Vertical analysis, as compared to a horizontal analysis, offers unique insights into a company’s financial performance. COMPARE.EDU.VN is dedicated to providing clear, objective comparisons of financial analysis techniques. Understanding both vertical and horizontal analysis empowers informed decision-making. Unlock superior financial insights with comparative methods and financial statement analysis on COMPARE.EDU.VN.

1. Understanding Financial Statement Analysis

Financial statement analysis is a critical process used to evaluate a company’s financial performance and health. It involves scrutinizing a company’s financial statements, including the balance sheet, income statement, and cash flow statement, to gain insights into its profitability, liquidity, solvency, and efficiency. There are several methods of financial statement analysis, each providing a unique perspective. Two prominent methods are vertical analysis and horizontal analysis. These techniques help stakeholders, such as investors, creditors, and management, make informed decisions. Vertical and horizontal analyses enable a comprehensive understanding of financial data by dissecting and comparing financial figures.

2. What is Vertical Analysis?

Vertical analysis, also known as common-size analysis, is a method of financial statement analysis that examines the proportional relationship of items within a single financial statement. It involves expressing each line item in the statement as a percentage of a base figure. For the income statement, the base figure is typically revenue or sales, while for the balance sheet, it is usually total assets or total liabilities and equity. This approach facilitates comparison of different companies, regardless of their size, and helps identify significant relationships and trends within a company’s financial structure.

2.1. Key Components of Vertical Analysis

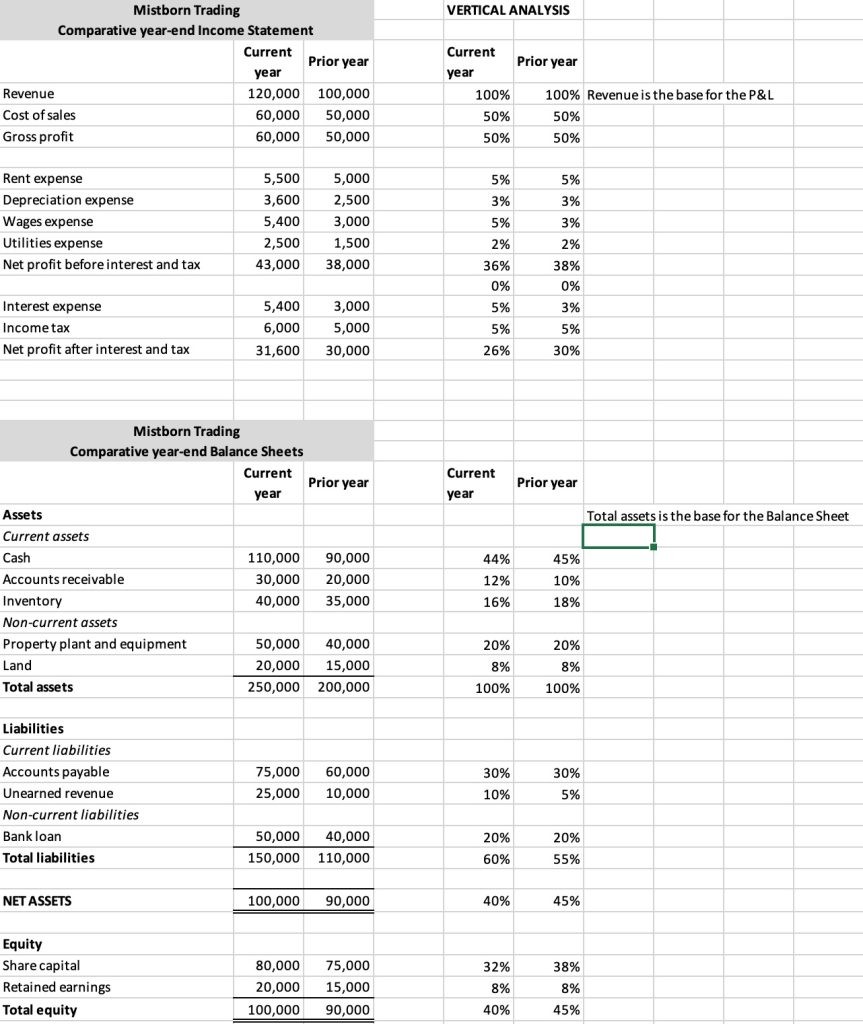

Vertical analysis transforms raw financial data into comparable percentages. On an income statement, each expense is expressed as a percentage of revenue, providing insights into cost control and profitability.

