403b Compare tools, like those found on COMPARE.EDU.VN, offer a comprehensive way to evaluate different retirement plan options. Our platform enables you to identify the best choices based on your individual needs, offering retirement savings insights and financial planning resources to secure your financial future. Discover more about retirement options and investment strategies with our financial comparison tools.

1. Understanding 403(b) Plans: A Comprehensive Overview

What is a 403(b) plan and how does it work? A 403(b) plan is a retirement savings plan available to employees of public schools, certain tax-exempt organizations, and ministers. It works similarly to a 401(k) plan, allowing employees to contribute pre-tax dollars, reducing their current taxable income, while their investments grow tax-deferred until retirement. These plans often include a range of investment options, such as mutual funds and annuity contracts.

1.1. Eligibility and Participation in 403(b) Plans

Who is eligible for a 403(b) plan? Employees of public education systems, such as teachers and school staff, certain non-profit organizations, like hospitals and charities, and ministers are typically eligible for 403(b) plans. Eligibility criteria can vary depending on the employer’s specific plan rules, but generally, any employee working for a qualifying organization can participate.

1.2. Contributions to 403(b) Plans: Employee and Employer

How much can you contribute to a 403(b) plan? In 2024, the maximum employee contribution to a 403(b) plan is $23,000. Employees age 50 and over can make an additional catch-up contribution of $7,500, bringing their total possible contribution to $30,500. Some plans also allow employer matching contributions, which can further boost retirement savings.

