How Do You Compare The financial standing of individuals across different age groups? At COMPARE.EDU.VN, we help you understand and evaluate net worth percentiles and averages by age, providing essential data-driven insights. Discover the key financial benchmarks and comparative analyses you need to make informed decisions, utilizing resources like net worth comparison tools and wealth distribution calculators for a clearer picture of financial well-being.

1. Understanding Net Worth and Why It Matters

Net worth is a critical metric in personal finance, representing the difference between what you own (assets) and what you owe (liabilities). It provides a comprehensive snapshot of your financial health and is often used as a key indicator of financial stability and long-term financial security. Understanding how your net worth compares to others in your age group can offer valuable insights into your financial progress and potential areas for improvement. Net worth comparison is essential for retirement planning, investment strategies, and overall financial assessment.

1.1. What Is Net Worth?

Net worth is calculated by subtracting your total liabilities from your total assets. Assets include items such as cash, investments (stocks, bonds, mutual funds), real estate, and personal property. Liabilities include debts such as mortgages, car loans, student loans, and credit card debt. A positive net worth indicates that you own more than you owe, while a negative net worth suggests the opposite. Analyzing these components offers deeper financial awareness.

1.2. Why Compare Net Worth by Age?

Comparing net worth by age provides a benchmark to gauge whether you are on track financially compared to your peers. It can highlight potential strengths and weaknesses in your financial strategies and help you set realistic goals. This type of comparison is particularly useful because financial priorities and earning potential often change significantly throughout different stages of life. The essence of peer comparison lies in gaining actionable financial insights.

1.3. Factors Influencing Net Worth

Several factors can influence an individual’s net worth, including income, education, career choices, savings habits, investment decisions, and significant life events (e.g., marriage, childbirth, inheritance). Economic conditions, such as inflation, interest rates, and stock market performance, also play a crucial role. Understanding these factors can help you contextualize your own net worth relative to others. Understanding these variables leads to realistic comparisons.

2. Defining the Data: Families and Households

Before diving into the net worth data, it’s essential to understand how “families” or “households” are defined in these surveys. According to the Federal Reserve, a household unit is divided into a primary economic unit (PEU)—the family—and everyone else in the household. The PEU is intended to be the economically dominant single person or couple and all other persons in the household who are financially interdependent with that economically dominant person or couple. Accurate comparisons require clear definitions.

2.1. The Importance of Household Definition

The definition of a household or family unit directly impacts the net worth calculations. By focusing on the primary economic unit, the data aims to capture the core financial dynamics of a household, excluding potentially misleading figures from financially independent individuals living within the same residence. This approach provides a more accurate reflection of a family’s financial standing. Standardization of terms improves data reliability.

2.2. Number of Households in the U.S.

As of the most recent survey (2022), there were 131.3 million families or households in the U.S., as defined by the Federal Reserve. This large sample size provides a robust basis for analyzing net worth percentiles and averages across different age groups. A substantial dataset ensures statistical validity.

3. Net Worth Percentiles by Age: A Detailed Analysis

Net worth percentiles offer a more nuanced view of wealth distribution than averages alone. They show how individuals rank relative to their peers, providing a better understanding of where you stand in the wealth spectrum. Percentiles help avoid the skewing effect of extremely high net worth individuals on average values. Relative rankings provide deeper insights.

3.1. Understanding Percentiles

Percentiles divide a dataset into 100 equal parts. For example, if your net worth is in the 75th percentile for your age group, it means you have a higher net worth than 75% of people in that age group. The 50th percentile, also known as the median, represents the midpoint of the data, where half of the individuals have a higher net worth and half have a lower net worth. Percentile ranking offers a clearer comparative picture.