Income statement showing revenue and expenses as percentages of total revenue.

Income statement showing revenue and expenses as percentages of total revenue.

2.2. Advantages of Vertical Analysis

One significant advantage of vertical analysis is its ability to standardize financial data. By converting figures into percentages, it allows for easy comparison between companies of different sizes. It also helps in identifying potential areas of concern, such as rising costs or decreasing profitability.

2.3. Limitations of Vertical Analysis

Despite its benefits, vertical analysis has limitations. It primarily focuses on internal relationships within a single period and does not provide insights into trends over time. Additionally, it can be influenced by accounting policies and may not capture external factors affecting a company’s performance.

3. What is Horizontal Analysis?

Horizontal analysis, also known as trend analysis, is a technique used to evaluate changes in financial statement items over a period of time. It involves comparing financial data across multiple periods to identify trends and patterns. This analysis helps in understanding the direction of a company’s financial performance and predicting future outcomes. Horizontal analysis provides insights into growth rates, stability, and potential areas of concern.

3.1. Key Components of Horizontal Analysis

Horizontal analysis calculates the percentage change in each line item from one period to the next. For example, it compares current year revenue to the previous year’s revenue to determine the growth rate.

3.2. Advantages of Horizontal Analysis

Horizontal analysis is valuable for identifying trends and changes over time. It helps in assessing the sustainability of a company’s performance and provides a basis for forecasting future results. By tracking changes in key financial metrics, stakeholders can make informed decisions about investments and strategic planning.

3.3. Limitations of Horizontal Analysis

Horizontal analysis can be misleading if significant events or changes in accounting policies occur during the period under review. It may also fail to capture the underlying drivers of financial performance and requires additional analysis to understand the reasons behind the observed trends.

4. Vertical Analysis as Compared to Horizontal Analysis: Key Differences

While both vertical and horizontal analysis are valuable tools in financial statement analysis, they serve different purposes and provide distinct insights. Understanding their key differences is essential for a comprehensive financial evaluation.

4.1. Focus and Perspective

Vertical analysis focuses on the relationship between items within a single financial statement, providing a snapshot of a company’s financial structure at a specific point in time. Horizontal analysis, on the other hand, focuses on changes in financial statement items over a period of time, providing a dynamic view of a company’s performance trends.

4.2. Timeframe

Vertical analysis is conducted for a single period, such as a year or a quarter, while horizontal analysis requires data from multiple periods to identify trends and patterns.

4.3. Base Figure

In vertical analysis, each item is expressed as a percentage of a base figure within the same statement, such as revenue for the income statement or total assets for the balance sheet. Horizontal analysis does not use a base figure but calculates the percentage change from one period to the next.

4.4. Comparative Analysis

Vertical analysis facilitates comparison between companies of different sizes by standardizing financial data. Horizontal analysis helps in comparing a company’s performance over time and identifying areas of improvement or concern.

4.5. Insights Provided

Vertical analysis provides insights into a company’s financial structure and the relative importance of each item within a statement. Horizontal analysis provides insights into a company’s growth trends and the sustainability of its financial performance.

