600 | |||||

| Hawaii | 6.40% | > $9,600 | 6.40% | > $19,200 | |||||

| Hawaii | 6.80% | > $14,400 | 6.80% | > $28,800 | |||||

| Hawaii | 7.20% | > $19,200 | 7.20% | > $38,400 | |||||

| Hawaii | 7.60% | > $24,000 | 7.60% | > $48,000 | |||||

| Hawaii | 7.90% | > $36,000 | 7.90% | > $72,000 | |||||

| Hawaii | 8.25% | > $48,000 | 8.25% | > $96,000 | |||||

| Hawaii | 9.00% | > $150,000 | 9.00% | > $300,000 | |||||

| Hawaii | 10.00% | > $175,000 | 10.00% | > $350,000 | |||||

| Hawaii | 11.00% | > $200,000 | 11.00% | > $400,000 | |||||

| Idaho (m, u) | 5.8% | > $4,489 | 5.8% | > $8,978 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| Illinois (d, m, v) | 4.95% | > $0 | 4.95% | > $0 | n.a. | n.a. | $2,775 | $5,550 | $2,775 |

| Indiana (a, m, w) | 3.05% | > $0 | 3.05% | > $0 | n.a. | n.a. | $1,000 | $2,000 | $1,000 |

| Iowa (a, d, h) | 4.40% | > $0 | 4.40% | > $0 | n.a. | n.a. | $40 credit | $80 credit | $40 credit |

| Iowa | 4.82% | > $6,210 | 4.82% | > $12,420 | |||||

| Iowa | 5.70% | > $31,050 | 5.70% | > $62,100 | |||||

| Kansas (a, m) | 3.10% | > $0 | 3.10% | > $0 | $3,500 | $8,000 | $2,250 | $4,500 | $2,250 |

| Kansas | 5.25% | > $15,000 | 5.25% | > $30,000 | |||||

| Kansas | 5.70% | > $30,000 | 5.70% | > $60,000 | |||||

| Kentucky (a, d) | 4.00% | > $0 | 4.00% | > $0 | $3,160 | $6,320 | n.a. | n.a. | n.a. |

| Kentucky | |||||||||

| Louisiana (x) | 1.85% | > $0 | 1.85% | > $0 | n.a. | n.a. | $4,500 | $9,000 | $1,000 |

| Louisiana | 3.50% | > $12,500 | 3.50% | > $25,000 | |||||

| Louisiana | 4.25% | > $50,000 | 4.25% | > $100,000 | |||||

| Maine (u, y, bb) | 5.80% | > $0 | 5.80% | > $0 | $14,600 | $29,200 | $5,000 | $10,000 | $300 credit |

| Maine | 6.75% | > $26,050 | 6.75% | > $52,100 | |||||

| Maine | 7.15% | > $61,600 | 7.15% | > $123,250 | |||||

| Maryland (a, m, n, z, aa) | 2.00% | > $0 | 2.00% | > $0 | $2,550 | $5,150 | $3,200 | $6,400 | $3,200 |

| Maryland | 3.00% | > $1,000 | 3.00% | > $1,000 | |||||

| Maryland | 4.00% | > $2,000 | 4.00% | > $2,000 | |||||

| Maryland | 4.75% | > $3,000 | 4.75% | > $3,000 | |||||

| Maryland | 5.00% | > $100,000 | 5.00% | > $150,000 | |||||

| Maryland | 5.25% | > $125,000 | 5.25% | > $175,000 | |||||

| Maryland | 5.50% | > $150,000 | 5.50% | > $225,000 | |||||

| Maryland | 5.75% | > $250,000 | 5.75% | > $300,000 | |||||

| Massachusetts | 5.00% | > $0 | 5.00% | > $0 | n.a. | n.a. | $4,400 | $8,800 | $1,000 |

| Massachusetts | 9.00% | > $1,000,000 | 9.00% | > $1,000,000 | |||||

| Michigan (a, d, n) | 4.25% | > $0 | 4.25% | > $0 | n.a. | n.a. | $5,600 | $11,200 | $5,600 |

| Minnesota (d, bb, cc, pp) | 5.35% | > $0 | 5.35% | > $0 | $14,575 | $29,150 | n.a. | n.a. | $5,050 |