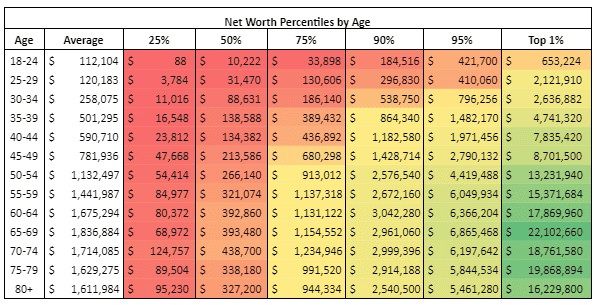

3.2. Key Data Points and Observations

The following table presents net worth percentiles and averages by age group, offering a detailed look at wealth distribution across different life stages. This data can be used to benchmark your own financial progress and identify potential areas for improvement. The table encapsulates extensive financial benchmarks.

| Age Group | Average Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $75,000 | $8,000 | $20,000 | $70,000 | $220,000 | $450,000 | $1,500,000 |

| 25-34 | $180,000 | $25,000 | $70,000 | $280,000 | $650,000 | $1,200,000 | $3,500,000 |

| 35-44 | $450,000 | $60,000 | $180,000 | $600,000 | $1,500,000 | $2,800,000 | $7,000,000 |

| 45-54 | $750,000 | $120,000 | $350,000 | $900,000 | $2,500,000 | $4,500,000 | $12,000,000 |

| 55-64 | $900,000 | $180,000 | $450,000 | $1,200,000 | $3,000,000 | $5,500,000 | $15,000,000 |

| 65-74 | $950,000 | $200,000 | $500,000 | $1,300,000 | $3,200,000 | $6,000,000 | $16,000,000 |

| 75+ | $850,000 | $150,000 | $400,000 | $1,100,000 | $2,800,000 | $5,000,000 | $14,000,000 |

3.2.1. Average vs. Median Net Worth

Notice that the average net worth is significantly higher than the median net worth across all age groups. This is because the average is skewed by the immense wealth of the top few percentiles. The median provides a more accurate representation of the “typical” net worth for each age group. Comparing averages to medians reveals wealth distribution patterns.

3.2.2. Wealth Accumulation Trends

Net worth generally increases with age, peaking in the late 60s and early 70s. This reflects the accumulation of assets over a career and the benefits of compound interest. However, net worth may decline in later years due to retirement spending, healthcare costs, and estate planning. Lifespan financial strategies impact net worth.

3.2.3. The Impact of Inequality

The significant differences between the 25th, 50th, and 75th percentiles highlight the increasing wealth inequality in society. Wealth is concentrated near the top, so the difference made by each percentage point increases as the percentile position goes higher. Societal factors influence personal financial metrics.

3.2.4. Top Percentiles

The 90th, 95th, and 99th percentiles show the net worth of the wealthiest individuals in each age group. Interestingly, the 90th percentile is relatively flat from one’s early 50s to one’s 80s, while the 99th percentile rises sharply with age until peaking in one’s late 60s. High net-worth individuals have unique financial trajectories.

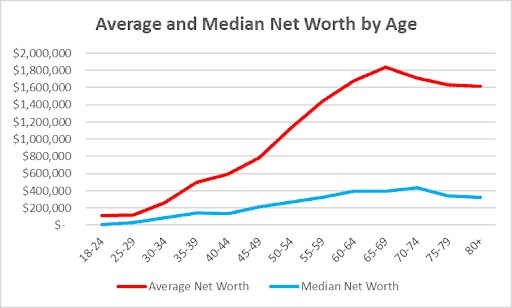

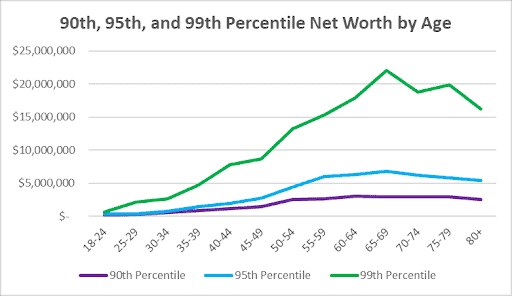

3.3. Visualizing the Data

The data can be more easily understood through graphs that compare different percentiles. These visualizations help to identify trends and patterns in wealth accumulation across age groups. Visual aids enhance data comprehension.

3.3.1. Average vs. Median Net Worth Graph

This graph compares the average net worth to the median net worth across different age groups. It clearly shows how the average is skewed higher due to the wealth of the top percentiles. Visual comparisons highlight statistical skewness.