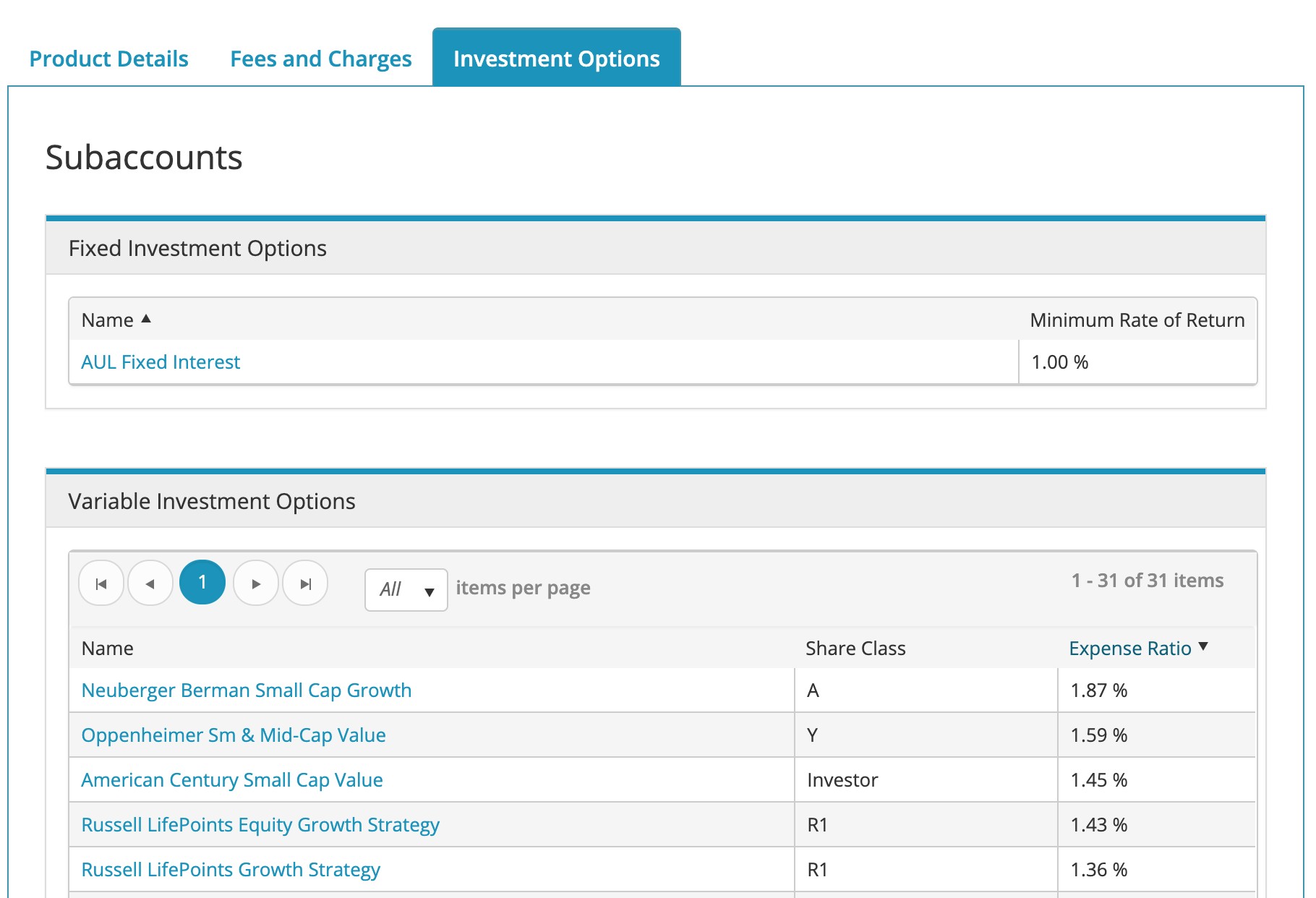

1.3. Investment Options Available in 403(b) Plans

What investment options are typically available in a 403(b) plan? Common investment options include mutual funds (stock, bond, and target-date funds), fixed and variable annuities, and sometimes employer stock. The specific investment options available depend on the plan provider and the employer’s selections. Diversifying investments across different asset classes is a key strategy for managing risk and maximizing returns.

1.4. Tax Advantages of 403(b) Plans

What are the tax advantages of a 403(b) plan? Contributions to a 403(b) plan are made on a pre-tax basis, which reduces your current taxable income. The earnings on your investments grow tax-deferred, meaning you don’t pay taxes on them until you withdraw the money in retirement. This can result in significant tax savings over the long term. Some plans also offer a Roth 403(b) option, where contributions are made after-tax but withdrawals in retirement are tax-free.

1.5. Understanding Vesting Schedules in 403(b) Plans

What is a vesting schedule in a 403(b) plan? A vesting schedule determines when you have full ownership of your employer’s contributions to your 403(b) plan. Employee contributions are always 100% vested immediately. Employer matching contributions, however, may be subject to a vesting schedule, such as a graded vesting (e.g., 20% per year of service) or cliff vesting (e.g., 100% after three years of service). Understanding the vesting schedule is crucial to know when you have full rights to your retirement funds.

2. Key Factors to Consider When Comparing 403(b) Plans

What are the essential factors to consider when you 403b compare? When evaluating 403(b) plans, focus on fees, investment options, historical performance, and the financial strength of the provider. Lower fees can significantly increase your long-term returns, while a diverse range of investment options allows you to align your portfolio with your risk tolerance and retirement goals. Utilize COMPARE.EDU.VN to analyze and compare these key elements, ensuring you make an informed decision that supports your retirement objectives.

2.1. Assessing and Comparing Fees in 403(b) Plans

How do you assess and compare fees in 403(b) plans? Fees in 403(b) plans can include administrative fees, investment management fees (expense ratios), and surrender charges. Administrative fees cover the cost of managing the plan, while expense ratios are charged by mutual funds to cover their operating expenses. Surrender charges may apply if you withdraw money early from certain investments, like annuities. To compare fees, request a detailed breakdown from each plan provider and calculate the total cost based on your investment amount. Look for plans with low expense ratios and minimal administrative fees to maximize your investment returns.

2.2. Evaluating Investment Options in 403(b) Plans

What should you look for when evaluating investment options in a 403(b) plan? Look for a variety of investment options that align with your risk tolerance and retirement timeline. This may include stock funds, bond funds, target-date funds, and balanced funds. Check the historical performance of each investment option and compare it to its benchmark. Ensure that the plan offers low-cost index funds or ETFs, which can provide broad market exposure at a lower cost than actively managed funds. Diversification is key to managing risk, so choose a mix of investments that span different asset classes and sectors.

