A commonly used multiple utilized in comparable company analysis is a powerful valuation technique, relying on key financial ratios and metrics derived from similar publicly traded companies to estimate the value of a target company. This method, facilitated by platforms like COMPARE.EDU.VN, offers a streamlined way to assess fair value by comparing essential financial aspects such as revenue, EBITDA, and other relevant benchmarks. Utilizing this comparative analysis, you gain valuable insights into a company’s worth, making informed decisions in investment or acquisition scenarios. This approach incorporates a range of similar company criteria, valuation benchmarks, and comparative financial metrics for comprehensive assessment.

1. Understanding Comparable Company Analysis

Comparable company analysis (CCA), also known as peer group analysis, is a relative valuation technique that determines the value of a company by examining the metrics of other similar companies. It’s a process of identifying companies that share similar business and financial characteristics with the target company and then calculating key ratios and multiples, such as price-to-earnings (P/E), enterprise value-to-revenue (EV/Revenue), or enterprise value-to-EBITDA (EV/EBITDA). These multiples are then applied to the target company’s corresponding metrics to arrive at an estimated valuation.

CCA is widely used in investment banking, private equity, and corporate finance because it provides a market-driven, relatively straightforward approach to valuation. It’s particularly useful when valuing private companies or divisions of larger companies where other valuation methods, such as discounted cash flow (DCF) analysis, may be less reliable due to the difficulty in forecasting future cash flows. The process generally involves several key steps, as detailed below.

1.1. Identifying Comparable Companies

The first and perhaps most critical step in CCA is identifying a suitable peer group. This involves finding publicly traded companies that operate in the same industry as the target company, have similar business models, and face similar risks. Factors to consider when selecting comparable companies include:

- Industry: Companies should operate in the same industry or closely related industries.

- Business Model: Similar revenue sources, customer base, and distribution channels are essential.

- Size: Comparable companies should be of a similar size in terms of revenue, assets, and market capitalization.

- Growth Rate: Companies with similar growth prospects are more likely to provide a relevant comparison.

- Profitability: Companies with similar profit margins and returns on investment are generally more comparable.

- Risk Profile: Companies facing similar economic, regulatory, and competitive risks are more suitable for comparison.

It’s often challenging to find companies that are perfectly comparable to the target company. Therefore, it’s important to use judgment and consider a range of factors to select the most appropriate peer group. COMPARE.EDU.VN offers resources and tools to assist in identifying and comparing companies across various industries.

1.2. Collecting Financial Data

Once the peer group is established, the next step is to collect relevant financial data for each company. This typically includes:

- Revenue: Total sales generated by the company.

- EBITDA: Earnings before interest, taxes, depreciation, and amortization.

- Net Income: The company’s profit after all expenses and taxes.

- Market Capitalization: The total value of the company’s outstanding shares.

- Enterprise Value: A measure of the company’s total value, including debt and equity.

This data can be obtained from various sources, including company financial statements (10-K and 10-Q filings), financial databases (such as Bloomberg, Reuters, or Capital IQ), and market research reports.

1.3. Calculating Key Ratios and Multiples

With the financial data in hand, the next step is to calculate key ratios and multiples for each comparable company. Common multiples used in CCA include:

- Price-to-Earnings (P/E): Market capitalization divided by net income.

- Enterprise Value-to-Revenue (EV/Revenue): Enterprise value divided by revenue.

- Enterprise Value-to-EBITDA (EV/EBITDA): Enterprise value divided by EBITDA.

- Price-to-Book (P/B): Market capitalization divided by book value of equity.

- Price-to-Sales (P/S): Market capitalization divided by revenue.

These multiples provide a standardized way to compare the valuation of different companies. It’s important to calculate multiples using consistent definitions and accounting methods to ensure comparability.

1.4. Applying Multiples to the Target Company

Once the multiples have been calculated for the peer group, the next step is to apply them to the target company. This involves multiplying the target company’s corresponding financial metrics by the average or median multiple from the peer group. For example, if the average EV/EBITDA multiple for the peer group is 10x and the target company’s EBITDA is $10 million, the estimated enterprise value of the target company would be $100 million.

It’s important to consider the specific characteristics of the target company when applying multiples. If the target company is growing faster or has higher profit margins than the peer group, it may be appropriate to use a higher multiple. Conversely, if the target company is smaller or faces greater risks, a lower multiple may be more appropriate.

