An appraiser’s role isn’t about wanting you to leave comparables; it’s about unbiased property valuation. COMPARE.EDU.VN offers resources to understand property appraisal, focusing on comprehensive evaluation and fair market value assessments. Discover the criteria for comparable sales, and appraisal guidelines, and learn how to navigate the appraisal process effectively on our website.

1. What Do Appraisers Consider As Comparables?

Appraisers primarily focus on finding comparables that closely resemble the subject property to determine its market value. Comparables, often called “comps,” are recently sold properties that share similar characteristics with the property being appraised. Key considerations include location, size, age, condition, style, and features. The more similar the comparables are to the subject property, the more reliable they are as indicators of value.

To elaborate, let’s break down the key elements appraisers consider when selecting comparables:

- Location: Comparables should ideally be located in the same neighborhood or a similar, competing neighborhood. Proximity is crucial because property values can vary significantly even within short distances due to factors like school districts, amenities, and neighborhood characteristics.

- Size and Living Area: The square footage of the living area should be similar. Appraisers typically look for comps within a reasonable range, such as 10-20% of the subject property’s size.

- Age and Condition: Newer properties often command higher prices, so the age of the comparables should be close to that of the subject property. The condition of the properties, including any renovations or upgrades, is also an important factor.

- Style and Design: Similar architectural styles are preferred. For example, a colonial house should ideally be compared to other colonial houses, and a ranch-style house should be compared to other ranch-style houses.

- Features and Amenities: Features like the number of bedrooms and bathrooms, garage spaces, наличие fireplaces, pools, and other amenities should be comparable. Any significant differences must be adjusted for in the appraisal.

Appraisers gather data on these characteristics from various sources, including:

- Multiple Listing Service (MLS): The MLS is a comprehensive database of real estate listings that provides detailed information on properties that have been sold or are currently for sale.

- Public Records: County assessor and recorder offices maintain public records on property characteristics, sales data, and tax assessments.

- On-Site Inspections: Appraisers conduct thorough inspections of both the subject property and the comparables to verify the information they have gathered and to assess the condition and features of each property.

By carefully analyzing these factors and comparing them to the subject property, appraisers can arrive at a well-supported opinion of value.

2. Why Is Location Important for Comparables?

Location is paramount when selecting comparables because it directly impacts property value. Properties in desirable neighborhoods with good schools, low crime rates, and convenient access to amenities typically command higher prices. Consequently, appraisers prioritize finding comparables in the same or similar neighborhoods to accurately reflect the subject property’s market value.

The significance of location can be further understood by examining the various elements that contribute to its value:

- School Districts: Properties located in highly-rated school districts often have higher values due to the perceived benefit of access to quality education.

- Neighborhood Amenities: Proximity to parks, recreational facilities, shopping centers, restaurants, and other amenities can increase property values.

- Crime Rates: Low crime rates contribute to a sense of safety and security, making neighborhoods more desirable and driving up property values.

- Accessibility: Easy access to major roads, public transportation, and employment centers can enhance property values.

- Views and Natural Features: Properties with desirable views or access to natural features like waterfronts, forests, or mountains can command premium prices.

Considering these factors, appraisers meticulously analyze the location of both the subject property and the potential comparables. They assess the neighborhood characteristics, amenities, and overall desirability to ensure that the comparables are truly representative of the subject property’s market.

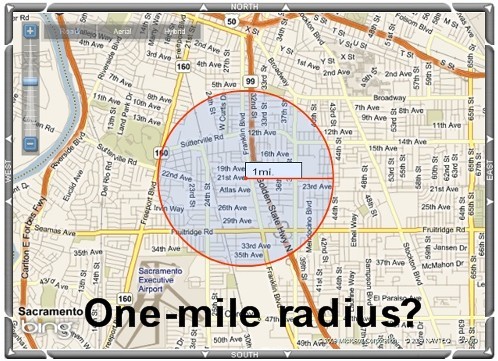

one-mile-radius

one-mile-radius

A one-mile radius helps maintain the integrity of property valuations in similar neighborhoods.