2.3. Understanding the Importance of Historical Performance

Why is historical performance important when choosing investments in a 403(b) plan? While past performance is not a guarantee of future results, it can provide insights into how an investment has performed relative to its peers and benchmark. Review the long-term performance of each investment option (e.g., 5-year, 10-year returns) and compare it to similar investments. Consider both returns and risk-adjusted returns (e.g., Sharpe ratio) to assess whether the investment has generated strong returns for the level of risk taken. Keep in mind that market conditions can change, so it’s important to consider performance in different economic environments.

2.4. Assessing the Financial Strength of the Provider

How do you assess the financial strength of a 403(b) plan provider? Assessing the financial strength of a 403(b) plan provider involves evaluating their credit ratings from agencies like Standard & Poor’s, Moody’s, and Fitch. Higher ratings indicate a lower risk of default. Also, review the provider’s history, stability, and reputation in the industry. Look for providers with a long track record of managing retirement plans and a strong financial foundation. This ensures that the provider can meet its obligations and protect your retirement savings.

2.5. Retirement Goals and Risk Tolerance Alignment

How do you align your investment choices with your retirement goals and risk tolerance? Determine your retirement goals, such as the age you plan to retire and the income you’ll need. Assess your risk tolerance, considering how comfortable you are with market volatility and potential losses. If you have a long time until retirement, you may be able to take on more risk with a higher allocation to stocks. If you are closer to retirement, you may prefer a more conservative approach with a higher allocation to bonds. Choose investment options that align with your goals and risk tolerance, and rebalance your portfolio periodically to maintain your desired asset allocation.

3. Step-by-Step Guide to Using COMPARE.EDU.VN for 403(b) Comparisons

How can COMPARE.EDU.VN help you 403b compare? COMPARE.EDU.VN offers a streamlined approach to evaluating 403(b) plans by providing detailed comparisons of fees, investment options, and historical performance. Our platform allows you to input your specific criteria and receive personalized recommendations. Use COMPARE.EDU.VN to gain clear, actionable insights that empower you to make well-informed decisions about your retirement savings, ensuring a secure financial future.

3.1. Navigating the COMPARE.EDU.VN Interface

How do you navigate the COMPARE.EDU.VN interface to find 403(b) information? Start by visiting the COMPARE.EDU.VN website. Use the search bar to enter “403(b) plans.” You will find a dedicated section for comparing 403(b) plans. The interface is designed to be user-friendly, with clear navigation and search filters to help you quickly find the information you need. You can browse by provider, investment type, or specific features to narrow down your options.

3.2. Utilizing Search Filters and Comparison Tools

What search filters and comparison tools are available on COMPARE.EDU.VN? COMPARE.EDU.VN offers a range of search filters to help you narrow down your 403(b) plan options. You can filter by fees (e.g., expense ratio, administrative fees), investment options (e.g., stock funds, bond funds, target-date funds), historical performance (e.g., 5-year, 10-year returns), and provider ratings. The comparison tools allow you to compare multiple plans side-by-side, highlighting the key differences in fees, investment options, and performance. This makes it easy to identify the best plan for your needs.

3.3. Reading and Interpreting Plan Details on COMPARE.EDU.VN

How do you read and interpret plan details on COMPARE.EDU.VN? Each 403(b) plan on COMPARE.EDU.VN has a detailed profile with information on fees, investment options, historical performance, and provider ratings. Start by reviewing the fee structure, paying attention to expense ratios, administrative fees, and any other charges. Examine the investment options to see if they align with your risk tolerance and retirement goals. Review the historical performance of each investment option and compare it to its benchmark. Finally, consider the provider’s ratings and financial strength. Use this information to assess whether the plan is a good fit for your needs.

3.4. Creating Side-by-Side Comparisons

How do you create a side-by-side comparison of 403(b) plans on COMPARE.EDU.VN? Once you have identified a few 403(b) plans that interest you, use the side-by-side comparison tool on COMPARE.EDU.VN. Select the plans you want to compare, and the tool will display their key features, fees, investment options, and performance metrics in a clear, easy-to-read format. This allows you to quickly identify the strengths and weaknesses of each plan and make an informed decision. You can customize the comparison by selecting the specific criteria that are most important to you.