5. Detailed Comparison Table

To further illustrate the differences between vertical and horizontal analysis, consider the following detailed comparison table:

| Feature | Vertical Analysis | Horizontal Analysis |

|---|---|---|

| Focus | Relationship within a single statement | Changes over time across multiple statements |

| Timeframe | Single period (e.g., year or quarter) | Multiple periods (e.g., years or quarters) |

| Base Figure | Uses a base figure (e.g., revenue or total assets) | Does not use a base figure |

| Comparative Analysis | Compares companies of different sizes | Compares a company’s performance over time |

| Insights Provided | Financial structure, item importance | Growth trends, performance sustainability |

| Calculation Method | Percentage of a base figure | Percentage change from one period to the next |

| Statement Focus | Income Statement, Balance Sheet | Income Statement, Balance Sheet, Cash Flow Statement |

| Primary Users | Investors, creditors, management | Analysts, management, strategic planners |

| Objective | Assess financial position at a point in time | Evaluate performance trends over time |

| Advantage | Standardizes data for easy comparison | Identifies patterns and changes in financial health |

| Limitation | Lacks insights into trends over time | May be misleading due to external factors |

| Decision Making | Resource allocation, cost control | Strategic planning, investment decisions |

| Additional Information | Helps in understanding internal relationships | Aids in forecasting future financial outcomes |

| Common Use | Benchmarking, internal assessments | Performance evaluation, trend analysis |

| Example (Income) | COGS as % of Revenue | Revenue growth rate from Year 1 to Year 2 |

| Example (Balance) | Cash as % of Total Assets | Change in total debt from Year 1 to Year 2 |

6. How to Perform Vertical Analysis

Performing vertical analysis involves a few straightforward steps. First, select the financial statement you want to analyze, such as the income statement or balance sheet. Next, identify the base figure, which is typically revenue for the income statement and total assets or total liabilities and equity for the balance sheet. Then, divide each line item by the base figure and multiply by 100 to express it as a percentage. Finally, analyze the percentages to identify significant relationships and trends.

6.1. Steps for Income Statement Analysis

- Select the income statement for the period you want to analyze.

- Identify revenue as the base figure.

- Divide each line item (e.g., cost of goods sold, operating expenses) by revenue.

- Multiply the result by 100 to express it as a percentage.

- Analyze the percentages to identify significant cost drivers and profit margins.

6.2. Steps for Balance Sheet Analysis

- Select the balance sheet for the period you want to analyze.

- Identify total assets or total liabilities and equity as the base figure.

- Divide each line item (e.g., cash, accounts receivable, accounts payable) by the base figure.

- Multiply the result by 100 to express it as a percentage.

- Analyze the percentages to understand the composition of assets, liabilities, and equity.

6.3. Example of Vertical Analysis Calculation

Consider a company with the following income statement:

- Revenue: $1,000,000

- Cost of Goods Sold (COGS): $600,000

- Operating Expenses: $200,000

- Net Income: $200,000

To perform vertical analysis:

- COGS as a percentage of Revenue: ($600,000 / $1,000,000) * 100 = 60%

- Operating Expenses as a percentage of Revenue: ($200,000 / $1,000,000) * 100 = 20%

- Net Income as a percentage of Revenue: ($200,000 / $1,000,000) * 100 = 20%

This analysis shows that COGS accounts for 60% of revenue, operating expenses account for 20%, and net income accounts for 20%.

7. How to Perform Horizontal Analysis

Performing horizontal analysis involves comparing financial data across multiple periods. First, select the financial statements for the periods you want to compare. Next, calculate the change in each line item from one period to the next. Then, divide the change by the base period figure and multiply by 100 to express it as a percentage. Finally, analyze the percentages to identify trends and patterns.

7.1. Steps for Income Statement Analysis

- Select the income statements for the periods you want to compare.

- Calculate the change in each line item from one period to the next.

- Divide the change by the base period figure.

- Multiply the result by 100 to express it as a percentage.

- Analyze the percentages to identify revenue growth, cost trends, and profit margin changes.

7.2. Steps for Balance Sheet Analysis

- Select the balance sheets for the periods you want to compare.

- Calculate the change in each line item from one period to the next.

- Divide the change by the base period figure.

- Multiply the result by 100 to express it as a percentage.

- Analyze the percentages to understand changes in assets, liabilities, and equity.

7.3. Example of Horizontal Analysis Calculation

Consider a company with the following revenue figures:

- Year 1 Revenue: $1,000,000

- Year 2 Revenue: $1,200,000

To perform horizontal analysis:

- Change in Revenue: $1,200,000 – $1,000,000 = $200,000

- Percentage Change: ($200,000 / $1,000,000) * 100 = 20%

This analysis shows that revenue increased by 20% from Year 1 to Year 2.

