Comparable company analysis provides valuable insights for financial decisions. COMPARE.EDU.VN offers a comprehensive guide to mastering this technique. Explore comparable ratios, financial modeling, and valuation methodology to make informed choices, leveraging LSI keywords like market multiples and valuation analysis for a complete understanding.

1. What Is Comparable Company Analysis?

Comparable company analysis, often referred to as “comps,” is a valuation technique that assesses a company’s value by examining the ratios of similar public companies. Unlike discounted cash flow (DCF) analysis, which is an intrinsic valuation method, comps is a relative valuation approach. According to a study by NYU Stern School of Business, using a relative valuation approach like comparable company analysis can provide a more accurate valuation in certain market conditions.

1.1 Why Use Comparable Company Analysis?

Comparable company analysis is a crucial tool for analysts in investment banking, equity research, corporate development, and private equity. It provides a benchmark for valuation, helping professionals understand how the market values similar companies. This method is particularly useful when intrinsic valuation is challenging due to a lack of reliable cash flow projections. The technique also enhances financial analysis and decision-making in various financial roles.

1.2 Intrinsic vs. Relative Valuation

Intrinsic valuation determines a company’s value based on its internal factors, such as cash flows and assets. In contrast, relative valuation, like comparable company analysis, values a company based on how it compares to its peers. Intrinsic valuation provides a theoretical value, while relative valuation reflects current market sentiment. A paper from Harvard Business School suggests that combining both methods can provide a more robust valuation.

2. Steps to Perform Comparable Company Analysis

Performing a comparable company analysis involves several steps. Each step is crucial for creating an accurate and reliable valuation. These steps include finding comparable companies, gathering financial data, setting up a comps table, calculating ratios, and interpreting the results.

2.1 Finding Comparable Companies

Identifying the right comparable companies is often the most subjective and challenging part of the analysis. Start by researching the target company on databases like Capital IQ or Bloomberg to understand its industry classification and business description.

2.1.1 Screening Criteria

Screen for companies based on the following criteria:

- Industry Classification: Ensure companies operate in the same industry.

- Geography: Consider companies in similar geographic regions.

- Size: Match companies with comparable revenue, assets, and employee numbers.

- Growth Rate: Look for companies with similar growth trajectories.

- Margins and Profitability: Compare companies with similar profit margins.

According to a report by McKinsey, companies in the same industry tend to have similar valuation multiples.

Comparable Companies

Comparable Companies

2.2 Gathering Financial Information

Once you have identified the comparable companies, the next step is to gather their financial information. Tools like Bloomberg Terminal and Capital IQ allow you to import financial data directly into Excel.

2.2.1 Key Financial Metrics

The financial metrics you need will vary based on the industry and the company’s lifecycle stage. Mature businesses require metrics like EBITDA and EPS, while early-stage companies may focus on Gross Profit or Revenue. Information can also be manually gathered from annual and quarterly reports.

Learn more: list of Bloomberg functions.

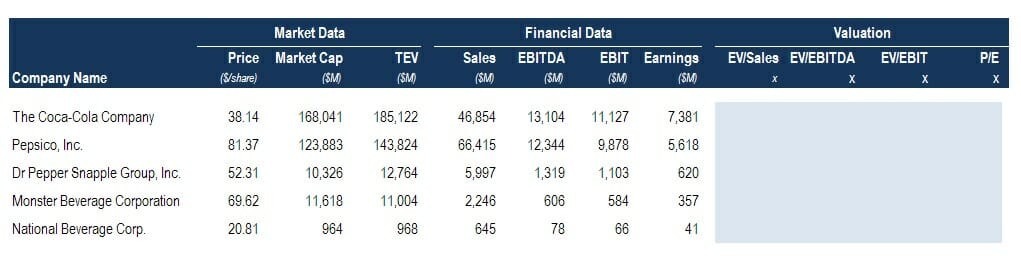

2.3 Setting Up the Comps Table

Organize the financial information in a structured Excel table. This table should list all relevant data about the comparable companies and the target company.

2.3.1 Essential Information

Include the following information in your comps table:

- Company Name

- Ticker Symbol

- Market Capitalization

- Enterprise Value

- Revenue (Current and Projected)

- EBITDA (Current and Projected)

- Net Income

- EPS

- Growth Rates

- Margins

2.4 Calculating Comparable Ratios

Calculate relevant ratios using historical financials and analyst estimates. These ratios help in valuing the target company.