1.5. Considering Limitations and Adjustments

CCA is not without its limitations. It relies on the assumption that the comparable companies are truly similar to the target company, which may not always be the case. Market conditions, temporary factors, and company-specific events can also distort multiples and lead to inaccurate valuations.

To address these limitations, it’s important to consider the following:

- Adjust for Differences: Make adjustments to multiples to account for differences in size, growth, profitability, and risk.

- Use a Range of Multiples: Instead of relying on a single multiple, consider a range of multiples to arrive at a more realistic valuation.

- Consider Other Valuation Methods: Use CCA in conjunction with other valuation methods, such as DCF analysis or precedent transactions analysis, to provide a more comprehensive assessment.

COMPARE.EDU.VN provides tools and resources to help users identify and adjust for differences between companies, ensuring a more accurate and reliable valuation.

2. Benefits of Using Comparable Company Analysis

Comparable company analysis offers several benefits as a valuation technique:

2.1. Market-Driven Approach

CCA is based on actual market data, reflecting the collective wisdom of investors and analysts. This makes it a more objective and market-relevant approach compared to other valuation methods that rely on subjective assumptions. The real-world basis of this technique means the valuations it provides are often more readily accepted and understood by stakeholders.

2.2. Simplicity and Transparency

Compared to complex valuation models like discounted cash flow analysis, CCA is relatively simple and transparent. The key inputs are readily available, and the calculations are straightforward. This simplicity makes it easier to explain and defend the valuation to clients, investors, and other stakeholders.

2.3. Relative Valuation

CCA provides a relative valuation, which means it values the company in relation to its peers. This can be particularly useful when valuing private companies or divisions of larger companies where absolute valuations are difficult to obtain. The relative nature of CCA makes it a practical tool for benchmarking and comparative analysis.

2.4. Flexibility

CCA can be applied to a wide range of companies and industries. The flexibility of this approach makes it a versatile tool for valuation professionals.

2.5. Adaptability

CCA can incorporate various metrics, including revenue, EBITDA, and non-GAAP measures, providing flexibility in situations where traditional metrics are not meaningful. This adaptability ensures that CCA can be tailored to the specific characteristics of the company being valued.

3. Pitfalls to Avoid in Comparable Company Analysis

Despite its benefits, CCA also has several pitfalls that must be avoided to ensure accurate and reliable valuations:

3.1. Difficulty Finding Truly Comparable Companies

One of the biggest challenges in CCA is finding companies that are truly comparable to the target company. Differences in size, business model, growth rate, and risk profile can make it difficult to find a peer group that is representative of the target company.

3.2. Market Conditions and Temporary Factors

Market conditions and temporary factors can distort multiples and lead to inaccurate valuations. For example, an outlier M&A transaction with a large premium or factors specific to a comparable company can result in overvaluation.

3.3. Subjectivity in Selecting Multiples and Making Adjustments

Selecting the appropriate multiples and making adjustments for differences between companies requires judgment and can be subjective. Different analysts may arrive at different valuations based on their interpretation of the data.

3.4. Lack of Forward-Looking Information

CCA is based on historical data and may not reflect future growth prospects or changes in market conditions. This can be a limitation when valuing high-growth companies or companies in rapidly changing industries.

3.5. Reliance on Publicly Available Data

CCA relies on publicly available data, which may not always be accurate or reliable. Financial statements may be subject to accounting manipulations, and analyst forecasts may be biased or overly optimistic.

4. Common Valuation Multiples in Comparable Company Analysis

Several valuation multiples are commonly used in CCA, each with its own strengths and weaknesses. The choice of multiple depends on the specific characteristics of the target company and the industry in which it operates.

4.1. Price-to-Earnings (P/E) Ratio

The P/E ratio is one of the most widely used valuation multiples. It is calculated by dividing the market capitalization of a company by its net income. The P/E ratio indicates how much investors are willing to pay for each dollar of earnings.

- Strengths: Simple to calculate and widely understood.

- Weaknesses: Can be distorted by accounting manipulations and may not be meaningful for companies with negative earnings.

4.2. Enterprise Value-to-Revenue (EV/Revenue) Ratio

The EV/Revenue ratio is calculated by dividing the enterprise value of a company by its revenue. This multiple is useful for valuing companies with negative earnings or inconsistent profitability.