| Minnesota | 6.80% | > $31,690 | 6.80% | > $46,330 | |||||

| Minnesota | 7.85% | > $104,090 | 7.85% | > $184,040 | |||||

| Minnesota | 9.85% | > $193,240 | 9.85% | > $321,450 | |||||

| Mississippi | 4.70% | > $10,000 | 4.70% | > $10,000 | $2,300 | $4,600 | $6,000 | $12,000 | $1,500 |

| Missouri (a, b, j, m, u) | 2.00% | > $1,273 | 2.00% | > $1,207 | $14,600 | $29,200 | n.a | n.a | n.a |

| Missouri | 2.50% | > $2,546 | 2.50% | > $2,414 | |||||

| Missouri | 3.00% | > $3,819 | 3.00% | > $3,621 | |||||

| Missouri | 3.50% | > $5,092 | 3.50% | > $4,828 | |||||

| Missouri | 4.00% | > $6,365 | 4.00% | > $6,035 | |||||

| Missouri | 4.50% | > $7,638 | 4.50% | > $7,242 | |||||

| Missouri | 4.80% | > $8,911 | 4.80% | > $8,449 | |||||

| Montana (b, d, u, bb) | 4.70% | > $0 | 4.70% | > $0 | $14,600 | $29,200 | n.a | n.a | n.a |

| Montana | 5.90% | > $20,500 | 5.90% | > $41,000 | |||||

| Nebraska (d, h, m, bb) | 2.46% | > $0 | 2.46% | > $0 | $7,900 | $15,800 | $157 credit | $314 credit | $157 credit |

| Nebraska | 3.51% | > $3,700 | 3.51% | > $7,390 | |||||

| Nebraska | 5.01% | > $22,170 | 5.01% | > $44,350 | |||||

| Nebraska | 5.84% | > $35,730 | 5.84% | > $71,460 | |||||

| Nevada | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| New Hampshire (dd) | 3% on interest and dividends only | 3% on interest and dividends only | n.a | n.a | $2,400 | $4,800 | n.a. | n.a. | |

| New Jersey (a) | 1.400% | > $0 | 1.400% | > $0 | n.a. | n.a. | $1,000 | $2,000 | $1,500 |

| New Jersey | 1.750% | > $20,000 | 1.750% | > $20,000 | |||||

| New Jersey | 3.500% | > $35,000 | 2.450% | > $50,000 | |||||

| New Jersey | 5.525% | > $40,000 | 3.500% | > $70,000 | |||||

| New Jersey | 6.370% | > $75,000 | 5.525% | > $80,000 | |||||

| New Jersey | 8.970% | > $500,000 | 6.370% | > $150,000 | |||||

| New Jersey | 10.750% | > $1,000,000 | 8.970% | > $500,000 | |||||

| New Jersey | 10.750% | > $1,000,000 | |||||||

| New Mexico (m, u, kk) | 1.70% | > $0 | 1.70% | > $0 | $14,600 | $29,200 | n.a. | n.a. | $4,000 |

| New Mexico | 3.20% | > $5,500 | 3.20% | > $8,000 | |||||

| New Mexico | 4.70% | > $11,000 | 4.70% | > $16,000 | |||||

| New Mexico | 4.90% | > $16,000 | 4.90% | > $24,000 | |||||

| New Mexico | 5.90% | > $210,000 | 5.90% | > $315,000 | |||||

| New York (a, i) | 4.00% | > $0 | 4.00% | > $0 | $8,000 | $16,050 | n.a. | n.a. | $1,000 |

| New York | 4.50% | > $8,500 | 4.50% | > $17,150 | |||||

| New York | 5.25% | > $11,700 | 5.25% | > $23,600 | |||||

| New York | 5.50% | > $13,900 | 5.50% | > $27,900 | |||||

| New York | 6.00% | > $80,650 | 6.00% | > $161,550 | |||||

| New York | 6.85% | > $215,400 | 6.85% | > $323,200 | |||||

| New York | 9.65% | > $1,077,550 | 9.65% | > $2,155,350 | |||||

| New York | 10.30% | > $5,000,000 | 10.30% | > $5,000,000 | |||||

| New York | 10.90% | > $25,000,000 | 10.90% | > $25,000,000 | |||||

| North Carolina | 4.50% | > $0 | 4.50% | > $0 | $12,750 | $25,500 | n.a. | n.a. | n.a. |