3.5. Saving and Sharing Your Research

Can you save and share your 403(b) research on COMPARE.EDU.VN? Yes, COMPARE.EDU.VN allows you to save your research and share it with others. You can create an account to save your favorite 403(b) plans, comparison results, and other research materials. This makes it easy to track your progress and revisit your findings later. You can also share your research with a financial advisor, family member, or colleague by sending them a link to your saved information. This facilitates collaboration and ensures that you have the support you need to make informed decisions about your retirement savings.

4. Understanding Fees: A Critical Component of 403(b) Plans

Why is it important to understand fees when you 403b compare? Understanding fees is crucial because they directly impact your long-term investment returns. COMPARE.EDU.VN provides detailed breakdowns of various fee types, helping you to see how these costs can accumulate over time. By comparing fee structures, you can identify cost-effective plans that maximize your savings. With COMPARE.EDU.VN, make informed decisions that help you achieve your retirement goals with less financial burden.

4.1. Types of Fees in 403(b) Plans

What are the different types of fees in 403(b) plans? Fees in 403(b) plans can be categorized into several types:

- Administrative Fees: These cover the cost of managing the plan, including record-keeping, compliance, and customer service.

- Investment Management Fees (Expense Ratios): These are charged by mutual funds or other investment options to cover their operating expenses.

- Surrender Charges: These may apply if you withdraw money early from certain investments, such as annuities.

- Transaction Fees: These can include fees for buying or selling investments within the plan.

- Advisory Fees: If you use a financial advisor, they may charge a fee for their services.

Understanding these fees is essential for evaluating the true cost of a 403(b) plan.

4.2. How Fees Impact Long-Term Returns

How do fees impact long-term investment returns in a 403(b) plan? Fees can significantly reduce your long-term investment returns. Even seemingly small fees can compound over time and erode your savings. For example, a 1% annual fee can reduce your retirement savings by as much as 28% over 30 years, according to a study by the U.S. Department of Labor. By choosing low-fee investment options and minimizing administrative fees, you can maximize your investment returns and reach your retirement goals sooner.

4.3. Benchmarking Fees Against Industry Averages

How do you benchmark fees against industry averages to determine if a 403(b) plan is cost-effective? To benchmark fees, compare the fees in your 403(b) plan to industry averages for similar plans and investment options. Resources like BrightScope and the Investment Company Institute (ICI) provide data on average fees for different types of retirement plans and mutual funds. If your plan’s fees are higher than the industry average, consider exploring lower-cost alternatives. Keep in mind that fees can vary depending on the size of the plan and the types of investments offered.

4.4. Negotiating Fees with Plan Providers

Can you negotiate fees with 403(b) plan providers? In some cases, it may be possible to negotiate fees with 403(b) plan providers, especially if your employer offers the plan. Employers can negotiate with providers to lower administrative fees or offer lower-cost investment options. If you are an employee, you can advocate for lower fees by raising the issue with your employer or plan sponsor. Collective bargaining or group negotiations may also be effective in reducing fees. Even small reductions in fees can make a big difference in your long-term returns.

4.5. Hidden Fees and How to Spot Them

What are some hidden fees in 403(b) plans and how can you spot them? Hidden fees in 403(b) plans can include:

- 12b-1 Fees: These are marketing and distribution fees charged by mutual funds.

- Sub-Transfer Agency (Sub-TA) Fees: These are fees paid to third-party administrators for record-keeping services.

- Wrap Fees: These are fees charged for bundled services, such as investment management and financial planning.

- Inactive Account Fees: These may be charged if you have a small balance or haven’t made contributions recently.

To spot these fees, carefully review the plan documents and fee disclosures. Ask your plan provider for a detailed breakdown of all fees and charges. Be wary of plans with complex fee structures or vague descriptions of fees.

