Are Comparative Statements Examples Of Horizontal Or Vertical Analysis? Comparative statements, crucial for financial evaluations, utilize both horizontal and vertical analysis techniques, each offering unique insights into a company’s performance and financial health; at COMPARE.EDU.VN, we offer the insights you need. Horizontal analysis examines trends over time, while vertical analysis assesses the proportional relationship of items within a single financial statement. These methods, invaluable for investors, analysts, and management, aid in identifying strengths, weaknesses, and areas for improvement using methods of financial statement analysis and trend analysis.

1. Understanding Comparative Statements in Financial Analysis

Comparative statements are essential tools in financial analysis, providing a structured way to examine a company’s financial performance over different periods or in relation to a base figure. These statements typically present data from multiple periods side-by-side, allowing for easy comparison and identification of trends. The core purpose of comparative statements is to highlight changes and patterns that might not be immediately apparent when looking at a single financial statement in isolation. Comparative statements often include balance sheets, income statements, and cash flow statements, each offering a different perspective on the company’s financial health and operational efficiency. The insights gained from comparative statements are invaluable for investors, analysts, and management alike, aiding in decision-making and strategic planning.

2. The Essence of Horizontal Analysis

Horizontal analysis, also known as trend analysis, is a technique used to evaluate financial statement data over a period of time. It involves comparing line items from one period to the next to calculate the change in dollar amount and percentage. This type of analysis is particularly useful for identifying trends and patterns in a company’s performance. The basic principle of horizontal analysis is to establish a base year and then compare subsequent years to that base. The changes are expressed both in absolute terms (dollar amounts) and as a percentage of the base year. For example, if a company’s revenue increased from $1 million in 2022 to $1.2 million in 2023, the horizontal analysis would show a $200,000 increase, or a 20% growth rate. By examining these trends, analysts can gain insights into a company’s growth trajectory, identify potential problem areas, and make informed predictions about future performance.

2.1. How Horizontal Analysis Works

To conduct a horizontal analysis, one must first select a base period. This is typically the earliest period in the comparative statement. Subsequent periods are then compared to this base period to determine the change in each line item. The formula for calculating the percentage change in horizontal analysis is:

Percentage Change = [(Current Period Amount – Base Period Amount) / Base Period Amount] * 100

This calculation provides the percentage by which a line item has increased or decreased relative to the base period. The results of this analysis are then presented in a comparative format, allowing for easy identification of trends and anomalies. For example, a consistent increase in revenue year over year might indicate strong growth, while a sudden drop in net income could signal underlying issues that require further investigation.

2.2. Advantages and Limitations of Horizontal Analysis

Horizontal analysis offers several advantages. It provides a clear view of trends and patterns over time, which can be invaluable for forecasting and strategic planning. It is relatively simple to perform and understand, making it accessible to a wide range of users. It can also help identify areas that require further investigation.

However, horizontal analysis also has its limitations. It primarily focuses on historical data, which may not always be indicative of future performance. It does not account for external factors such as economic conditions or industry trends, which can significantly impact a company’s financial results. Additionally, horizontal analysis may not be useful for comparing companies of different sizes or in different industries, as the absolute values and percentage changes can be misleading in such cases.