- Strengths: Not affected by accounting manipulations and can be used to value companies with negative earnings.

- Weaknesses: Does not take into account differences in profitability or capital structure.

4.3. Enterprise Value-to-EBITDA (EV/EBITDA) Ratio

The EV/EBITDA ratio is calculated by dividing the enterprise value of a company by its EBITDA. This multiple is widely used in valuation because it reflects the company’s operating performance without being affected by financing or accounting decisions.

- Strengths: Not affected by financing or accounting decisions and can be used to compare companies with different capital structures.

- Weaknesses: May not be meaningful for companies with significant capital expenditures or working capital requirements.

4.4. Price-to-Book (P/B) Ratio

The P/B ratio is calculated by dividing the market capitalization of a company by its book value of equity. This multiple is useful for valuing companies with significant tangible assets, such as banks or real estate companies.

- Strengths: Provides a measure of the company’s net asset value.

- Weaknesses: May not be meaningful for companies with significant intangible assets or companies in asset-light industries.

4.5. Price-to-Sales (P/S) Ratio

The P/S ratio is calculated by dividing the market capitalization of a company by its revenue. This multiple is useful for valuing companies with high growth rates or companies in industries with low profit margins.

- Strengths: Simple to calculate and can be used to value companies with negative earnings.

- Weaknesses: Does not take into account differences in profitability or capital structure.

5. Trailing vs. Forward Multiples

When applying comparable multiples, it’s important to decide whether to use trailing multiples (based on historical data) or forward multiples (based on projected data). Each approach has its own advantages and disadvantages.

5.1. Trailing Multiples

Trailing multiples are based on historical financial data, such as the last twelve months (LTM) or trailing twelve months (TTM). These multiples provide a measure of the company’s performance over the past year.

- Advantages: Data is readily available and reliable.

- Disadvantages: May not reflect future growth prospects or changes in market conditions.

5.2. Forward Multiples

Forward multiples are based on projected financial data, such as analyst forecasts or company guidance. These multiples provide a measure of the company’s expected performance in the future.

- Advantages: Reflects future growth prospects and changes in market conditions.

- Disadvantages: Data may be unreliable or biased.

In general, forward multiples are more appropriate for valuing high-growth companies or companies in rapidly changing industries. However, it’s important to carefully evaluate the reliability of the projected data before using forward multiples.

6. Impact of Peer Groups on Valuation

The selection of the peer group can have a significant impact on the valuation derived from CCA. Therefore, it’s important to carefully consider the characteristics of the peer group and ensure that it is representative of the target company.

6.1. Niche Competitor Subset vs. Broad Competitor Set

Using a niche competitor subset can provide a more accurate valuation if the target company is highly specialized or operates in a niche market. However, using a broad competitor set may be more appropriate if the target company competes with a wide range of companies in different industries.

6.2. Example of Peer Group Impact

Consider a high-growth data analytics SaaS technology company that provides less diversified product offerings than its direct public competitors. In this case, using a niche competitor subset consisting of five directly comparable companies that have recently gone public may provide a more accurate valuation than using a broad competitor set.

7. Precedent Transaction Analysis vs. Comparable Company Analysis

In addition to CCA, precedent transaction analysis is another relative valuation technique that can be used to value companies. Precedent transaction analysis involves examining the pricing metrics of mergers and acquisitions (M&A) transactions involving similar companies.

7.1. Similarities and Differences

Both CCA and precedent transaction analysis are based on market data and provide a relative valuation. However, CCA uses the trading multiples of publicly traded companies, while precedent transaction analysis uses the transaction multiples of M&A deals.

7.2. Advantages and Disadvantages

CCA is generally more transparent and easier to apply than precedent transaction analysis. However, precedent transaction analysis may provide a more accurate valuation if there are recent M&A deals involving similar companies.

7.3. When to Use Each Method

CCA is typically used when valuing companies that are not likely to be acquired in the near future. Precedent transaction analysis is typically used when valuing companies that are likely to be acquired or when assessing the fairness of a proposed M&A deal.