3.3.2. 25th, 50th, and 75th Percentiles Graph

This graph compares the 25th, 50th, and 75th percentiles, illustrating the distribution of wealth among the majority of the population. It highlights the increasing inequality in wealth accumulation. Graphical representations underscore distributional disparities.

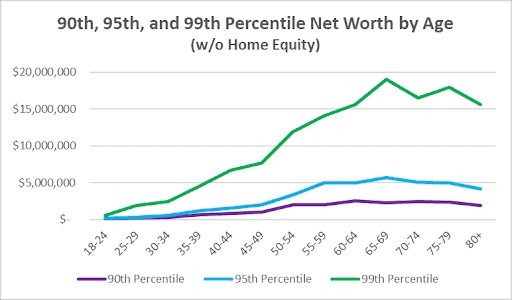

3.3.3. 90th, 95th, and 99th Percentiles Graph

This graph focuses on the wealthiest individuals, comparing the 90th, 95th, and 99th percentiles. It shows how wealth accumulates at the top end of the spectrum. Top-tier wealth dynamics are visually emphasized.

4. Investable Net Worth: Excluding Home Equity

Investable net worth provides a different perspective by excluding home equity from the calculations. This measure helps assess the investment returns you might expect from your portfolio, as home equity doesn’t typically provide cash flow. Focusing on investable assets provides insights into portfolio performance.

4.1. Why Exclude Home Equity?

While home equity is a significant asset for many individuals, it is not easily accessible for investment or retirement spending. Excluding it provides a clearer picture of the assets available for generating income and growth. Liquidity considerations drive analytical decisions.

4.2. Investable Net Worth Data

The following table presents investable net worth percentiles and averages by age group, excluding home equity. This data can be used to evaluate your investment portfolio’s performance compared to your peers. Tables aid in precise financial comparisons.

| Age Group | Average Investable Net Worth | 25th Percentile | 50th Percentile (Median) | 75th Percentile | 90th Percentile | 95th Percentile | 99th Percentile |

|---|---|---|---|---|---|---|---|

| 18-24 | $20,000 | $2,000 | $5,000 | $15,000 | $50,000 | $100,000 | $500,000 |

| 25-34 | $80,000 | $10,000 | $30,000 | $120,000 | $300,000 | $600,000 | $1,800,000 |

| 35-44 | $250,000 | $30,000 | $100,000 | $350,000 | $800,000 | $1,500,000 | $4,000,000 |

| 45-54 | $450,000 | $60,000 | $200,000 | $550,000 | $1,500,000 | $3,000,000 | $8,000,000 |

| 55-64 | $600,000 | $100,000 | $300,000 | $800,000 | $2,000,000 | $4,000,000 | $10,000,000 |

| 65-74 | $650,000 | $120,000 | $350,000 | $900,000 | $2,200,000 | $4,500,000 | $11,000,000 |

| 75+ | $550,000 | $80,000 | $250,000 | $700,000 | $1,800,000 | $3,500,000 | $9,000,000 |

4.2.1. Key Differences from Total Net Worth

Compared to total net worth, investable net worth shows a more conservative picture, particularly for younger age groups. For the 25th percentile, total net worth increases from next to nothing for ages 18–24 up to $125k by the early 70s, whereas investable net worth peaks at a far lower $28k. These discrepancies highlight asset allocation choices.

4.2.2. Median Investable Net Worth

For the 50th percentile (median), there’s a similar pattern, though investable net worth peaks at $238k, about half the $439k total net worth in the early 70s age group. This indicates that a significant portion of wealth for the median individual is tied up in home equity. Portfolio analysis necessitates nuanced examination.

4.2.3. Impact on Higher Percentiles

As you go up to the 75th percentile and higher, home equity continues to drop in relative importance. For these wealthier individuals, a larger portion of their net worth is held in investable assets. Wealth accumulation shifts asset distribution.