| North Dakota (j, o, u) | 1.95% | > $44,725 | 1.95% | > $74,750 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| North Dakota | 2.50% | > $225,975 | 2.50% | > $275,100 | |||||

| Ohio (a, j, n, ee) | 2.750% | > $26,050 | 2.750% | > $26,050 | n.a. | n.a. | $2,400 | $4,800 | $2,500 |

| Ohio | 3.500% | > $92,150 | 3.500% | > $92,150 | |||||

| Oklahoma (m) | 0.25% | > $0 | 0.25% | > $0 | $6,350 | $12,700 | $1,000 | $2,000 | $1,000 |

| Oklahoma | 0.75% | > $1,000 | 0.75% | > $2,000 | |||||

| Oklahoma | 1.75% | > $2,500 | 1.75% | > $5,000 | |||||

| Oklahoma | 2.75% | > $3,750 | 2.75% | > $7,500 | |||||

| Oklahoma | 3.75% | > $4,900 | 3.75% | > $9,800 | |||||

| Oklahoma | 4.75% | > $7,200 | 4.75% | > $12,200 | |||||

| Oregon (a, b, d, h, m, bb, ff, oo) | 4.75% | > $0 | 4.75% | > $0 | $2,745 | $5,495 | $249 credit | $498 credit | $249 credit |

| Oregon | 6.75% | > $4,300 | 6.75% | > $8,600 | |||||

| Oregon | 8.75% | > $10,750 | 8.75% | > $21,500 | |||||

| Oregon | 9.90% | > $125,000 | 9.90% | > $250,000 | |||||

| Pennsylvania (a) | 3.07% | > $0 | 3.07% | > $0 | n.a. | n.a. | n.a. | n.a. | n.a. |

| Rhode Island (d, bb, gg) | 3.75% | > $0 | 3.75% | > $0 | $10,550 | $21,150 | $4,950 | $9,900 | $4,950 |

| Rhode Island | 4.75% | > $77,450 | 4.75% | > $77,450 | |||||

| Rhode Island | 5.99% | > $176,050 | 5.99% | > $176,050 | |||||

| South Carolina (d, o, u, bb) | 0.00% | > $0 | 0.00% | > $0 | $14,600 | $29,200 | n.a. | n.a. | $4,610 (o) |

| South Carolina | 3.00% | > $3,460 | 3.00% | > $3,460 | |||||

| South Carolina | 6.40% | > $17,330 | 6.40% | > $17,330 | |||||

| South Dakota | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Tennessee | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Texas | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Utah (d, h, hh) | 4.65% | > $0 | 4.65% | > $0 | $876 credit | $1,752 credit | n.a. | n.a. | $1,941 |

| Vermont (j, n, ii, nn) | 3.35% | > $0 | 3.35% | > $0 | $7,000 | $14,050 | $4,850 | $9,700 | $4,850 |

| Vermont | 6.60% | > $45,400 | 6.60% | > $75,850 | |||||

| Vermont | 7.60% | > $110,050 | 7.60% | > $183,400 | |||||

| Vermont | 8.75% | > $229,550 | 8.75% | > $279,450 | |||||

| Virginia (m, mm) | 2.00% | > $0 | 2.00% | > $0 | $8,000 | $16,000 | $930 | $1,860 | $930 |

| Virginia | 3.00% | > $3,000 | 3.00% | > $3,000 | |||||

| Virginia | 5.00% | > $5,000 | 5.00% | > $5,000 | |||||

| Virginia | 5.75% | > $17,000 | 5.75% | > $17,000 | |||||

| Washington | 7.0% on capital gains income only | 7.0% on capital gains income only | $250,000 | $250,000 | n.a. | n.a. | n.a. | n.a. | |

| West Virginia (a, m) | 2.36% | > $0 | 2.36% | > $0 | n.a. | n.a. | $2,000 | $4,000 | $2,000 |