3. What Is Considered a Reasonable Distance for Comparables?

A reasonable distance for comparables largely depends on the property type and the density of the area. In suburban settings, appraisers often try to find comparables within a one-mile radius of the subject property. In rural areas, this distance may extend to five miles or more to account for the lower density of sales.

However, it’s crucial to understand that these are general guidelines, not rigid rules. Appraisers must exercise professional judgment and consider the specific circumstances of each appraisal. If there are no suitable comparables within the typical radius, the appraiser may need to expand the search area to find properties that are truly comparable.

Several factors influence the appropriate distance for comparables:

- Property Type: Unique properties, such as luxury homes or waterfront properties, may require a wider search area to find suitable comparables.

- Market Activity: In active markets with numerous sales, it may be possible to find ample comparables within a small radius. In slower markets, a wider search area may be necessary.

- Geographical Barriers: Natural barriers like rivers, mountains, or highways can create distinct market areas. Appraisers must consider these barriers when determining the appropriate distance for comparables.

- Neighborhood Boundaries: Appraisers should be mindful of neighborhood boundaries and avoid crossing into significantly different neighborhoods unless there is a compelling reason to do so.

4. Can Appraisers Use Comparables From Different Neighborhoods?

Yes, appraisers can use comparables from different neighborhoods, but they must justify their reasoning. If there are no suitable comparables within the immediate neighborhood, an appraiser may look to competing neighborhoods. This decision should be based on a thorough analysis of market conditions and a clear explanation in the appraisal report.

When using comparables from different neighborhoods, appraisers should provide a detailed explanation of why they chose those properties and how the neighborhoods compare. This explanation should address any significant differences between the neighborhoods, such as:

- School District Ratings: Compare the ratings of the school districts serving each neighborhood.

- Property Values: Analyze the overall property values in each neighborhood to determine if there are significant differences.

- Amenities: Compare the availability of amenities like parks, shopping centers, and restaurants in each neighborhood.

- Crime Rates: Compare the crime rates in each neighborhood to assess the safety and security of each area.

- Market Trends: Analyze the recent sales trends in each neighborhood to identify any significant differences in market activity.

By addressing these factors and providing a clear explanation, appraisers can support their decision to use comparables from different neighborhoods and ensure that the appraisal report is credible and reliable.

5. How Many Comparables Does an Appraiser Need?

Appraisers typically need a minimum of three closed sales as comparables. These should be the most similar properties available. Additional supporting sales may be included to strengthen the analysis, but the primary focus is on the three best comparables.

In addition to the three closed sales, appraisers may also include:

- Active Listings: Current listings of similar properties can provide insights into the current market conditions and the competition that the subject property faces.

- Pending Sales: Properties that are under contract but have not yet closed can indicate the direction of the market and provide an early indication of future sales prices.

- Prior Sales of the Subject Property: If the subject property has been sold recently, the prior sale can be a valuable data point for the appraiser.

- Re-Sales of Comparables: If any of the comparables have been resold recently, this can provide additional information about market trends and the stability of property values.

While appraisers focus on the three best comparables, they consider all available data to arrive at a well-supported opinion of value.

6. What Happens If There Are No Good Comparables Available?

If there are no good comparables available, the appraiser must expand their search area, consider alternative appraisal methods, or disclose the limitations in the appraisal report. In some cases, the appraiser may have to decline the assignment if a reliable valuation cannot be determined.

Alternative appraisal methods may include:

- Cost Approach: This approach estimates the value of the property by calculating the cost to build a new replica, less depreciation. It is often used for unique properties or when comparable sales data is limited.

- Income Approach: This approach estimates the value of the property based on the income it generates. It is typically used for investment properties like apartments or commercial buildings.

In addition to expanding the search area and considering alternative appraisal methods, appraisers should also:

- Consult with Other Appraisers: Seeking input from experienced appraisers in the area can provide valuable insights and help identify potential comparables that may have been overlooked.

- Communicate with the Client: Appraisers should communicate with their clients about the challenges they are facing and discuss potential solutions.