5. Evaluating Investment Options: Stocks, Bonds, and More

How do you evaluate investment options when you 403b compare? Evaluating investment options requires understanding your risk tolerance and long-term goals. COMPARE.EDU.VN provides detailed information on stocks, bonds, mutual funds, and other investment vehicles available within 403(b) plans. Our platform helps you assess the potential risks and rewards of each option, enabling you to diversify your portfolio effectively. With COMPARE.EDU.VN, gain the insights you need to make informed investment decisions that align with your financial objectives.

5.1. Understanding Different Asset Classes

What are the different asset classes available in 403(b) plans? The main asset classes available in 403(b) plans include:

- Stocks: Represent ownership in companies and offer the potential for high growth but also carry higher risk.

- Bonds: Represent debt and provide more stable returns with lower risk compared to stocks.

- Mutual Funds: Pools of money invested in a diversified portfolio of stocks, bonds, or other assets.

- Exchange-Traded Funds (ETFs): Similar to mutual funds but trade like stocks on an exchange.

- Target-Date Funds: Automatically adjust their asset allocation over time to become more conservative as you approach your retirement date.

- Annuities: Contracts with an insurance company that provide a stream of income in retirement.

Understanding these asset classes is crucial for building a diversified portfolio.

5.2. The Importance of Diversification

Why is diversification important in a 403(b) plan? Diversification is important because it helps to reduce risk and improve returns. By spreading your investments across different asset classes, sectors, and geographic regions, you can minimize the impact of any single investment on your overall portfolio. A well-diversified portfolio is more likely to weather market volatility and achieve your long-term retirement goals.

5.3. Analyzing Risk and Return Potential

How do you analyze the risk and return potential of different investment options in a 403(b) plan? To analyze risk and return potential, consider the following factors:

- Historical Performance: Review the long-term performance of the investment option, including its returns, volatility, and risk-adjusted returns (e.g., Sharpe ratio).

- Investment Strategy: Understand the investment strategy of the fund or asset class. Is it focused on growth, income, or a combination of both?

- Expense Ratio: Consider the expense ratio, which is the annual fee charged to manage the fund.

- Risk Metrics: Look at risk metrics such as standard deviation and beta to assess the volatility of the investment.

- Market Outlook: Consider the current market conditions and economic outlook.

Use this information to assess whether the investment option aligns with your risk tolerance and retirement goals.

5.4. Target-Date Funds: A Hands-Off Approach

What are target-date funds and how do they work in a 403(b) plan? Target-date funds are mutual funds that automatically adjust their asset allocation over time to become more conservative as you approach your retirement date. They are designed to simplify retirement investing by providing a diversified portfolio that is tailored to your specific retirement timeline. As you get closer to retirement, the fund will gradually shift its assets from stocks to bonds, reducing risk. Target-date funds are a convenient option for investors who prefer a hands-off approach to retirement investing.

5.5. Evaluating Actively vs. Passively Managed Funds

How do you evaluate actively vs. passively managed funds in a 403(b) plan? Actively managed funds are managed by a fund manager who tries to outperform the market by selecting specific investments. Passively managed funds, such as index funds, track a specific market index and aim to match its performance. To evaluate these options, consider the following:

- Fees: Passively managed funds typically have lower fees than actively managed funds.

- Performance: Compare the historical performance of the fund to its benchmark.

- Manager Expertise: Evaluate the experience and track record of the fund manager.

- Investment Strategy: Understand the investment strategy of the fund and whether it aligns with your goals.

Research suggests that passively managed funds often outperform actively managed funds over the long term, especially after accounting for fees.

6. Retirement Planning Strategies for 403(b) Participants

What are some effective retirement planning strategies for 403(b) participants? Effective strategies include maximizing contributions, diversifying investments, and regularly reviewing your plan. COMPARE.EDU.VN offers tools and resources to help you create a personalized retirement plan that aligns with your financial goals. By using COMPARE.EDU.VN, you can stay informed and make proactive decisions to secure a comfortable retirement.

6.1. Maximizing Contributions to Your 403(b) Plan

How do you maximize contributions to your 403(b) plan to reach your retirement goals? To maximize contributions, aim to contribute the maximum amount allowed by law each year. In 2024, the maximum employee contribution is $23,000, with an additional catch-up contribution of $7,500 for those age 50 and over. If your employer offers matching contributions, contribute enough to take full advantage of the match. Increase your contributions gradually over time as your income grows. Consider automating your contributions to ensure consistency.