2.4.1 Key Ratios

Include the following ratios in your analysis:

- EV/Revenue: Enterprise Value to Revenue ratio.

- EV/Gross Profit: Enterprise Value to Gross Profit ratio.

- EV/EBITDA: Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization ratio.

- P/E: Price to Earnings ratio.

- P/NAV: Price to Net Asset Value ratio.

- P/B: Price to Book ratio.

2.5 Using Multiples to Value the Target Company

Analysts typically use the average or median multiples from comparable companies to value the target company. These multiples are applied to the target company’s revenue, gross profit, EBITDA, or net income. Outliers are often removed to ensure a meaningful average.

2.5.1 Example Calculation

If the average P/E ratio of the comparable companies is 12.5x, multiply the target company’s earnings by 12.5 to estimate its equity value.

3. Formatting and Presenting the Comps Table

Proper formatting is essential for a clear and understandable comps table. Organize market data, financial data, and multiples into separate sections.

3.1 Formatting Guidelines

- Clearly separate market data, financial data, and multiples.

- Include an “x” next to multiples.

- Present multiples to one decimal place.

- Clearly separate the average or median section at the bottom of the table.

- Indicate any adjustments made to the data.

3.2 Table Structure

| Company | Ticker | Market Cap (USD millions) | Revenue (USD millions) | EBITDA (USD millions) | EV/Revenue | EV/EBITDA |

|---|---|---|---|---|---|---|

| Company A | ABC | 500 | 200 | 50 | 2.5x | 10.0x |

| Company B | DEF | 750 | 300 | 75 | 2.5x | 10.0x |

| Company C | GHI | 1000 | 400 | 100 | 2.5x | 10.0x |

| Average | 2.5x | 10.0x | ||||

| Target Co. | ? | 250 | 60 | ? | ? |

4. Interpreting the Results

Interpreting the results of the comps table involves understanding why certain companies trade at different multiples. This can help identify overvalued or undervalued companies.

4.1 Understanding Multiple Differences

Consider the reasons why one company trades at a discounted EV/EBITDA multiple compared to another. Factors may include:

- Growth rate

- Capital expenditure requirements

- Risk factors

- Management quality

4.2 Qualitative Factors

Remember that comparable company analysis does not include qualitative factors. The interpretation of the results should be done carefully, considering all relevant aspects of the business. Understanding the “why” behind the numbers is crucial for accurate analysis.

5. Applications of Comparable Company Analysis

Comparable company analysis has a wide range of applications in finance. It is commonly used in IPOs, follow-on offerings, M&A advisory, fairness opinions, restructuring, share buybacks, and terminal value calculations in DCF models.

5.1 Initial Public Offerings (IPOs)

Comps are used to determine the appropriate valuation range for companies going public. By comparing the company to its peers, analysts can estimate a fair offering price.

5.2 Mergers & Acquisitions (M&A)

In M&A transactions, comps help assess the value of the target company. It provides a benchmark for negotiations and ensures that the deal is fair for both parties.

5.3 Fairness Opinions

Fairness opinions rely heavily on comparable company analysis. These opinions are used to ensure that the terms of a transaction are fair to shareholders.

5.4 Terminal Value in DCF Models

Multiples are often used to calculate the terminal value in a DCF model. The most common approach is to use an EV/EBITDA multiple based on current market conditions.

6. Multiples and Financial Modeling

Multiples play a significant role in financial modeling. They are used as the terminal value assumption in DCF models and help tie the results back to reality.

6.1 Using Multiples for Reality Checks

If a financial model implies a 30x EV/EBITDA multiple, and none of the comps are trading above 12x, the model may need adjustments. This ensures the model’s output is realistic and aligned with market conditions.

6.2 DCF Model Integration

Using multiples in conjunction with DCF models provides a comprehensive valuation approach. This combines the strengths of both intrinsic and relative valuation methods.

7. Best Practices for Comparable Company Analysis

To conduct an effective comparable company analysis, it’s important to adhere to certain best practices. These practices ensure accuracy, relevance, and reliability in your valuation.

7.1 Ensuring Data Accuracy

Verify all financial data against multiple sources. Cross-reference information from Bloomberg, Capital IQ, and company reports to minimize errors.

7.2 Keeping Information Current

Update your comps table regularly to reflect the most recent financial data and market conditions. This ensures that your analysis remains relevant and accurate.