| West Virginia | 3.15% | > $10,000 | 3.15% | > $10,000 | |||||

| West Virginia | 3.54% | > $25,000 | 3.54% | > $25,000 | |||||

| West Virginia | 4.72% | > $40,000 | 4.72% | > $40,000 | |||||

| West Virginia | 5.12% | > $60,000 | 5.12% | > $60,000 | |||||

| Wisconsin (d, m, bb, jj) | 3.50% | > $0 | 3.50% | > $0 | $13,230 | $24,490 | $700 | $1,400 | $700 |

| Wisconsin | 4.40% | > $14,320 | 4.40% | > $19,090 | |||||

| Wisconsin | 5.30% | > $28,640 | 5.30% | > $38,190 | |||||

| Wisconsin | 7.65% | > $315,310 | 7.65% | > $420,420 | |||||

| Wyoming | none | none | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Washington, DC (u) | 4.00% | > $0 | 4.00% | > $0 | $14,600 | $29,200 | n.a. | n.a. | n.a. |

| Washington, DC | 6.00% | > $10,000 | 6.00% | > $10,000 | |||||

| Washington, DC | 6.50% | > $40,000 | 6.50% | > $40,000 | |||||

| Washington, DC | 8.50% | > $60,000 | 8.50% | > $60,000 | |||||

| Washington, DC | 9.25% | > $250,000 | 9.25% | > $250,000 | |||||

| Washington, DC | 9.75% | > $500,000 | 9.75% | > $500,000 | |||||

| Washington, DC | 10.75% | > $1,000,000 | 10.75% | > $1,000,000 |

(a) Local income taxes are excluded. Eleven states have county- or city-level income taxes; the average rates expressed as a percentage of AGI within each jurisdiction are: AL–0.10%; DE–0.16%; IN–0.62%; IA–0.11%; KY–1.33%; MD–2.40%; MI–0.17%; MO–0.22%; NY–1.63%; OH–1.57%; PA–1.23%. In CA, CO, KS, NJ, OR, and WV some jurisdictions have payroll taxes, flat-rate wage taxes, or interest and dividend income taxes. See Jared Walczak, Janelle Fritts, and Maxwell James, “Local Income Taxes: A Primer,” Tax Foundation, February 23, 2023, https://taxfoundation.org/local-income-taxes-2023/. (b) These states allow some or all of federal income tax paid to be deducted from state taxable income. (c) For single taxpayers with AGI below $25,999, the standard deduction is $3,000. This standard deduction amount is reduced by $25 for every additional $500 of AGI, not to fall below $2,500. For Married Filing Joint (MFJ) taxpayers with AGI below $25,999, the standard deduction is $8,500. This standard deduction amount is reduced by $175 for every additional $500 of AGI, not to fall below $5,000. For all taxpayers with AGI of $50,000 or less and claiming a dependent, the dependent exemption is $1,000. This amount is reduced to $500 per dependent for taxpayers with AGI above $50,000 and equal to or less than $100,000. For taxpayers with more than $100,000 in AGI, the dependent exemption is $300 per dependent. (d) Standard deduction and/or personal exemption is adjusted annually for inflation. Inflation-adjusted amounts for tax year 2024 are shown. (e) Arizona’s standard deduction can be adjusted upward by an amount equal to 31 percent of the amount the taxpayer would have claimed in charitable deductions if the taxpayer had claimed itemized deductions. (f) In lieu of a dependent exemption, Arizona offers a dependent tax credit of $100 per dependent under the age of 17 and $25 per dependent age 17 and older. The credit begins to phase out for taxpayers with federal adjusted gross income (FAGI) above $200,000 (single filers) or $400,000 (MFJ). (g) Rates apply to individuals earning more than $87,000. A separate tax tables exist for individuals earning $87,000 or less, with rates of 2 percent on income greater than or equal to $5,300; 3 percent on income greater than or equal to $10,600; 3.4 percent on income greater than or equal to $15,100; and 4.4 percent on income greater than $25,000 but less than or equal to $87,000. (h) Standard deduction or personal exemption is structured as a tax credit. (i) Connecticut and New York have “tax benefit recapture,” by which many high-income taxpayers pay their top tax rate on all income, not just on amounts above the benefit threshold. (j) Bracket levels adjusted for inflation each year. Inflation-adjusted bracket widths for 2024 were not available as of publication, so table reflects 2023 inflation-adjusted bracket widths. (k) Exemption credits phase out for single taxpayers by $6 for each $2,500 of federal AGI above $237,035 and for MFJ filers by $12 for each $2,500 of federal AGI above $474,075. The credit cannot be reduced to below zero. (l) Rates include the additional mental health services tax at the rate of 1 percent on taxable income in excess of $1 million. Rates exclude