- Document the Efforts: Appraisers should thoroughly document all of the steps they have taken to find comparables and explain why they chose the properties that they did.

7. How Do Appraisers Adjust for Differences Between Comparables and the Subject Property?

Appraisers adjust for differences between comparables and the subject property by making monetary adjustments to the sales prices of the comparables. These adjustments reflect the estimated value of each difference, such as an extra bedroom, a larger lot, or a renovated kitchen.

The process of making adjustments involves:

- Identifying Differences: The appraiser must carefully identify all of the significant differences between the comparables and the subject property.

- Estimating the Value of Each Difference: The appraiser must estimate the monetary value of each difference based on market data and their professional judgment.

- Applying Adjustments: The appraiser adds value to the comparable if it is inferior to the subject property and subtracts value if it is superior.

Common adjustments include:

- Location: Adjustments may be made to reflect differences in neighborhood desirability, school district ratings, or proximity to amenities.

- Size and Living Area: Adjustments are typically made on a per-square-foot basis to account for differences in living area.

- Age and Condition: Adjustments may be made to reflect differences in age, condition, or the presence of renovations or upgrades.

- Features and Amenities: Adjustments are made for differences in the number of bedrooms and bathrooms, garage spaces, fireplaces, pools, and other amenities.

The goal of the adjustment process is to make the comparables as similar as possible to the subject property so that the adjusted sales prices accurately reflect the subject property’s market value.

8. What Is the Role of Underwriters in the Appraisal Process?

Underwriters review appraisal reports to ensure they meet lender guidelines and Fannie Mae or Freddie Mac requirements. They may question appraisers about their comp selections, adjustments, or conclusions if anything seems inconsistent or unsupported.

Underwriters play a critical role in the appraisal process by:

- Ensuring Compliance: Underwriters verify that the appraisal report complies with all applicable regulations and guidelines, including those issued by Fannie Mae, Freddie Mac, and the lender.

- Assessing Risk: Underwriters evaluate the appraisal report to assess the risk associated with the loan. They look for any red flags that could indicate that the property is overvalued or that the borrower may have difficulty repaying the loan.

- Protecting the Lender: Underwriters protect the lender’s interests by ensuring that the appraisal report is accurate, reliable, and well-supported.

- Maintaining Independence: Underwriters must maintain independence from the appraiser and avoid any influence that could compromise the integrity of the appraisal process.

If an underwriter has concerns about the appraisal report, they may:

- Request Additional Information: The underwriter may ask the appraiser to provide additional information or documentation to support their conclusions.

- Order a Second Appraisal: In some cases, the underwriter may order a second appraisal from a different appraiser to verify the value of the property.

- Decline the Loan: If the underwriter is not satisfied with the appraisal report, they may decline the loan.

9. How Can Homeowners Help Ensure an Accurate Appraisal?

Homeowners can help ensure an accurate appraisal by providing the appraiser with information about recent improvements, a list of comparable sales they believe are relevant, and access to all areas of the property. Honesty and transparency are key.

Specifically, homeowners can:

- Provide a List of Improvements: Compile a list of all recent improvements, including the dates of completion and the costs.

- Gather Comparable Sales Data: Research recent sales of similar properties in the neighborhood and provide this information to the appraiser.

- Highlight Unique Features: Point out any unique features of the property that may not be readily apparent, such as energy-efficient upgrades or custom landscaping.

- Grant Access to All Areas: Ensure that the appraiser has access to all areas of the property, including the attic, basement, and any outbuildings.

- Be Present During the Appraisal: Be present during the appraisal to answer any questions the appraiser may have and to provide additional information as needed.

- Be Respectful and Professional: Treat the appraiser with respect and professionalism, and avoid any attempts to influence their opinion of value.

10. What Should You Do If You Disagree With an Appraisal?

If you disagree with an appraisal, you can provide the lender with additional information to support a different valuation, request a second appraisal, or challenge the appraisal through the lender’s dispute resolution process. It’s important to act promptly and provide credible evidence.