7.3 Maintaining Objectivity

Avoid bias in your selection of comparable companies and interpretation of results. Strive for objectivity to ensure that your analysis is fair and reliable.

7.4 Understanding Industry Dynamics

Develop a deep understanding of the industry in which the target company operates. This knowledge is crucial for selecting appropriate comparable companies and interpreting the results accurately.

7.5 Using Multiple Valuation Methods

Combine comparable company analysis with other valuation methods, such as discounted cash flow (DCF) analysis, to provide a more comprehensive and robust valuation.

8. Common Mistakes to Avoid

Several common mistakes can undermine the accuracy and reliability of comparable company analysis. Avoiding these pitfalls is crucial for sound valuation.

8.1 Selecting Inappropriate Comps

Choosing companies that are not truly comparable can lead to inaccurate valuation. Ensure that the companies you select have similar business models, growth rates, and risk profiles.

8.2 Relying Solely on Quantitative Data

Over-reliance on quantitative data without considering qualitative factors can lead to misinterpretations. Understand the underlying drivers of performance for each company in your comps table.

8.3 Ignoring Market Conditions

Failing to account for current market conditions can distort your valuation. Consider factors such as interest rates, economic growth, and industry trends.

8.4 Using Stale Data

Using outdated financial data can lead to inaccurate results. Always ensure that your data is current and reflects the most recent financial performance of the comparable companies.

8.5 Overlooking Outliers

Failing to identify and address outliers can skew your analysis. Consider removing or adjusting outliers to ensure that your average and median multiples are representative.

9. The Role of Technology in Comparable Company Analysis

Technology plays a crucial role in streamlining and enhancing comparable company analysis. Various software tools and databases are available to help analysts gather data, perform calculations, and present their findings.

9.1 Bloomberg Terminal

Bloomberg Terminal provides access to real-time financial data, news, and analytics. It allows analysts to screen for comparable companies, gather financial information, and perform ratio analysis.

9.2 Capital IQ

Capital IQ offers comprehensive financial data and analytics for public and private companies. It includes tools for screening, valuation, and financial modeling.

9.3 Excel

Excel is a versatile tool for organizing data, performing calculations, and creating comps tables. It allows analysts to customize their analysis and present their findings in a clear and organized manner.

9.4 Online Databases

Online databases such as Yahoo Finance and Google Finance provide free access to basic financial data. While these resources may not be as comprehensive as Bloomberg or Capital IQ, they can be useful for gathering preliminary information.

9.5 Automation Tools

Automation tools can help streamline the process of gathering data and performing calculations. These tools can save time and reduce the risk of errors.

10. Advanced Techniques in Comparable Company Analysis

Beyond the basic steps, several advanced techniques can enhance the sophistication and accuracy of comparable company analysis.

10.1 Regression Analysis

Regression analysis can be used to identify the key drivers of valuation multiples. By regressing multiples against various financial metrics, analysts can determine which factors have the greatest impact on valuation.

10.2 Sensitivity Analysis

Sensitivity analysis involves testing the impact of different assumptions on the valuation. By varying key inputs such as growth rates and discount rates, analysts can assess the range of potential values for the target company.

10.3 Scenario Analysis

Scenario analysis involves creating different scenarios based on potential future events. By valuing the target company under different scenarios, analysts can assess the range of potential outcomes and identify key risks and opportunities.

10.4 Discount for Lack of Marketability (DLOM)

When valuing private companies, it is important to consider the discount for lack of marketability (DLOM). This discount reflects the fact that private companies are less liquid than public companies.

10.5 Size Premium

Smaller companies may trade at a discount to larger companies due to factors such as increased risk and lower liquidity. A size premium may be applied to account for these factors.

11. Case Studies: Real-World Examples of Comparable Company Analysis

Examining real-world case studies can provide valuable insights into how comparable company analysis is applied in practice.

11.1 Valuing a Tech Startup

Consider a tech startup in the software industry. To value this company, an analyst would identify comparable companies that operate in the same industry, have similar growth rates, and target similar customers. The analyst would then gather financial data for these companies and calculate key ratios such as EV/Revenue and EV/EBITDA. By applying the median multiples from the comparable companies to the startup’s revenue and EBITDA, the analyst can estimate its value.

11.2 Assessing a Retail Chain

Consider a retail chain that is considering a merger or acquisition. To assess the value of this company, an analyst would identify comparable companies that operate in the same industry, have similar store formats, and target similar customers. The analyst would then gather financial data for these companies and calculate key ratios such as P/E and P/B. By applying the median multiples from the comparable companies to the retail chain’s earnings and book value, the analyst can estimate its value.