3. The Foundation of Vertical Analysis

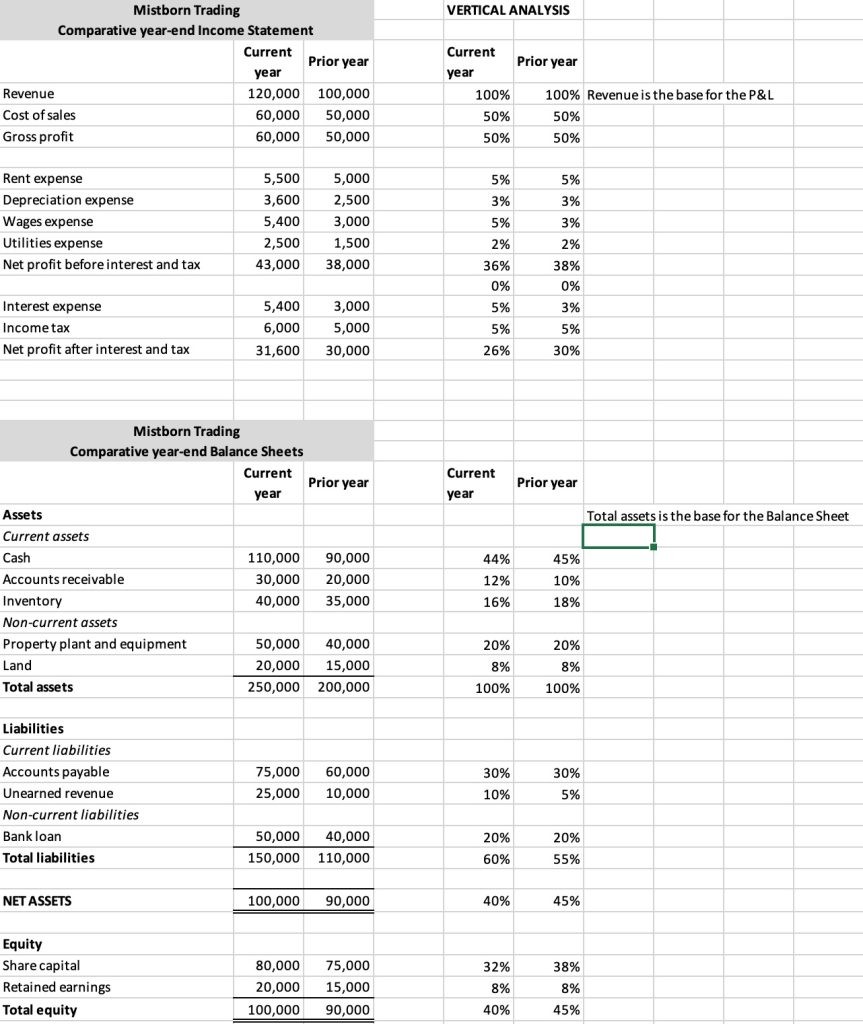

Vertical analysis, also known as common-size analysis, is a method of financial statement analysis that expresses each line item as a percentage of a base figure within the same period. This technique is particularly useful for comparing companies of different sizes or for analyzing trends within a single company over time. In vertical analysis, the base figure is typically total assets for the balance sheet and net sales for the income statement. For example, on a balance sheet, cash might be expressed as 10% of total assets, while on an income statement, cost of goods sold might be expressed as 60% of net sales. By converting financial statement data into percentages, vertical analysis allows for a standardized comparison that eliminates the impact of size differences. This makes it easier to identify key drivers of performance and to benchmark against industry peers.

3.1. How Vertical Analysis Works

To perform vertical analysis, one must first identify the base figure for each financial statement. As mentioned earlier, this is typically total assets for the balance sheet and net sales for the income statement. Each line item is then divided by the base figure and multiplied by 100 to express it as a percentage. The formula for calculating the percentage in vertical analysis is:

Percentage = (Line Item Amount / Base Figure Amount) * 100

This calculation provides the percentage that each line item represents of the base figure. The results are then presented in a common-size format, allowing for easy comparison of the relative importance of each item. For example, if a company’s advertising expense is 5% of net sales, it means that for every dollar of sales, the company spends 5 cents on advertising. By comparing these percentages over time or against industry averages, analysts can gain insights into a company’s cost structure, profitability, and efficiency.

3.2. Advantages and Limitations of Vertical Analysis

Vertical analysis offers several advantages. It allows for easy comparison of companies of different sizes, as the data is standardized in percentage terms. It provides insights into the relative importance of each line item, helping to identify key drivers of performance. It can also be used to track changes in a company’s cost structure or profitability over time.

However, vertical analysis also has its limitations. It does not provide information about the absolute dollar amounts, which can be important for understanding the overall scale of a company’s operations. It may not be useful for analyzing trends over time, as the percentages can fluctuate due to changes in the base figure. Additionally, vertical analysis should be used in conjunction with other analytical techniques to provide a comprehensive view of a company’s financial performance.

4. Comparative Statements: A Hybrid Approach

Comparative statements are not strictly horizontal or vertical analysis but incorporate elements of both to provide a more comprehensive view of a company’s financial performance. They present financial data from multiple periods side-by-side, allowing for easy comparison of line items over time (horizontal analysis). Additionally, they often include common-size percentages, which express each line item as a percentage of a base figure within the same period (vertical analysis). This hybrid approach allows users to analyze both the trends in absolute dollar amounts and the relative importance of each line item. For example, a comparative income statement might show the year-over-year growth in revenue (horizontal analysis) as well as the percentage of revenue that is consumed by cost of goods sold (vertical analysis). By combining these two techniques, comparative statements offer a more nuanced and informative analysis of a company’s financial performance.