Here are the steps you can take if you disagree with an appraisal:

- Review the Appraisal Report: Carefully review the appraisal report to understand the appraiser’s reasoning and identify any errors or omissions.

- Gather Supporting Documentation: Compile any documentation that supports your opinion of value, such as comparable sales data, contractor estimates for recent improvements, or evidence of unique features.

- Contact the Lender: Contact your lender and explain why you disagree with the appraisal. Provide them with your supporting documentation and ask them to reconsider the appraisal.

- Request a Second Appraisal: If the lender is unwilling to reconsider the appraisal, you can request a second appraisal from a different appraiser. Be prepared to pay for the second appraisal yourself.

- Challenge the Appraisal: If you believe that the appraiser violated appraisal standards or engaged in unethical conduct, you can file a complaint with the appropriate regulatory agency.

11. What Are Common Issues Appraisers Face When Finding Comparables?

Appraisers often struggle with finding comparables in areas with limited sales data, unique properties, or rapidly changing markets. They must also navigate challenges related to data accuracy and subjective adjustments.

Some of the most common issues appraisers face include:

- Limited Sales Data: In some areas, there may be very few recent sales of similar properties, making it difficult to find reliable comparables.

- Unique Properties: Properties with unique features or architectural styles can be challenging to appraise because there may be few or no comparable sales.

- Rapidly Changing Markets: In rapidly appreciating or depreciating markets, it can be difficult to find comparables that accurately reflect current market conditions.

- Data Accuracy: Appraisers rely on data from various sources, such as the MLS and public records, which may not always be accurate or complete.

- Subjective Adjustments: Making adjustments for differences between comparables and the subject property involves a degree of subjectivity, which can lead to disagreements and challenges.

- Appraiser Bias: Appraiser bias, whether conscious or unconscious, can influence the appraisal process and lead to inaccurate valuations.

To overcome these challenges, appraisers must:

- Expand Their Search Area: Be willing to expand their search area to find suitable comparables, even if it means going outside of the immediate neighborhood.

- Consider Alternative Appraisal Methods: Explore alternative appraisal methods, such as the cost approach or the income approach, when comparable sales data is limited.

- Consult with Other Appraisers: Seek input from experienced appraisers in the area to gain valuable insights and identify potential comparables.

- Stay Up-to-Date on Market Trends: Continuously monitor market trends and adjust their valuation accordingly.

- Maintain Objectivity: Strive to maintain objectivity and avoid any influence that could compromise the integrity of the appraisal process.

12. What Are the Ethical Considerations for Appraisers When Selecting Comparables?

Appraisers must adhere to a strict code of ethics that requires them to be objective, impartial, and independent. They must avoid any conflicts of interest and ensure that their comp selections are based on factual data and sound judgment, not on pressure from clients or other parties.

Key ethical considerations for appraisers include:

- Objectivity: Appraisers must be objective and impartial in their valuations, avoiding any bias or prejudice.

- Independence: Appraisers must be independent and free from any undue influence from clients or other parties.

- Confidentiality: Appraisers must maintain the confidentiality of their clients’ information.

- Competency: Appraisers must be competent to perform the appraisal and have the necessary knowledge, skills, and experience.

- Integrity: Appraisers must act with integrity and honesty in all of their dealings.

- Disclosure: Appraisers must disclose any conflicts of interest or other factors that could affect their objectivity.

13. How Do Appraisers Use Technology to Find Comparables?

Appraisers use a variety of technological tools to find comparables, including online databases, mapping software, and automated valuation models (AVMs). These tools help them efficiently search for and analyze data on potential comparables.

Here are some of the technologies appraisers use:

- Multiple Listing Service (MLS): The MLS is a comprehensive database of real estate listings that provides detailed information on properties that have been sold or are currently for sale.

- Public Records Databases: Online databases provide access to public records on property characteristics, sales data, and tax assessments.

- Mapping Software: Mapping software allows appraisers to visualize the location of the subject property and potential comparables and to analyze the surrounding area.

- Automated Valuation Models (AVMs): AVMs are computer-based models that use statistical analysis to estimate the value of a property based on data from various sources.