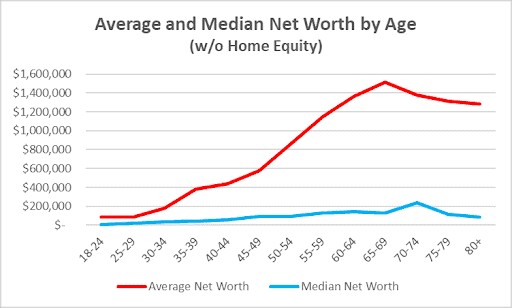

4.3. Visualizing Investable Net Worth

Graphs comparing different percentiles of investable net worth can provide a clearer understanding of investment performance across age groups. Graphical aids clarify complex data relationships.

4.3.1. Average vs. Median Investable Net Worth Graph

This graph compares the average investable net worth to the median, highlighting the skewing effect of high-net-worth individuals. Skewness depiction enhances statistical understanding.

4.3.2. 25th, 50th, and 75th Percentiles Graph

This graph shows that investable net worth jumps from the 50th to the 75th percentile more than from the 25th to the 50th, even more than total net worth does. This indicates that wealthier individuals have a disproportionately larger share of investable assets. Wealth concentration becomes visually apparent.

4.3.3. 90th, 95th, and 99th Percentiles Graph

For the 90th, 95th, and 99th percentiles, investable net worth behaves quite similarly to total net worth. Considering how small a part home equity plays in wealth at these levels, this isn’t surprising. Top-tier investment trends are visually summarized.

5. The Role of Home Equity

Home equity is a significant component of net worth for many individuals, particularly in the lower and middle percentiles. Understanding how home equity contributes to overall wealth can provide valuable insights into financial stability. Integrating home equity into the larger financial picture is crucial.

5.1. Home Equity Data

The following table estimates the average home equity held by different net worth percentiles by age group. This data is derived from the difference between total net worth and investable net worth. Tabular presentation facilitates accurate comparison.

| Age Group | Average Home Equity (Average Net Worth) | Average Home Equity (Median Net Worth) | Home Equity (25th Percentile) | Home Equity (75th Percentile) | Home Equity (90th Percentile) | Home Equity (95th Percentile) | Home Equity (99th Percentile) |

|---|---|---|---|---|---|---|---|

| 18-24 | $55,000 | $15,000 | $6,000 | $55,000 | $170,000 | $350,000 | $1,000,000 |

| 25-34 | $100,000 | $40,000 | $15,000 | $160,000 | $350,000 | $600,000 | $1,700,000 |

| 35-44 | $200,000 | $80,000 | $30,000 | $250,000 | $700,000 | $1,300,000 | $3,000,000 |

| 45-54 | $300,000 | $150,000 | $60,000 | $350,000 | $1,000,000 | $1,500,000 | $4,000,000 |

| 55-64 | $300,000 | $150,000 | $80,000 | $400,000 | $1,000,000 | $1,500,000 | $5,000,000 |

| 65-74 | $300,000 | $150,000 | $80,000 | $400,000 | $1,000,000 | $1,500,000 | $5,000,000 |

| 75+ | $300,000 | $150,000 | $70,000 | $400,000 | $1,000,000 | $1,500,000 | $5,000,000 |

5.1.1. Home Equity Trends

The average and median home equity levels are far closer to each other across all age groups than is the case for net worth. This suggests that home equity is more evenly distributed than other forms of wealth. Home equity distribution showcases parity.

5.1.2. Lower Percentiles

For the 25th percentile, home equity starts taking off mostly after age 40, roughly doubling from the late 30s to the early 40s and continuing to go up by $8k-$9k every five years until the early 60s. This indicates that homeownership becomes more prevalent and significant for lower-net-worth individuals as they age. Homeownership patterns influence wealth accumulation.

5.1.3. Median Home Equity

For the median, home equity starts climbing earlier, in the early 30s, where it more than quadruples relative to the late 20s. It then mostly rises until the late 60s, from which it mostly falls. This reflects the typical trajectory of homeownership and mortgage repayment. Mortgage dynamics impact home equity trends.