5. Horizontal vs. Vertical Analysis: Key Differences

While both horizontal and vertical analysis are valuable tools for financial statement analysis, they differ in their approach and the types of insights they provide. Horizontal analysis focuses on trends over time, comparing line items from one period to the next to identify changes and patterns. It is primarily concerned with the direction and magnitude of these changes, expressed both in dollar amounts and percentages.

Vertical analysis, on the other hand, focuses on the relationship between line items within a single period, expressing each item as a percentage of a base figure. It is primarily concerned with the relative importance of each item and how it contributes to the overall financial picture.

| Feature | Horizontal Analysis | Vertical Analysis |

|---|---|---|

| Focus | Trends over time | Relationship between line items within a single period |

| Comparison | Line items from one period to the next | Each line item as a percentage of a base figure |

| Base Figure | Previous period’s amount | Total assets (balance sheet), net sales (income statement) |

| Primary Insight | Changes and patterns in financial performance over time | Relative importance of each line item |

6. Advantages of Using Both Analyses

Using both horizontal and vertical analysis in conjunction can provide a more complete and insightful view of a company’s financial performance. Horizontal analysis can help identify trends and patterns that might not be apparent when looking at a single period, while vertical analysis can provide insights into the relative importance of each line item and how it contributes to the overall financial picture. By combining these two techniques, analysts can gain a deeper understanding of a company’s strengths, weaknesses, and areas for improvement. For example, a company might experience strong revenue growth (horizontal analysis), but vertical analysis might reveal that its cost of goods sold is also increasing as a percentage of revenue, indicating a potential issue with profitability.

7. Practical Examples of Comparative Statement Analysis

To illustrate the practical application of comparative statement analysis, let’s consider a hypothetical company, “Tech Solutions Inc.” We will analyze its comparative income statement and balance sheet using both horizontal and vertical analysis techniques.

7.1. Comparative Income Statement Analysis

The following table presents Tech Solutions Inc.’s comparative income statement for the years 2022 and 2023:

| Line Item | 2022 | 2023 | Change ($) | Change (%) |

|---|---|---|---|---|

| Net Sales | $1,000,000 | $1,200,000 | $200,000 | 20% |

| Cost of Goods Sold | $600,000 | $700,000 | $100,000 | 16.67% |

| Gross Profit | $400,000 | $500,000 | $100,000 | 25% |

| Operating Expenses | $200,000 | $250,000 | $50,000 | 25% |

| Net Income | $200,000 | $250,000 | $50,000 | 25% |

Horizontal Analysis:

The horizontal analysis reveals that Tech Solutions Inc. experienced significant growth in 2023. Net sales increased by 20%, gross profit increased by 25%, and net income increased by 25%. This indicates strong overall performance.

Vertical Analysis:

To perform vertical analysis, we will express each line item as a percentage of net sales:

| Line Item | 2022 (%) | 2023 (%) |

|---|---|---|

| Net Sales | 100% | 100% |

| Cost of Goods Sold | 60% | 58.33% |

| Gross Profit | 40% | 41.67% |

| Operating Expenses | 20% | 20.83% |

| Net Income | 20% | 20.83% |

The vertical analysis shows that the cost of goods sold decreased as a percentage of net sales, while gross profit and net income increased. This indicates improved profitability.

7.2. Comparative Balance Sheet Analysis

The following table presents Tech Solutions Inc.’s comparative balance sheet for the years 2022 and 2023:

| Line Item | 2022 | 2023 | Change ($) | Change (%) |

|---|---|---|---|---|

| Cash | $100,000 | $120,000 | $20,000 | 20% |

| Accounts Receivable | $150,000 | $180,000 | $30,000 | 20% |

| Total Assets | $500,000 | $600,000 | $100,000 | 20% |

| Accounts Payable | $50,000 | $60,000 | $10,000 | 20% |

| Total Liabilities | $150,000 | $180,000 | $30,000 | 20% |

| Equity | $350,000 | $420,000 | $70,000 | 20% |

| Total Liabilities & Equity | $500,000 | $600,000 | $100,000 | 20% |

Horizontal Analysis:

The horizontal analysis reveals that Tech Solutions Inc. experienced a 20% increase in all major balance sheet items, including cash, accounts receivable, total assets, accounts payable, total liabilities, and equity. This indicates consistent growth across the board.