- Geographic Information Systems (GIS): GIS software allows appraisers to analyze geographic data, such as school district boundaries, crime rates, and proximity to amenities.

By leveraging these technologies, appraisers can efficiently gather and analyze data on potential comparables, saving time and improving the accuracy of their valuations.

14. How Does the Appraisal Process Differ in Rural Areas Compared to Urban Areas?

The appraisal process in rural areas often differs from that in urban areas due to the lower density of sales and the greater distances between properties. Appraisers in rural areas may need to expand their search area and rely more heavily on their local market knowledge.

Key differences in the appraisal process in rural areas include:

- Wider Search Area: Appraisers in rural areas typically need to expand their search area to find suitable comparables, often exceeding the one-mile radius that is common in urban areas.

- Greater Reliance on Local Market Knowledge: Appraisers in rural areas often rely more heavily on their local market knowledge to assess property values, as there may be less data available from traditional sources.

- More Subjective Adjustments: Making adjustments for differences between comparables and the subject property can be more subjective in rural areas due to the limited availability of data.

- Challenges with Unique Properties: Rural areas often have a higher proportion of unique properties, such as farms, ranches, and waterfront properties, which can be challenging to appraise.

- Increased Travel Time: Appraisers in rural areas often spend more time traveling between properties due to the greater distances between them.

15. Do Renovations Affect What An Appraiser Considers a Comparable?

Yes, renovations significantly affect what an appraiser considers a comparable. Appraisers must consider the extent and quality of renovations when selecting comparables, making adjustments to reflect any differences.

Renovations can impact property value in several ways:

- Improved Condition: Renovations can improve the condition of a property, making it more appealing to buyers and increasing its value.

- Modernized Features: Renovations can modernize the features of a property, such as the kitchen or bathrooms, making it more competitive with newer homes.

- Increased Functionality: Renovations can increase the functionality of a property, such as by adding a bedroom or bathroom, making it more desirable to buyers.

- Enhanced Curb Appeal: Renovations can enhance the curb appeal of a property, making it more attractive to potential buyers.

When selecting comparables, appraisers must consider the extent and quality of any renovations that have been made to the properties. They must make adjustments to reflect any differences in condition, features, and functionality.

For example, if the subject property has a renovated kitchen, the appraiser should look for comparables with renovated kitchens as well. If there are no comparables with renovated kitchens, the appraiser must make an adjustment to reflect the value of the renovation.

16. How Do Economic Factors Influence What An Appraiser Considers a Comparable?

Economic factors, such as interest rates, unemployment rates, and inflation, can significantly influence what an appraiser considers a comparable. These factors affect the overall demand for housing and can impact property values.

- Interest Rates: Lower interest rates can increase the demand for housing, driving up property values. Higher interest rates can decrease the demand for housing, putting downward pressure on property values.

- Unemployment Rates: Lower unemployment rates can increase the demand for housing, as more people have stable incomes and are able to afford homes. Higher unemployment rates can decrease the demand for housing, as more people are out of work and unable to afford homes.

- Inflation: Inflation can erode the purchasing power of consumers, making it more difficult for them to afford homes.

Appraisers must consider these economic factors when selecting comparables and making adjustments. They should look for comparables that have sold under similar economic conditions to the subject property.

For example, if interest rates have risen since the comparable sale, the appraiser should make an adjustment to reflect the impact of the higher interest rates on property values.

17. What Legal Considerations Do Appraisers Have Regarding Comparables?

Appraisers must comply with a variety of legal considerations when selecting comparables, including fair housing laws, appraisal independence requirements, and the Uniform Standards of Professional Appraisal Practice (USPAP).

- Fair Housing Laws: Appraisers must comply with fair housing laws, which prohibit discrimination based on race, color, religion, national origin, sex, familial status, and disability. Appraisers cannot select comparables based on these protected characteristics.

- Appraisal Independence Requirements: Appraisers must be independent and free from any undue influence from clients or other parties. They cannot accept compensation or anything of value that could compromise their independence.