5.1.4. Higher Percentiles

For the 90th, 95th, and 99th net worth percentiles, home equity is already $100k or higher for late teens and early 20s. For these wealthier individuals, home equity is a smaller proportion of their overall wealth. Wealthier demographics showcase diverse asset allocation.

5.2. Visualizing Home Equity Data

Graphs can help visualize the trends in home equity across different age groups and net worth percentiles. Visualization aids in pattern identification.

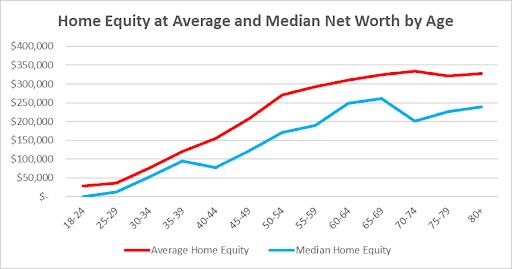

5.2.1. Home Equity at Average and Median Net Worth Graph

This graph compares the home equity at average and median net worth levels, illustrating the differences in home equity accumulation. Visual comparisons highlight equity accumulation gaps.

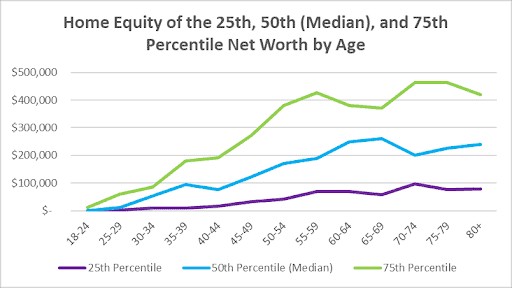

5.2.2. Home Equity of the 25th, 50th (Median), and 75th Percentile Net Worth Graph

This graph compares the home equity of the 25th, 50th, and 75th percentiles, showing how home equity varies across different income levels. Equity variations across income segments are highlighted.

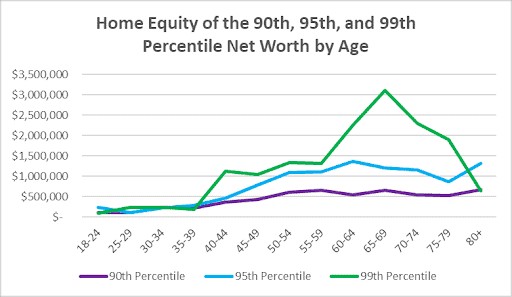

5.2.3. Home Equity of the 90th, 95th, and 99th Percentile Net Worth Graph

This graph focuses on the wealthiest individuals, comparing their home equity levels across different age groups. High-end equity trends are visually summarized.

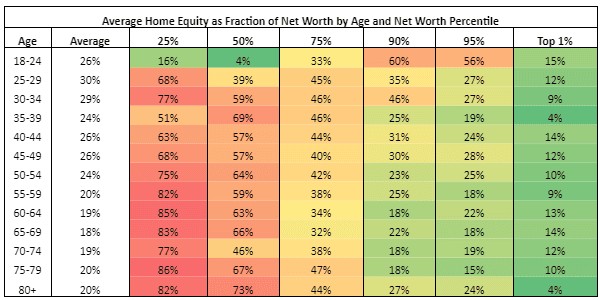

6. Home Equity as a Fraction of Net Worth

Examining home equity as a fraction of net worth provides a relative measure of its importance in overall wealth accumulation. This perspective helps to understand how reliant individuals are on their homes for their net worth. Proportional analysis reveals reliance on home equity.

6.1. Proportional Data

The following table shows home equity for various net worth percentiles as a fraction of net worth rather than in absolute dollar terms. This data provides a relative measure of the importance of home equity. Tabular data shows fractional representation.