Vertical Analysis:

To perform vertical analysis, we will express each asset line item as a percentage of total assets and each liability and equity line item as a percentage of total liabilities and equity:

| Line Item | 2022 (%) | 2023 (%) |

|---|---|---|

| Cash | 20% | 20% |

| Accounts Receivable | 30% | 30% |

| Total Assets | 100% | 100% |

| Accounts Payable | 10% | 10% |

| Total Liabilities | 30% | 30% |

| Equity | 70% | 70% |

| Total Liabilities & Equity | 100% | 100% |

The vertical analysis shows that the composition of assets, liabilities, and equity remained relatively stable from 2022 to 2023. This indicates that the company’s financial structure is consistent.

8. The Role of COMPARE.EDU.VN in Comparative Analysis

COMPARE.EDU.VN plays a crucial role in facilitating comparative analysis by providing users with the tools and resources they need to make informed decisions. Whether you’re comparing different products, services, or educational programs, COMPARE.EDU.VN offers a comprehensive platform for evaluating your options. Our website provides detailed comparisons, side-by-side analyses, and user reviews to help you weigh the pros and cons of each choice. With COMPARE.EDU.VN, you can easily identify the key differences between alternatives and select the one that best meets your needs and preferences. Our goal is to empower you with the knowledge and insights you need to make confident decisions, saving you time and effort in the process.

9. Choosing the Right Analysis for Your Needs

The choice between horizontal and vertical analysis depends on the specific goals of the analysis and the type of insights you are seeking. If you are interested in identifying trends and patterns over time, horizontal analysis is the more appropriate choice. If you are interested in understanding the relative importance of each line item and how it contributes to the overall financial picture, vertical analysis is the better option. In many cases, using both techniques in conjunction can provide a more complete and insightful view of a company’s financial performance.

10. Common Mistakes to Avoid in Comparative Analysis

When conducting comparative analysis, it is important to avoid several common mistakes that can lead to inaccurate or misleading conclusions. One common mistake is failing to adjust for inflation or changes in accounting standards. Inflation can distort the comparison of financial data over time, while changes in accounting standards can make it difficult to compare financial statements prepared under different sets of rules.

Another common mistake is focusing solely on the numbers without considering the underlying business context. Financial analysis should always be accompanied by a thorough understanding of the company’s industry, competitive environment, and strategic objectives. Additionally, it is important to avoid making overly simplistic or generalized conclusions based on a limited set of data. Comparative analysis should be a comprehensive and nuanced process that takes into account all relevant factors.

11. Advanced Techniques in Comparative Analysis

In addition to horizontal and vertical analysis, there are several advanced techniques that can be used to enhance the insights gained from comparative statements. These include ratio analysis, regression analysis, and trend forecasting.

Ratio analysis involves calculating and comparing various financial ratios, such as profitability ratios, liquidity ratios, and solvency ratios. These ratios can provide insights into a company’s financial health and performance that are not readily apparent from the financial statements themselves.

Regression analysis is a statistical technique that can be used to identify relationships between different financial variables. For example, regression analysis might be used to determine the relationship between sales and advertising expense.

Trend forecasting involves using historical data to predict future financial performance. This can be done using a variety of statistical techniques, such as time series analysis and exponential smoothing.

12. Industry-Specific Considerations for Comparative Analysis

The specific techniques and metrics used in comparative analysis may vary depending on the industry in which a company operates. For example, in the retail industry, key metrics might include same-store sales growth and inventory turnover, while in the banking industry, key metrics might include net interest margin and loan loss reserves. It is important to understand the unique characteristics of each industry and to tailor the analysis accordingly. Additionally, it is important to benchmark a company’s performance against its industry peers to determine how it stacks up against the competition.

13. Best Practices for Presenting Comparative Analysis Results

When presenting the results of comparative analysis, it is important to follow several best practices to ensure that the information is clear, concise, and easy to understand. The results should be presented in a visually appealing format, using charts, graphs, and tables to illustrate key trends and patterns. The analysis should be accompanied by a clear and concise narrative that explains the key findings and their implications. Additionally, it is important to provide context and background information to help the audience understand the analysis. Finally, the analysis should be objective and unbiased, presenting both the positive and negative aspects of a company’s financial performance.

14. Case Studies: Successful Applications of Comparative Analysis

To further illustrate the power and versatility of comparative analysis, let’s examine a few case studies of companies that have successfully used this technique to improve their financial performance.