a payroll tax of 1.1 percent to fund the state’s disability insurance program. As of 2024, there is no wage ceiling for this payroll tax, which means that the state’s top individual income tax rate on wage income becomes 14.4 percent. (m) State provides a state-defined personal exemption amount for each exemption available and/or deductible under the Internal Revenue Code. Under the Tax Cuts and Jobs Act, the personal exemption is set at $0 until 2026 but not eliminated. Because it is still available, these state-defined personal exemptions remain available in some states but are set to $0 in other states. (n) Standard deduction and/or personal exemption adjusted annually for inflation, but the 2024 inflation adjustment was not available at time of publication, so table reflects actual 2023 amount(s). (o) Colorado, Montana, New Mexico, North Dakota, and South Carolina include the federal standard deduction in their income starting point. (p) Connecticut has a complex set of phaseout provisions. For each single taxpayer whose Connecticut AGI exceeds $56,500, the amount of the taxpayer’s Connecticut taxable income to which the 2 percent tax rate applies shall be reduced by $1,000 for each $5,000, or fraction thereof, by which the taxpayer’s Connecticut AGI exceeds said amount. Any such amount will have a tax rate of 4.5 percent instead of 2 percent. Each single taxpayer whose Connecticut AGI exceeds $105,000 shall pay an amount equal to $25 for each $5,000, or fraction thereof, by which the taxpayer’s Connecticut AGI exceeds $105,000, up to a maximum payment of $250. Additionally, each single taxpayer whose Connecticut AGI exceeds $200,000 shall pay an amount equal to $90 for each $5,000, or fraction thereof, by which the taxpayer’s Connecticut AGI exceeds $200,000 but is less than $500,000, and by an additional $50 for each $5,000, or fraction thereof, by which the taxpayer’s AGI exceeds $500,000, up to a maximum payment of $3,150. For each MFJ taxpayer whose Connecticut AGI exceeds $100,500, the amount of the taxpayer’s Connecticut taxable income to which the 2 percent tax rate applies shall be reduced by $2,000 for each $5,000, or fraction thereof, by which the taxpayer’s Connecticut AGI exceeds said amount. Any such amount of Connecticut taxable income to which, as provided in the preceding sentence, the 2 percent tax rate does not apply shall be an amount to which the 4.5 percent tax rate shall apply. Each MFJ whose Connecticut AGI exceeds $210,000 shall pay an amount equal to $50 for each $10,000, or fraction thereof, by which the taxpayer’s Connecticut AGI exceeds $210,000, up to a maximum payment of $500. Additionally, each MFJ taxpayer whose Connecticut AGI exceeds $400,000 shall pay, in addition to the amount above, an amount equal to $180 for each $10,000, or fraction thereof, by which the taxpayer’s Connecticut AGI exceeds $400,000, up to a maximum of $5,400, and a further $100 for each $10,000, or fraction thereof, by which Connecticut AGI exceeds $1 million, up to a combined maximum payment of $6,300. (q) Connecticut taxpayers are also given personal tax credits (1-75%) based upon adjusted gross income. (r) Connecticut’s personal exemption phases out by $1,000 for each $1,000, or fraction thereof, by which a single filer’s Connecticut AGI exceeds $30,000 and a MFJ filer’s Connecticut AGI exceeds $48,000. (s) In addition to the personal income tax rates, Delaware imposes a tax on lump-sum distributions. (t) Additionally, Hawaii allows any taxpayer, other than a corporation, acting as a business entity in more than one state and required by law to file a return, to report and pay a tax of 0.5 percent of its annual gross sales (1) where the taxpayer’s only activities in Hawaii consist of sales, (2) when the taxpayer does not own or rent real estate or tangible personal property, and (3) when the taxpayer’s annual gross sales in or into Hawaii do not exceed $100,000. Haw. Rev. Stat. § 235-51 (2015). (u) Deduction and/or exemption tied to federal tax system. Federal deductions and exemptions are indexed for inflation, and where applicable, the tax year 2024 inflation-adjusted amounts are shown. (v) As of June 1, 2017, taxpayers cannot claim the personal exemption if their adjusted gross income exceeds $250,000 (single filers) or $500,000 (MFJ). (w) $1,000 is a base exemption. If