8. Combining Vertical and Horizontal Analysis for Comprehensive Insights

Combining vertical and horizontal analysis provides a comprehensive view of a company’s financial performance. Vertical analysis offers a snapshot of a company’s financial structure at a specific point in time, while horizontal analysis reveals trends and changes over time. By using both methods, stakeholders can gain a deeper understanding of a company’s strengths, weaknesses, and potential risks.

8.1. Synergistic Benefits

The synergistic benefits of combining vertical and horizontal analysis include:

- Comprehensive Understanding: Provides a complete picture of a company’s financial health.

- Trend Identification: Helps identify both short-term and long-term trends.

- Informed Decision-Making: Supports better decisions related to investments, strategic planning, and resource allocation.

8.2. Practical Application

For example, if vertical analysis shows that COGS is a high percentage of revenue, and horizontal analysis reveals that COGS is increasing over time, it may indicate a need to improve cost control measures.

9. Real-World Examples and Case Studies

To illustrate the practical application of vertical and horizontal analysis, let’s consider a few real-world examples and case studies.

9.1. Case Study 1: Retail Company

A retail company experienced a decline in net income. Vertical analysis of the income statement revealed that operating expenses had increased as a percentage of revenue. Horizontal analysis showed that these expenses had been steadily rising over the past three years. This prompted management to investigate and implement cost-cutting measures, resulting in improved profitability.

9.2. Case Study 2: Manufacturing Firm

A manufacturing firm wanted to assess its financial health. Vertical analysis of the balance sheet showed that a significant portion of its assets was tied up in inventory. Horizontal analysis revealed that inventory turnover had slowed down over the past year. This led management to optimize its inventory management practices, reducing holding costs and improving cash flow.

9.3. Example: Technology Startup

A tech startup is evaluating its financial performance to attract investors. They present the following data:

Income Statement (Year 2)

- Revenue: $2,000,000

- Cost of Goods Sold: $800,000

- Operating Expenses: $600,000

- Net Income: $600,000

Vertical Analysis:

- COGS as % of Revenue: ($800,000 / $2,000,000) * 100 = 40%

- Operating Expenses as % of Revenue: ($600,000 / $2,000,000) * 100 = 30%

- Net Income as % of Revenue: ($600,000 / $2,000,000) * 100 = 30%

Balance Sheet (Year 2)

- Total Assets: $5,000,000

- Total Liabilities: $1,500,000

- Equity: $3,500,000

Vertical Analysis:

- Liabilities as % of Assets: ($1,500,000 / $5,000,000) * 100 = 30%

- Equity as % of Assets: ($3,500,000 / $5,000,000) * 100 = 70%

Horizontal Analysis (Year 1 vs. Year 2)

| Item | Year 1 | Year 2 | Change | % Change |

|---|---|---|---|---|

| Revenue | $1,500,000 | $2,000,000 | $500,000 | 33.33% |

| Net Income | $400,000 | $600,000 | $200,000 | 50.00% |

| Total Assets | $4,000,000 | $5,000,000 | $1,000,000 | 25.00% |

| Total Liabilities | $1,200,000 | $1,500,000 | $300,000 | 25.00% |

Insights:

- Vertical Analysis: Shows the structure of the company’s finances. COGS is 40% of revenue, indicating efficient cost management. Equity is 70% of assets, suggesting a strong financial position.

- Horizontal Analysis: Reveals significant growth. Revenue increased by 33.33%, and net income by 50%, demonstrating the company’s growth potential.

By presenting this data, the startup can effectively communicate its financial health and growth potential to potential investors.

10. Advantages and Disadvantages of Each Analysis Type

Both vertical and horizontal analysis offer distinct advantages and disadvantages, which are important to consider when conducting financial analysis.

10.1. Advantages of Vertical Analysis

- Standardization: Allows for easy comparison between companies of different sizes.

- Internal Insights: Provides a clear view of the relationships between items within a financial statement.