6.2. Asset Allocation and Rebalancing Strategies

What are effective asset allocation and rebalancing strategies for a 403(b) plan? Asset allocation involves dividing your investments among different asset classes, such as stocks, bonds, and cash, based on your risk tolerance and retirement timeline. Rebalancing involves periodically adjusting your asset allocation to maintain your desired mix of investments. A common strategy is to rebalance annually or whenever your asset allocation deviates significantly from your target. Rebalancing helps to ensure that your portfolio stays aligned with your risk tolerance and retirement goals.

6.3. Rollover Options: Moving Your 403(b) Funds

What are the rollover options for moving your 403(b) funds to another account? You can roll over your 403(b) funds to another 403(b) plan, a 401(k) plan, or an IRA (Individual Retirement Account). A direct rollover involves transferring the funds directly from your 403(b) plan to the new account. An indirect rollover involves receiving a check from your 403(b) plan and then depositing it into the new account within 60 days. Rolling over your funds can provide greater investment flexibility and control over your retirement savings.

6.4. Understanding Withdrawal Rules and Penalties

What are the withdrawal rules and penalties for 403(b) plans? Generally, you can start withdrawing money from your 403(b) plan without penalty at age 59 1/2. Withdrawals before age 59 1/2 are typically subject to a 10% early withdrawal penalty, as well as income taxes. There are some exceptions to the penalty, such as for qualified disability, medical expenses, or a qualified domestic relations order (QDRO). Understanding these rules is essential for avoiding costly penalties and maximizing your retirement savings.

6.5. Seeking Professional Financial Advice

When should you seek professional financial advice for your 403(b) plan? You should consider seeking professional financial advice if you are unsure about how to invest your 403(b) funds, need help with retirement planning, or want a second opinion on your investment strategy. A financial advisor can provide personalized advice based on your individual circumstances and help you make informed decisions about your retirement savings. Look for a qualified and experienced financial advisor who is a fiduciary, meaning they are legally obligated to act in your best interest.

7. Case Studies: Real-Life 403(b) Comparison Scenarios

How can case studies help you understand 403b compare scenarios? Case studies provide real-world examples of how different 403(b) plans perform under various circumstances. COMPARE.EDU.VN offers case studies that illustrate the impact of fees, investment choices, and market conditions on retirement outcomes. By reviewing these scenarios, you can gain a better understanding of the factors that influence your retirement savings and make more informed decisions.

7.1. Comparing Plans with Different Fee Structures

How do different fee structures affect the long-term performance of 403(b) plans? Let’s consider two hypothetical 403(b) plans:

- Plan A: Has an expense ratio of 0.50% and no administrative fees.

- Plan B: Has an expense ratio of 1.50% and annual administrative fees of $50.

Assuming an initial investment of $10,000 and an annual return of 7%, the difference in fees can have a significant impact over time. After 30 years, Plan A would have a balance of approximately $76,123, while Plan B would have a balance of approximately $54,379. This demonstrates the importance of comparing fee structures and choosing plans with low fees.

7.2. Evaluating Investment Choices in Varying Market Conditions

How do different investment choices perform in varying market conditions within a 403(b) plan? Consider two investment options:

- Stock Fund: Invests primarily in stocks and offers the potential for high growth but also carries higher risk.

- Bond Fund: Invests primarily in bonds and provides more stable returns with lower risk.

During bull markets, the stock fund is likely to outperform the bond fund. However, during bear markets, the bond fund is likely to hold up better than the stock fund. Diversifying your portfolio across both stocks and bonds can help to balance risk and return in varying market conditions.

7.3. Impact of Employer Matching Contributions

How do employer matching contributions affect retirement savings in a 403(b) plan? Employer matching contributions can significantly boost your retirement savings. For example, if your employer matches 50% of your contributions up to 6% of your salary, you could receive an additional 3% of your salary in matching contributions each year. Over time, these matching contributions can compound and significantly increase your retirement balance. Always take full advantage of employer matching contributions to maximize your retirement savings.