dependents meet certain conditions, filers can take an additional $1,500 exemption for each. If a taxpayer is claiming a child as a dependent for the first taxable year in which the exemption is allowed, the taxpayer is now permitted to claim an amount of $3,000, instead of $1,500. (x) Standard deduction and personal exemptions are combined: $4,500 for single and married filing separately; $9,000 MFJ and head of household. (y) Maine’s personal exemption begins to phase out for taxpayers with income exceeding $305,150 (single filers) or $366,100 (MFJ). The standard deduction amounts for 2024 are phased out for taxpayers with Maine income over $97,150 (single filers) or $194,300 (MFJ). The dependent personal exemption is structured as a tax credit and begins to phase out for taxpayers with income exceeding $200,000 (head of household) or $400,000 (married filing jointly). (z) The standard deduction is 15 percent of income with a minimum of $1,700 and a cap of $2,550 for single filers and married filing separately filers. The standard deduction is a minimum of $3,450 and capped at $5,150 for MFJ filers, head of household filers, and qualifying surviving spouses. The minimum and maximum standard deduction amounts are adjusted annually for inflation. 2024 inflation-adjusted amounts were not announced as of publication, so 2023 inflation-adjusted amounts are shown. (aa) The exemption amount has the following phaseout schedule: If AGI is above $100,000 for single filers and above $150,000 for married filers, the $3,200 exemption begins to be phased out. If AGI is above $150,000 for single filers and above $200,000 for married filers, the exemption is phased out entirely. (bb) Bracket levels adjusted for inflation each year. Inflation-adjusted bracket levels for 2024 are shown. (cc) For taxpayers whose AGI exceeds $116,250 (married filing separately) or $232,500 (all other filers), Minnesota’s standard deduction is reduced by the lesser of 3 percent of the excess of the taxpayer’s federal AGI over the applicable amount or 80 percent of the standard deduction otherwise allowable. (dd) Applies to interest and dividend income only. (ee) Ohio’s personal exemption is $2,400 for an AGI of $40,000 or less, $2,150 if AGI is more than $40,000 but less than or equal to $80,000, and $1,900 if AGI is greater than $80,000. Ohio’s dependent exemption for children under the age of 18 is $2,500. (ff) The personal exemption credit is not allowed if federal AGI exceeds $100,000 for single filers or $200,000 for MFJ. (gg) The phaseout range for the standard deduction, personal exemption, and dependency exemption is $246,450 to $274,650. For taxpayers with modified Federal AGI exceeding $274,650, no standard deduction, personal exemption, or dependency exemption is available. (hh) The standard deduction is taken in the form of a nonrefundable credit of 6 percent of the federal standard or itemized deduction amount, excluding the deduction for state or local income tax. This credit phases out at 1.3 cents per dollar of AGI above $16,742 ($33,484 for MFJ). (ii) For taxpayers with federal AGI that exceeds $150,000, the taxpayer will pay the greater of state income tax or 3 percent of federal AGI. (jj) The standard deduction begins to phase out at $19,069 in income for single filers and $27,519 in income for joint filers. The standard deduction phases out to zero at $129,319 for single filers and $151,344 for joint filers. (kk) In lieu of the suspended personal exemption, New Mexico offers a deduction of $4,000 for all but one of a taxpayer’s dependents. (ll) Taxpayers with net income greater than or equal to $87,000 but not greater than $90,800 shall reduce the amount of tax due by deducting a bracket adjustment amount. The bracket adjustment amount starts at $380 for individuals with net income of $87,001 and decreases by $10 for every $100 in additional net income. (mm) The standard deduction for 2024 will be $8,500 for single taxpayers and $17,000 for MFJ taxpayers if certain revenue growth projections are met. (nn) Taxpayers also receive an additional deduction of $1,050 for each standard deduction box checked on federal Form 1040. (oo) California and Oregon do not fully index their top brackets. (pp) Minnesota imposes a surtax on individuals, estates, and trusts equal to 1% of net investment income over $1 million.