8. Case Studies of Comparable Company Analysis

To illustrate the application of CCA, let’s consider a few case studies:

8.1. Example 1: Semiconductor Designer and Manufacturer

A semiconductor designer and manufacturer that specializes in microchips for artificial intelligence (AI) applications is on the verge of an exit and has been profitable for the last six years. In this case, precedent transaction analysis may be more appropriate than CCA because the company is likely to be acquired.

8.2. Example 2: High-Growth Series B Technology Company

A high-growth Series B technology company that specializes in enterprise communication software is utilizing venture capital financing to scale. In this case, forward revenue multiples may be more appropriate than trailing revenue multiples because the company is experiencing significant historical revenue growth.

8.3. Example 3: Mid-to-Large PE-Backed Technology Firm

A mid-to-large PE-backed technology firm that specializes in mapping family history and ancestry generates significant EBITDA margins. In this case, EV/EBITDA multiples may be more appropriate than other multiples because the company has consistent EBITDA margins.

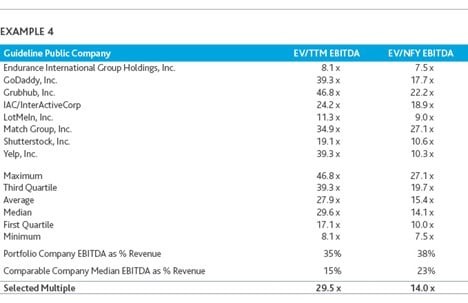

Valuation Example 4

Valuation Example 4

9. Conclusion: Implementing Effective Comparable Company Analysis

Comparable company analysis is a powerful valuation technique that can be used to estimate the value of a company by examining the metrics of other similar companies. However, it’s important to carefully consider the limitations of CCA and avoid the pitfalls that can lead to inaccurate valuations.

By following best practices, such as carefully selecting the peer group, calculating key ratios and multiples, and considering the specific characteristics of the target company, valuation professionals can use CCA to arrive at a reasonable range of fair value.

Remember that no company operates in a vacuum. The public market offers a continuous evaluation of similar businesses. Don’t disregard the insights this provides. For further exploration of comparable company analysis and other valuation techniques, visit COMPARE.EDU.VN at 333 Comparison Plaza, Choice City, CA 90210, United States. You can also contact us via Whatsapp at +1 (626) 555-9090.

10. Frequently Asked Questions (FAQs) About Comparable Company Analysis

To further enhance understanding of comparable company analysis, here are some frequently asked questions:

10.1. What is the primary goal of comparable company analysis?

The primary goal is to determine the fair value of a target company by comparing its financial metrics to those of similar publicly traded companies.

10.2. How do you select comparable companies for analysis?

Select companies that operate in the same industry, have similar business models, are of similar size, and have similar growth and risk profiles.

10.3. What are the key multiples used in comparable company analysis?

Key multiples include Price-to-Earnings (P/E), Enterprise Value-to-Revenue (EV/Revenue), and Enterprise Value-to-EBITDA (EV/EBITDA).

10.4. Why is it important to adjust multiples in comparable company analysis?

Adjusting multiples accounts for differences in size, growth, profitability, and risk, ensuring a more accurate valuation.

10.5. What are the limitations of using trailing multiples?

Trailing multiples are based on historical data and may not reflect future growth prospects or changes in market conditions.

10.6. When is it appropriate to use forward multiples?

Forward multiples are appropriate for valuing high-growth companies or companies in rapidly changing industries.

10.7. How does the selection of the peer group impact valuation?

The selection of the peer group can significantly impact the valuation, making it important to ensure the group is representative of the target company.

10.8. What is the difference between precedent transaction analysis and comparable company analysis?

Comparable company analysis uses trading multiples of publicly traded companies, while precedent transaction analysis uses transaction multiples of M&A deals.

10.9. When should you use precedent transaction analysis?

Use precedent transaction analysis when valuing companies that are likely to be acquired or when assessing the fairness of a proposed M&A deal.

10.10. How can COMPARE.EDU.VN assist in performing comparable company analysis?

COMPARE.EDU.VN provides resources and tools to identify and compare companies, ensuring a more accurate and reliable valuation.

Ready to make informed decisions? Visit COMPARE.EDU.VN to explore detailed comparisons and find the best choices tailored to your needs. Our comprehensive analysis ensures you’re equipped to make confident decisions every time. Check out compare.edu.vn today for comparisons that count.