| Age Group | Home Equity as % of Net Worth (25th Percentile) | Home Equity as % of Net Worth (Median) | Home Equity as % of Net Worth (75th Percentile) | Home Equity as % of Net Worth (90th Percentile) | Home Equity as % of Net Worth (95th Percentile) | Home Equity as % of Net Worth (99th Percentile) |

|---|---|---|---|---|---|---|

| 18-24 | 75% | 75% | 79% | 77% | 78% | 67% |

| 25-34 | 60% | 57% | 57% | 54% | 50% | 49% |

| 35-44 | 50% | 44% | 42% | 47% | 46% | 43% |

| 45-54 | 50% | 43% | 39% | 40% | 33% | 33% |

| 55-64 | 44% | 33% | 33% | 33% | 27% | 33% |

| 65-74 | 40% | 30% | 31% | 31% | 25% | 31% |

| 75+ | 47% | 38% | 36% | 36% | 30% | 36% |

6.1.1. Home Equity Dependence

Home equity is more than half the net worth at the 25th percentile, reaching as high as 86% for the late 70s age group. This indicates that lower-net-worth individuals are highly reliant on their homes for their overall wealth. Dependence metrics underscore economic fragility.

6.1.2. Median Dependence

For the median net worth, home equity is again half or more of net worth for most age groups above age 30, peaking at a somewhat lower 73% for ages 80 and over. This reinforces the importance of homeownership for the typical household. Homeownership’s central role in wealth is confirmed.

6.1.3. Higher Percentiles

Those in the 90th percentile have home equity starting at 60% in their late teens and early 20s before dropping to a range of 18% to 31% for ages 40 and over. For the top 1%, home equity plays a small role in their net worth, ranging from a high of 15% for the youngest age group down to as low as 4% for those in their late 30s and again for ages 80 and up. Wealth diversification mitigates home equity dependence.

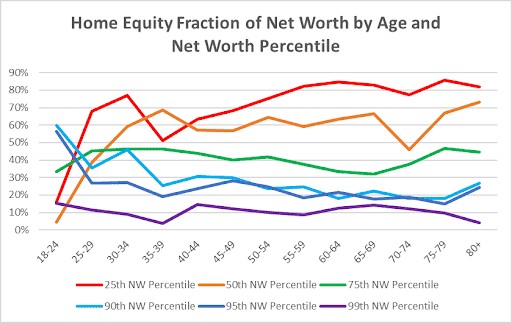

6.2. Visualizing Proportional Data

Graphs can illustrate how home equity as a fraction of net worth changes across different age groups and wealth percentiles. Visualization clarifies proportional changes.

6.2.1. Average Home Equity as Fraction of Net Worth Graph

This graph shows how home equity percentage peaks move from older to younger as wealth increases. Visual trends highlight intergenerational wealth shifts.

6.2.2. Home Equity Fraction of Net Worth Graph

The last graph shows this picture visually, where home equity plays a smaller and smaller role in net worth as one’s wealth grows. It also shows how home equity percentage peaks move from older to younger as wealth increases. Proportional data clarifies wealth dynamics.

7. Expert Perspectives on Net Worth Comparisons

While comparing net worth can provide valuable insights, it’s essential to consider expert perspectives on its usefulness and potential pitfalls. Financial professionals offer balanced viewpoints.

7.1. The Benefits of Comparison

Comparing net worth, especially with one’s age cohort, can be helpful and counterproductive. On the positive side, such comparisons can provide a benchmark, motivating individuals to save and invest more wisely to achieve financial security. It can foster competition, leading to better financial decisions and habits. Comparative analysis spurs financial discipline.

7.2. The Pitfalls of Comparison

This practice can also be counterproductive, leading to feelings of inadequacy or stress if one’s financial situation lags behind peers. It might encourage unhealthy financial behaviors, such as excessive risk-taking or overspending, in an attempt to ‘keep up.’ Psychological impacts caution against superficial comparisons.

7.3. Focusing on Personal Goals

Individuals must focus on personal financial goals tailored to their circumstances rather than purely on comparison. A balanced approach, using comparisons as a tool for insight rather than a definitive measure of success, can help readers make informed decisions while maintaining financial well-being. Personal benchmarks foster sustainable financial habits.

7.4. Viewing Wealth Accumulation as a Personal Competition

If you do choose to view wealth accumulation as a competition, it’s best to view it as a competition between your present and past selves rather than between you and everyone else. Self-improvement trumps external comparisons.