- Uniform Standards of Professional Appraisal Practice (USPAP): Appraisers must comply with USPAP, which sets forth the ethical and performance standards for appraisers. USPAP requires appraisers to be competent, objective, and impartial in their valuations.

18. What Happens if the Best Comparables Are Significantly Different From the Subject Property?

If the best comparables are significantly different from the subject property, the appraiser must acknowledge these differences and make appropriate adjustments. The appraiser should also explain why these comparables were selected and how the adjustments were made.

In cases where the comparables are significantly different from the subject property, the appraiser should:

- Clearly Describe the Differences: The appraiser should clearly describe the differences between the comparables and the subject property.

- Provide a Detailed Explanation of the Adjustments: The appraiser should provide a detailed explanation of the adjustments that were made to reflect these differences.

- Explain Why These Comparables Were Selected: The appraiser should explain why these comparables were selected, even though they are significantly different from the subject property.

- Consider Alternative Appraisal Methods: The appraiser may consider alternative appraisal methods, such as the cost approach or the income approach, if the comparable sales approach is not reliable.

- Disclose the Limitations of the Appraisal: The appraiser should disclose the limitations of the appraisal due to the lack of suitable comparables.

19. How Do Appraisers Handle Foreclosed or Short Sale Comparables?

Appraisers can use foreclosed or short sale comparables, but they must carefully analyze these sales and make adjustments to account for any distressed conditions that may have affected the sale price.

Foreclosed and short sale properties often sell for less than market value due to factors such as:

- Distressed Condition: Foreclosed and short sale properties may be in poor condition due to neglect or deferred maintenance.

- Quick Sale: Foreclosed and short sale properties are often sold quickly, which can depress the sale price.

- Limited Marketing: Foreclosed and short sale properties may not be marketed as effectively as traditional sales.

When using foreclosed or short sale comparables, appraisers must:

- Verify the Sale Details: The appraiser should verify the details of the sale, such as the date, price, and terms.

- Assess the Condition of the Property: The appraiser should assess the condition of the property and make adjustments for any needed repairs or maintenance.

- Analyze the Market Conditions: The appraiser should analyze the market conditions at the time of the sale to determine if there were any factors that may have affected the sale price.

- Make Appropriate Adjustments: The appraiser should make appropriate adjustments to the sale price to account for any distressed conditions.

- Disclose the Use of Foreclosed or Short Sale Comparables: The appraiser should disclose the use of foreclosed or short sale comparables in the appraisal report.

20. What Resources Are Available to Learn More About Appraisal Comparables?

Several resources are available to learn more about appraisal comparables, including appraisal courses, industry publications, and online resources like COMPARE.EDU.VN.

Here are some helpful resources:

- Appraisal Courses: Consider taking an appraisal course to learn more about the appraisal process and how to select comparables.

- Industry Publications: Subscribe to industry publications, such as The Appraisal Journal and Valuation, to stay up-to-date on the latest trends and best practices.

- Online Resources: Explore online resources, such as the Appraisal Institute’s website and COMPARE.EDU.VN, to find information on appraisal comparables.

- Appraisal Organizations: Join appraisal organizations, such as the Appraisal Institute and the American Society of Appraisers, to network with other appraisers and access educational resources.

- Government Agencies: Consult with government agencies, such as the U.S. Department of Housing and Urban Development (HUD) and the Consumer Financial Protection Bureau (CFPB), to learn more about appraisal regulations and requirements.

By utilizing these resources, you can gain a better understanding of appraisal comparables and the appraisal process.

Understanding the intricacies of property appraisal and comparable sales doesn’t have to be daunting. At COMPARE.EDU.VN, we simplify complex information, offering clear comparisons and expert insights to help you make informed decisions. Whether you’re a homeowner, buyer, or real estate professional, our resources are designed to empower you with the knowledge you need. Visit us today at compare.edu.vn to explore our comprehensive guides and tools. For further assistance, contact us at 333 Comparison Plaza, Choice City, CA 90210, United States. Whatsapp: +1 (626) 555-9090.