14.1. Case Study 1: Retail Chain Improves Profitability

A retail chain used comparative analysis to identify and address a decline in profitability. By analyzing its comparative income statements, the company discovered that its cost of goods sold was increasing as a percentage of revenue, while its gross profit margin was declining. Further investigation revealed that the company was experiencing higher inventory costs and lower sales prices due to increased competition. To address these issues, the company implemented a new inventory management system and launched a series of promotional campaigns to boost sales. As a result, the company was able to reduce its cost of goods sold, increase its gross profit margin, and improve its overall profitability.

14.2. Case Study 2: Manufacturing Company Optimizes Asset Utilization

A manufacturing company used comparative analysis to optimize its asset utilization. By analyzing its comparative balance sheets, the company discovered that its accounts receivable balance was increasing as a percentage of total assets, while its cash balance was declining. Further investigation revealed that the company was experiencing delays in collecting payments from its customers. To address this issue, the company implemented a new credit and collection policy and offered discounts to customers who paid their invoices early. As a result, the company was able to reduce its accounts receivable balance, increase its cash balance, and improve its overall asset utilization.

15. The Future of Comparative Analysis

The field of comparative analysis is constantly evolving, driven by advances in technology and changes in the business environment. One key trend is the increasing use of data analytics and artificial intelligence to automate and enhance the analysis process. These technologies can be used to identify patterns and anomalies in financial data that might not be apparent to human analysts, and to generate more accurate and reliable forecasts of future financial performance. Another trend is the increasing focus on non-financial metrics, such as environmental, social, and governance (ESG) factors. These metrics are becoming increasingly important to investors and other stakeholders, and comparative analysis is being used to assess and compare companies’ performance in these areas.

16. FAQs About Comparative Statements

1. What is the primary purpose of comparative statements?

The primary purpose of comparative statements is to provide a structured way to examine a company’s financial performance over different periods or in relation to a base figure.

2. What is the difference between horizontal and vertical analysis?

Horizontal analysis focuses on trends over time, while vertical analysis focuses on the relationship between line items within a single period.

3. What is the base figure typically used in vertical analysis for the balance sheet?

The base figure typically used in vertical analysis for the balance sheet is total assets.

4. What is the base figure typically used in vertical analysis for the income statement?

The base figure typically used in vertical analysis for the income statement is net sales.

5. What are some common mistakes to avoid in comparative analysis?

Some common mistakes to avoid in comparative analysis include failing to adjust for inflation or changes in accounting standards, focusing solely on the numbers without considering the underlying business context, and making overly simplistic or generalized conclusions based on a limited set of data.

6. What are some advanced techniques that can be used to enhance the insights gained from comparative statements?

Some advanced techniques that can be used to enhance the insights gained from comparative statements include ratio analysis, regression analysis, and trend forecasting.

7. How does the choice between horizontal and vertical analysis depend on the specific goals of the analysis?

If you are interested in identifying trends and patterns over time, horizontal analysis is the more appropriate choice. If you are interested in understanding the relative importance of each line item and how it contributes to the overall financial picture, vertical analysis is the better option.

8. What are some industry-specific considerations for comparative analysis?

The specific techniques and metrics used in comparative analysis may vary depending on the industry in which a company operates.

9. What are some best practices for presenting comparative analysis results?

Some best practices for presenting comparative analysis results include presenting the results in a visually appealing format, using charts, graphs, and tables to illustrate key trends and patterns, and accompanying the analysis with a clear and concise narrative that explains the key findings and their implications.

10. How is COMPARE.EDU.VN useful in performing comparative analysis?

COMPARE.EDU.VN offers a comprehensive platform for evaluating your options, providing detailed comparisons, side-by-side analyses, and user reviews to help you weigh the pros and cons of each choice.

17. Conclusion: Mastering Comparative Analysis for Financial Success

In conclusion, comparative statements are invaluable tools for financial analysis, offering a comprehensive view of a company’s performance and financial health. By understanding the nuances of horizontal and vertical analysis, and by avoiding common mistakes, you can unlock the full potential of these techniques and make more informed decisions. Whether you are an investor, analyst, or business owner, mastering comparative analysis is essential for achieving financial success. Visit COMPARE.EDU.VN at 333 Comparison Plaza, Choice City, CA 90210, United States, or contact us via Whatsapp at +1 (626) 555-9090 to discover how we can help you make better comparisons and smarter choices. Let compare.edu.vn be your guide to informed decision-making.