- Benchmarking: Facilitates comparison with industry averages and competitors.

10.2. Disadvantages of Vertical Analysis

- Limited Scope: Focuses only on internal relationships and does not provide insights into trends over time.

- Static View: Offers a snapshot of a company’s financial position at a specific point in time.

- Accounting Policy Influence: Can be affected by accounting policies and may not capture external factors.

10.3. Advantages of Horizontal Analysis

- Trend Identification: Helps identify trends and changes in financial performance over time.

- Forecasting: Provides a basis for forecasting future results.

- Performance Evaluation: Useful for evaluating the sustainability of a company’s performance.

10.4. Disadvantages of Horizontal Analysis

- External Factor Sensitivity: Can be misleading if significant events or changes in accounting policies occur.

- Underlying Driver Complexity: May not capture the underlying drivers of financial performance.

- Data Dependency: Requires reliable and consistent data from multiple periods.

11. Tools and Technologies for Conducting Financial Analysis

Various tools and technologies are available to assist in conducting vertical and horizontal analysis. These tools range from spreadsheet software to specialized financial analysis platforms.

11.1. Spreadsheet Software

Spreadsheet software, such as Microsoft Excel and Google Sheets, is widely used for financial analysis. These tools allow users to input financial data, perform calculations, and create charts and graphs to visualize trends and relationships.

11.2. Financial Analysis Platforms

Specialized financial analysis platforms, such as Bloomberg Terminal and FactSet, provide comprehensive financial data and analytical tools. These platforms offer advanced features for conducting in-depth financial analysis and creating detailed reports.

11.3. Accounting Software

Accounting software, such as QuickBooks and Xero, can also be used for financial analysis. These tools provide real-time financial data and automated reporting capabilities, making it easier to track financial performance and identify trends.

12. Common Mistakes to Avoid When Performing Financial Analysis

Several common mistakes can undermine the accuracy and effectiveness of financial analysis. Avoiding these pitfalls is crucial for obtaining reliable insights.

12.1. Ignoring External Factors

Failing to consider external factors, such as economic conditions, industry trends, and regulatory changes, can lead to inaccurate conclusions. It’s essential to incorporate these factors into the analysis to provide a more complete picture.

12.2. Relying Solely on Financial Data

Relying solely on financial data without considering qualitative factors, such as management quality, competitive landscape, and brand reputation, can result in a biased analysis.

12.3. Using Inconsistent Data

Using inconsistent data or accounting methods can distort the results of financial analysis. It’s important to ensure that the data is reliable and comparable across periods.

12.4. Overlooking Significant Trends

Overlooking significant trends or anomalies in the data can lead to missed opportunities or potential risks. It’s crucial to carefully examine the data and identify any unusual patterns.

13. The Role of Financial Analysis in Decision Making

Financial analysis plays a vital role in decision-making for various stakeholders, including investors, creditors, and management.

13.1. Investment Decisions

Investors use financial analysis to assess the attractiveness of investment opportunities. By analyzing a company’s financial performance and health, investors can make informed decisions about whether to buy, sell, or hold a stock.

13.2. Credit Decisions

Creditors use financial analysis to evaluate the creditworthiness of borrowers. By assessing a company’s ability to repay its debts, creditors can make informed decisions about whether to extend credit and on what terms.

13.3. Management Decisions

Management uses financial analysis to monitor and improve a company’s financial performance. By analyzing financial data, management can identify areas of strength and weakness and make strategic decisions to enhance profitability and efficiency.

14. E-E-A-T and YMYL Considerations

When creating content about financial analysis, it’s crucial to adhere to the principles of E-E-A-T (Expertise, Experience, Authoritativeness, and Trustworthiness) and YMYL (Your Money or Your Life). These guidelines ensure that the information provided is accurate, reliable, and trustworthy, especially given the potential impact on readers’ financial decisions.

14.1. Expertise

Demonstrate expertise by providing well-researched, accurate, and up-to-date information. Cite credible sources and ensure that the content is free of errors and omissions.