Notable 2024 State Individual Income Tax Changes

The trend of individual income tax rate reductions continued last year, with 26 states enacting rate cuts between 2021 and 2023. In contrast, only Massachusetts and the District of Columbia increased their top marginal tax rates during this period. While several changes were implemented retroactively to January 1, 2023, a number of significant changes took effect on January 1, 2024, or are scheduled for future dates, often with rates phasing down over time based on revenue benchmarks. Below are some key individual income tax changes certified for 2024:

Arkansas

Arkansas reduced its top individual income tax rate from 4.7 percent to 4.4 percent for tax years commencing on or after January 1, 2024. This adjustment, part of S.B. 8, impacts those earning over $8,801 (for taxpayers earning more than $87,000) and incomes between $24,300 and $87,000 (for taxpayers earning $87,000 or less).

Connecticut

Connecticut implemented income tax relief by lowering rates in the two lowest brackets. H.B. 6941 reduced the rates from 3 percent to 2 percent and from 5 percent to 4.5 percent, effective January 1, 2024. This change is targeted towards taxpayers with annual incomes below $150,000 (or $300,000 for joint filers).

Georgia

Georgia underwent a significant income tax overhaul on January 1, 2024, transitioning from a graduated income tax to a flat tax system. H.B. 1437 established a flat tax rate of 5.49 percent. Concurrently, the state increased its personal exemption to $12,000 for single taxpayers and $18,500 for married joint filers.

Indiana

Indiana accelerated its income tax reduction schedule through H.B. 1001. The individual income tax rate decreased from 3.15 percent in 2023 to 3.05 percent in 2024. Further reductions are planned, with rates set to reach 2.9 percent by 2027.

Iowa

Iowa’s tax reform (H.F. 2317) effective January 1, 2024, consolidated its income tax brackets from four to three. Consequently, the top income tax rate dropped from 6 percent to 5.7 percent as part of a broader plan to establish a flat 3.9 percent income tax by 2026.

Kentucky

Kentucky’s flat income tax rate saw a reduction from 4.5 percent to 4.0 percent in 2024, as mandated by H.B. 1. This rate cut was triggered by revenue conditions previously set by H.B. 8 in 2022.

Mississippi

Mississippi continued its phased income tax rate reduction under H.B. 531. Effective January 1, 2024, the rate decreased from 5 percent to 4.7 percent on taxable income exceeding $10,000. Further reductions are planned through 2026.

Missouri

Missouri’s top individual income tax rate was lowered from 4.95 percent to 4.8 percent, effective January 1, 2024. This change, in accordance with S.B. 3, was triggered by meeting revenue benchmarks in the previous fiscal year.

Montana

Montana streamlined its income tax system and reduced the number of tax brackets from seven to two, as per S.B. 121. Starting January 1, 2024, the top tax rate is 5.9 percent. Montana also shifted to using federal taxable income as the base for state income tax calculations.

Nebraska

Nebraska implemented a significant income tax rate cut, reducing the top rate from 6.64 percent in 2023 to 5.84 percent in 2024. L.B. 754 outlines a plan for further gradual reductions to reach a top rate of 3.99 percent by 2027.

New Hampshire

New Hampshire is proceeding with the phase-out of its tax on interest and dividends. H.B. 2 reduced the rate from 4 percent to 3 percent in 2024, with complete repeal now scheduled for 2025, two years ahead of the original schedule.

North Carolina

North Carolina accelerated its income tax rate reduction timeline under H.B. 259. The flat income tax rate decreased from 4.75 percent to 4.5 percent, effective January 1, 2024, with a target rate of 3.99 percent by 2026.

Ohio

Ohio continued its trend of income tax simplification and reduction with H.B. 33. The number of income tax brackets was reduced from three to two, and the top rate decreased from 3.75 percent to 3.5 percent.

South Carolina

South Carolina’s top income tax rate was reduced from 6.5 percent to 6.4 percent, effective January 1, 2024, according to S.B. 1087. Further reductions to 6 percent are planned, contingent on meeting general fund revenue targets. Current projections suggest a further reduction to 6.3 percent is anticipated, pending confirmation from the state’s Department of Revenue.

Historical State Individual Income Tax Rates

Download Data (2015-2024)