11.3 Evaluating a Manufacturing Firm

Consider a manufacturing firm that is considering an IPO. To evaluate the value of this company, an analyst would identify comparable companies that operate in the same industry, have similar production processes, and target similar customers. The analyst would then gather financial data for these companies and calculate key ratios such as EV/Revenue and EV/EBITDA. By applying the median multiples from the comparable companies to the manufacturing firm’s revenue and EBITDA, the analyst can estimate its value.

12. Ethical Considerations in Comparable Company Analysis

Ethical considerations are paramount in comparable company analysis. Analysts must adhere to a code of conduct that promotes integrity, objectivity, and fairness.

12.1 Maintaining Confidentiality

Analysts must maintain the confidentiality of sensitive information. This includes non-public information about the target company and the comparable companies.

12.2 Avoiding Conflicts of Interest

Analysts must avoid conflicts of interest. This includes disclosing any relationships that could potentially bias their analysis.

12.3 Ensuring Objectivity

Analysts must ensure that their analysis is objective and unbiased. This includes avoiding any personal opinions or biases that could influence their conclusions.

12.4 Providing Full and Fair Disclosure

Analysts must provide full and fair disclosure of all relevant information. This includes disclosing any limitations or assumptions that could impact the accuracy of their analysis.

12.5 Complying with Regulations

Analysts must comply with all applicable laws and regulations. This includes insider trading laws and securities regulations.

13. Future Trends in Comparable Company Analysis

The field of comparable company analysis is constantly evolving. Several emerging trends are likely to shape the future of this valuation method.

13.1 Increased Use of Artificial Intelligence

Artificial intelligence (AI) is likely to play an increasingly important role in comparable company analysis. AI can be used to automate the process of gathering data, performing calculations, and identifying comparable companies.

13.2 Greater Emphasis on ESG Factors

Environmental, social, and governance (ESG) factors are likely to become more important in valuation. Analysts will need to consider the impact of ESG factors on the value of the target company and the comparable companies.

13.3 More Sophisticated Valuation Techniques

More sophisticated valuation techniques are likely to be developed. This includes the use of regression analysis, sensitivity analysis, and scenario analysis.

13.4 Integration with Big Data Analytics

Comparable company analysis is likely to be integrated with big data analytics. This will allow analysts to access and analyze vast amounts of data, providing them with a more comprehensive view of the market.

13.5 Focus on Non-Financial Metrics

Non-financial metrics such as customer satisfaction, employee engagement, and brand reputation are likely to become more important in valuation. Analysts will need to consider the impact of these metrics on the value of the target company and the comparable companies.

14. Frequently Asked Questions (FAQs) About Comparable Company Analysis

1. What is the primary goal of comparable company analysis?

The primary goal is to determine the fair value of a company by comparing it to similar companies in the same industry, based on key financial ratios and metrics.

2. How do you select comparable companies for analysis?

Comparable companies should be selected based on similar industry, size, growth rate, geography, and business model. The closer the match, the more reliable the analysis.

3. What are the key financial ratios used in comparable company analysis?

Key financial ratios include EV/Revenue, EV/EBITDA, P/E, P/B, and others, depending on the industry and stage of the company.

4. What is the difference between intrinsic and relative valuation methods?

Intrinsic valuation determines value based on internal factors like cash flows, while relative valuation compares a company to its peers based on market data.

5. How do you handle outliers in a comparable company analysis?

Outliers should be carefully examined and potentially removed or adjusted if they skew the results significantly.

6. What role does financial modeling play in comparable company analysis?

Financial modeling helps project future performance and estimate key financial metrics needed for calculating valuation multiples.

7. Why is formatting important in a comps table?

Proper formatting enhances clarity and makes it easier for readers to follow the data and understand the analysis.

8. What are the limitations of comparable company analysis?

Limitations include subjectivity in selecting comps, ignoring qualitative factors, and potential distortion due to market conditions.

9. How can technology enhance the accuracy of comparable company analysis?

Tools like Bloomberg and Capital IQ provide access to real-time data and analytics, streamlining data gathering and calculations, and reducing errors.

10. What ethical considerations should be kept in mind during comparable company analysis?

Ethical considerations include maintaining confidentiality, avoiding conflicts of interest, ensuring objectivity, and complying with regulations.