7.4. The Effects of Early Withdrawals on Retirement Savings

What are the effects of early withdrawals on retirement savings in a 403(b) plan? Early withdrawals from a 403(b) plan can have a significant negative impact on your retirement savings. In addition to the 10% early withdrawal penalty, you will also have to pay income taxes on the withdrawal. Furthermore, you will lose the potential for those funds to grow tax-deferred over time. Avoid early withdrawals whenever possible to protect your retirement savings.

7.5. Optimizing 403(b) Plans for Different Age Groups

How should 403(b) plans be optimized for different age groups to align with their retirement goals? For younger employees, it may be appropriate to invest more aggressively in stocks to maximize long-term growth. As you get closer to retirement, you may want to gradually shift your assets to bonds to reduce risk. Consider your age, risk tolerance, and retirement timeline when making investment decisions. Regularly review and adjust your asset allocation as your circumstances change.

8. Common Mistakes to Avoid When Choosing a 403(b) Plan

What are the common mistakes to avoid when you 403b compare? Common mistakes include not comparing fees, ignoring investment options, and failing to understand the plan rules. COMPARE.EDU.VN helps you avoid these pitfalls by providing comprehensive information and comparison tools. With COMPARE.EDU.VN, you can make well-informed decisions that safeguard your financial future.

8.1. Not Comparing Fees

Why is it a mistake not to compare fees when selecting a 403(b) plan? Not comparing fees is a significant mistake because fees can significantly reduce your long-term investment returns. Even small differences in fees can compound over time and erode your savings. Always compare the fees of different 403(b) plans before making a decision.

8.2. Ignoring Investment Options

Why is it a mistake to ignore investment options when choosing a 403(b) plan? Ignoring investment options is a mistake because the investment choices you make can have a significant impact on your retirement savings. Choose investment options that align with your risk tolerance and retirement goals. Diversify your portfolio across different asset classes to reduce risk.

8.3. Failing to Understand Plan Rules

Why is it important to understand the rules of a 403(b) plan before investing? Failing to understand the rules of a 403(b) plan can lead to costly mistakes. Make sure you understand the contribution limits, vesting schedule, withdrawal rules, and other important plan provisions. Consult with a financial advisor if you have any questions.

8.4. Not Taking Advantage of Employer Matching

Why should you always take advantage of employer matching contributions in a 403(b) plan? Not taking advantage of employer matching contributions is like leaving free money on the table. Employer matching contributions can significantly boost your retirement savings and help you reach your goals sooner. Always contribute enough to your 403(b) plan to take full advantage of the employer match.

8.5. Neglecting to Review and Adjust Your Plan

Why is it important to review and adjust your 403(b) plan regularly? Neglecting to review and adjust your 403(b) plan regularly can lead to suboptimal results. Your circumstances, risk tolerance, and retirement goals may change over time, so it’s important to periodically review and adjust your plan accordingly. Rebalance your portfolio as needed to maintain your desired asset allocation.

9. Future Trends in 403(b) Plans: What to Expect

What are the future trends in 403(b) plans? Expect to see increased transparency, lower fees, and more personalized investment options. COMPARE.EDU.VN stays ahead of these trends to provide you with the most current and relevant information. By using COMPARE.EDU.VN, you can prepare for the future and make informed decisions that maximize your retirement savings potential.

9.1. Increased Transparency in Fees and Investment Options

How will increased transparency affect 403(b) plan participants? Increased transparency in fees and investment options will make it easier for 403(b) plan participants to understand the true cost of their plans and make informed decisions about their investments. Regulatory changes and industry initiatives are driving increased transparency, which will benefit plan participants.

9.2. Lower Fees Due to Increased Competition

How will increased competition among plan providers affect fees in 403(b) plans? Increased competition among plan providers is likely to drive fees lower, as providers compete for business. This will benefit plan participants by reducing the cost of saving for retirement. Look for plans with low fees and transparent fee structures.

9.3. More Personalized Investment Options

How will more personalized investment options benefit 403(b) plan participants? More personalized investment options will allow 403(b) plan participants to tailor their investment portfolios to their individual circumstances, risk tolerance, and retirement goals. This will improve retirement outcomes and help participants achieve their financial objectives.