14.2. Experience

Share practical examples and case studies to illustrate the application of financial analysis techniques. Provide insights based on real-world experiences and lessons learned.

14.3. Authoritativeness

Establish authoritativeness by highlighting the credentials and expertise of the content creators. Showcase their experience in the field of finance and their contributions to the industry.

14.4. Trustworthiness

Build trust by providing transparent and unbiased information. Disclose any potential conflicts of interest and ensure that the content is free of promotional or misleading claims.

14.5. YMYL Considerations

Recognize that financial analysis content falls under the YMYL category, as it can impact readers’ financial well-being. Ensure that the content is accurate, reliable, and trustworthy to avoid causing harm.

15. Future Trends in Financial Analysis

The field of financial analysis is constantly evolving, driven by technological advancements and changing business needs. Several key trends are shaping the future of financial analysis.

15.1. Artificial Intelligence (AI)

AI is transforming financial analysis by automating tasks, improving accuracy, and providing deeper insights. AI-powered tools can analyze large datasets, identify patterns, and generate forecasts with greater speed and efficiency.

15.2. Big Data Analytics

Big data analytics is enabling financial analysts to process and analyze vast amounts of data from various sources. This allows for more comprehensive and accurate financial assessments.

15.3. Cloud Computing

Cloud computing is making financial analysis tools and data more accessible and affordable. Cloud-based platforms enable analysts to collaborate and share information more easily.

15.4. Blockchain Technology

Blockchain technology is enhancing the transparency and security of financial transactions. This can improve the reliability of financial data and reduce the risk of fraud.

16. Conclusion: The Power of Comparative Financial Analysis

In conclusion, both vertical and horizontal analysis are essential tools for evaluating a company’s financial performance. Vertical analysis offers a snapshot of a company’s financial structure at a specific point in time, while horizontal analysis reveals trends and changes over time. By combining these methods, stakeholders can gain a comprehensive understanding of a company’s strengths, weaknesses, and potential risks. Whether you’re assessing profitability, monitoring growth, or making strategic decisions, COMPARE.EDU.VN equips you with the insights needed for success.

For in-depth comparisons and objective evaluations, visit COMPARE.EDU.VN. Our platform provides comprehensive analyses, empowering you to make well-informed decisions.

17. Call to Action

Ready to make smarter financial decisions? Visit compare.edu.vn today to explore detailed comparisons and objective evaluations of various financial analysis tools and techniques. Empower yourself with the insights you need to achieve financial success. Our address is 333 Comparison Plaza, Choice City, CA 90210, United States. You can also reach us via Whatsapp at +1 (626) 555-9090.

18. Frequently Asked Questions (FAQ)

1. What is the main difference between vertical and horizontal analysis?

Vertical analysis examines the proportional relationship of items within a single financial statement, while horizontal analysis evaluates changes in financial statement items over time.

2. When should I use vertical analysis?

Use vertical analysis when you want to compare companies of different sizes or assess the relative importance of items within a financial statement.

3. When should I use horizontal analysis?

Use horizontal analysis when you want to identify trends and changes in financial performance over time or forecast future results.

4. Can I use both vertical and horizontal analysis together?

Yes, combining both methods provides a comprehensive view of a company’s financial performance and helps identify both short-term and long-term trends.

5. What are the limitations of vertical analysis?

Vertical analysis is limited by its focus on internal relationships and its static view of a company’s financial position.

6. What are the limitations of horizontal analysis?

Horizontal analysis can be misleading if significant events or changes in accounting policies occur and may not capture the underlying drivers of financial performance.

7. What tools can I use to perform vertical and horizontal analysis?

You can use spreadsheet software, financial analysis platforms, and accounting software to perform these analyses.

8. How does financial analysis help in investment decisions?

Financial analysis helps investors assess the attractiveness of investment opportunities by evaluating a company’s financial performance and health.

9. How does financial analysis help in credit decisions?

Financial analysis helps creditors evaluate the creditworthiness of borrowers by assessing their ability to repay debts.

10. What are the key trends shaping the future of financial analysis?

Key trends include artificial intelligence, big data analytics, cloud computing, and blockchain technology.