8. Key Takeaways and Recommendations

Analyzing net worth percentiles by age provides a comprehensive understanding of wealth distribution and accumulation trends. By considering these insights and expert perspectives, you can make informed financial decisions and set realistic goals. Synthesis enables informed financial planning.

8.1. Understand Your Financial Position

Use the tables and graphs provided to compare your net worth to the overall population, to see where you come out in the wealth distribution. This will help you understand your financial position relative to your peers. Comparative assessment sharpens financial self-awareness.

8.2. Set Realistic Goals

Based on your current position and future aspirations, set realistic financial goals. Consider factors such as income, expenses, savings habits, and investment strategies when setting your goals. Goal-setting drives purposeful financial action.

8.3. Focus on Personal Improvement

Rather than obsessing over external comparisons, focus on improving your own financial habits and strategies. This will lead to more sustainable and fulfilling financial success. Self-improvement yields lasting financial benefits.

8.4. Seek Professional Advice

Consider consulting a financial advisor to get personalized advice and guidance. A financial advisor can help you develop a comprehensive financial plan tailored to your specific needs and goals. Professional guidance enhances financial clarity.

9. FAQs on Net Worth Comparison

1. What is considered a good net worth by age?

A “good” net worth varies depending on individual circumstances and goals. However, comparing your net worth to the percentiles provided in this article can give you a general idea of where you stand relative to your peers. Relative benchmarks gauge financial progress.

2. How often should I compare my net worth?

It’s a good practice to review your net worth annually or bi-annually to track your progress and make any necessary adjustments to your financial plan. Regular monitoring facilitates financial adaptability.

3. What factors can significantly impact net worth?

Factors such as income, education, career choices, savings habits, investment decisions, and significant life events can significantly impact net worth. Multi-faceted variables influence wealth accumulation.

4. Is it better to focus on average or median net worth?

The median net worth provides a more accurate representation of the “typical” net worth for each age group, as the average can be skewed by extremely wealthy individuals. Median values offer robust statistical insights.

5. How does home equity affect net worth?

Home equity is a significant component of net worth for many individuals, particularly in the lower and middle percentiles. Understanding how home equity contributes to overall wealth can provide valuable insights into financial stability. Equity dynamics are critical for wealth understanding.

6. Should I include retirement accounts in my net worth calculation?

Yes, retirement accounts such as 401(k)s and IRAs should be included as assets when calculating your net worth. Retirement assets form a key part of net worth.

7. How can I improve my net worth?

You can improve your net worth by increasing your income, reducing your expenses, saving more, investing wisely, and paying down debt. Strategic actions boost overall net worth.

8. What role does debt play in net worth?

Debt reduces your net worth. High levels of debt can significantly hinder your ability to accumulate wealth. Debt management is vital for wealth growth.

9. Is it important to compare my net worth to others?

While comparing your net worth can provide valuable insights, it’s essential to focus on your personal financial goals and circumstances rather than obsessing over external comparisons. Individual goals should guide financial planning.

10. What is investable net worth, and why is it important?

Investable net worth excludes home equity and provides a clearer picture of the assets available for generating income and growth. It’s an essential metric for assessing investment portfolio performance. Investable assets drive financial growth strategies.

10. COMPARE.EDU.VN: Your Partner in Financial Understanding

Navigating the complexities of net worth comparison can be challenging. At COMPARE.EDU.VN, we strive to provide comprehensive and objective analyses to help you make informed financial decisions. Whether you’re comparing investment options, planning for retirement, or simply trying to understand your financial standing, our resources are designed to empower you with the knowledge you need. Objective analysis ensures informed decision-making.

Are you looking for detailed, unbiased comparisons to help you make sound financial decisions? Visit COMPARE.EDU.VN today to explore our extensive collection of articles and resources. Don’t navigate the financial world alone; let us help you compare, understand, and succeed. Contact us at 333 Comparison Plaza, Choice City, CA 90210, United States, or reach out via WhatsApp at +1 (626) 555-9090. Your financial clarity starts here at compare.edu.vn.

Disclaimer: This article is intended for informational purposes only and should not be considered financial advice. You should consult a financial professional before making any major financial decisions.