9.4. Greater Emphasis on Financial Wellness

How will a greater emphasis on financial wellness affect 403(b) plan participants? A greater emphasis on financial wellness will provide 403(b) plan participants with the tools and resources they need to make informed decisions about their finances. This will improve financial literacy and help participants achieve their financial goals.

9.5. Technology-Driven Innovations in Plan Management

How will technology-driven innovations affect the management of 403(b) plans? Technology-driven innovations are streamlining the management of 403(b) plans, making it easier for participants to access information, monitor their accounts, and make investment decisions. Online tools, mobile apps, and robo-advisors are improving the user experience and making retirement planning more accessible.

10. Frequently Asked Questions (FAQs) About 403(b) Plans

10.1. What is the difference between a 403(b) and a 401(k) plan?

What are the key differences between 403(b) and 401(k) retirement plans? 403(b) plans are for employees of public schools and non-profit organizations, while 401(k) plans are for employees of for-profit companies. Both offer pre-tax contributions and tax-deferred growth, but investment options and administrative details may vary.

10.2. Can I contribute to both a 403(b) and a Roth IRA?

Is it possible to contribute to both a 403(b) and a Roth IRA in the same year? Yes, you can contribute to both a 403(b) and a Roth IRA in the same year, subject to certain income limitations for Roth IRA contributions.

10.3. What happens to my 403(b) if I change jobs?

What are the options for your 403(b) plan if you change jobs? If you change jobs, you can typically roll over your 403(b) funds to another 403(b) plan, a 401(k) plan, or an IRA.

10.4. Are 403(b) plans protected from creditors in case of bankruptcy?

Are 403(b) retirement plans protected from creditors in the event of bankruptcy? Yes, 403(b) plans are generally protected from creditors in case of bankruptcy, subject to certain limitations.

10.5. How do I find a financial advisor who specializes in 403(b) plans?

How can you find a qualified financial advisor who specializes in 403(b) retirement plans? You can find a financial advisor who specializes in 403(b) plans by searching online directories, asking for referrals from friends or colleagues, or contacting professional organizations such as the Certified Financial Planner Board of Standards.

10.6. What are the tax implications of withdrawing money from a 403(b) plan in retirement?

What are the tax implications when withdrawing funds from a 403(b) plan during retirement? Withdrawals from a traditional 403(b) plan in retirement are taxed as ordinary income. Roth 403(b) withdrawals, if qualified, are tax-free.

10.7. How often should I review my 403(b) plan and investment options?

How frequently should you review your 403(b) plan and investment options to ensure they align with your goals? You should review your 403(b) plan and investment options at least annually, or more frequently if there are significant changes in your circumstances or market conditions.

10.8. Can I borrow money from my 403(b) plan?

Is it possible to borrow money from your 403(b) retirement plan? Some 403(b) plans allow you to borrow money from your account, subject to certain limitations and repayment terms.

10.9. What are the advantages of a Roth 403(b) compared to a traditional 403(b)?

What are the main advantages of choosing a Roth 403(b) over a traditional 403(b) plan? The main advantage of a Roth 403(b) is that qualified withdrawals in retirement are tax-free, while traditional 403(b) withdrawals are taxed as ordinary income.

10.10. How does 403(b) compare with similar options like 457 plans?

What are the key differences between a 403(b) plan and a 457 retirement plan? Both 403(b) and 457 plans are retirement savings options for public sector and non-profit employees, but 457 plans may offer different rules regarding withdrawals and eligibility.

Choosing the right 403(b) plan requires careful consideration and comparison. COMPARE.EDU.VN provides the tools and resources you need to make informed decisions and secure your financial future.

Ready to take control of your retirement savings? Visit COMPARE.EDU.VN today to compare 403(b) plans, assess your options, and make the best choice for your future. Our comprehensive comparison tools, detailed plan information, and expert insights will empower you to make confident decisions about your retirement.

Contact us for more information:

Address: 333 Comparison Plaza, Choice City, CA 90210, United States

WhatsApp: +1 (626) 555-9090

Website: compare.edu.vn